Canadian natural gas producers

I have taken a small equity position (roughly 2.5% each) in two Canadian natural gas producers. I’ve exhaustively looked at the (not obviously insolvent) producers that are at least 75% natural gas boe equivalent and chosen the two companies I’ve deemed ‘best’ in lieu of just making a home-brew index of all of them.

This is not a particular call on the natural gas industry in general – right now the economics are absolutely horrible for Canada. There have been some days where spot pricing has been such that you have to pay to give away your natural gas! The federal government is hell-bent on destroying the fossil fuel industry. The USA has shale gas coming out of their… well, you know. There’s no hope and only despair!

Sounds like a good time to invest.

However, run the thought experiment on every company you look at: “Let’s pretend you could acquire 100% of the company’s equity for ZERO, but had to take a personal guarantee on their outstanding debt. Would you take them over?”

Under the right conditions, a lot of these companies will double, triple or even quadruple their equity prices. The timing is unclear, but we will see. I remember getting into oil and gas for a short-lived foray in 2014 that exhibited a colossal amount of stupidity, but will this time be different?

Canadian preferred shares – commentary

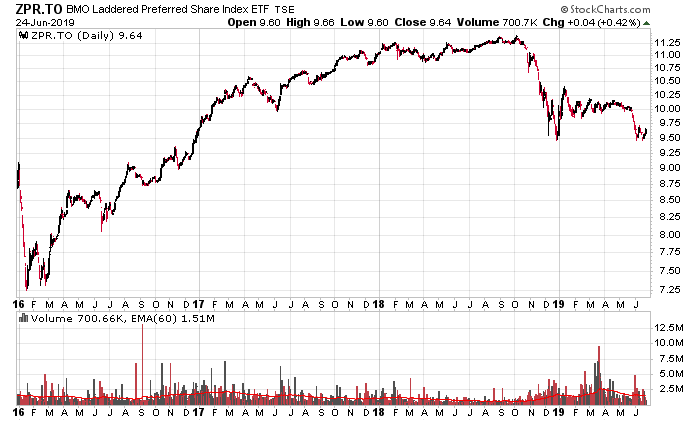

Early 2016 was a good time to invest in Canadian preferred shares, and there was also a lot of carnage in the equity market at the time. Five-year government bond yields bottomed at 0.48% in February 2016, and you can see the damage it did to the preferred share market – ZPR is an ETF that tracks 5-year rate resets:

What is interesting is a well-timed entry on the bottom (not completely clairvoyant, but say $7.50/unit) and an exit anytime between October 2017 to 2018 would have netted a total return that exceeded the TSX with less risk. Of course, you can’t determine those preferred shares will do better than the TSX when you’re sitting at your computer console in February 2016!

Today’s investing environment has plenty of parallels – the 5-year interest rate has dropped to 135bps from 240bps back in October. If 5-year yields continue to drop further, there is a high degree of likelihood that preferred shares will also be sold down to levels seen in 2016.

The question is getting the timing correct.

A lot of retail investors get burnt by buying into a relatively high yield product thinking it is safe. While the yield itself may be safe (it has been awhile since I can recall a dividend suspension in the Canadian preferred share marketplace beyond Aimia and some really garbage split-share corps), the capital is most certainly at risk. It looks like a very easy leveraged trade on paper when margin rates are 2.5% and you see a financial instrument at 5%, but how much pain can you take when the yield goes to 6%? 7%? You’ve just lost nearly 17% and 29% of your capital, respectively.

Using a real example, investors in Brookfield Preferred Shares series 30 (TSX: BAM.PR.Z) back in September was trading at par, had a near-guarantee 4.7% yield, and a rate reset of 2.96% over the 5-year government bond rate. Some enterprising chap sees margin rates at 2.5% and decides to invest $50,000 cash to buy $100,000 of BAM.PR.Z. Now they’re sitting on $23,000 in equity plus $3,500 in accumulated dividends and they would have surely received a margin call (or would be very close to one). How much of the population out there is leveraged to preferred shares in this manner and are feeling nervous? How many will hit the sell button to take the tax hit and move away from this “guaranteed leveraged return”?

Ideally when they all want to cash out, that’s the time to get in. Doesn’t quite feel time yet.

Hudson’s Bay – Internal take-over

This is a few days late, but the headline coming from (TSX: HBC) is: “Shareholders Collectively Owning 57% of Hudson’s Bay Company’s Outstanding Common Shares Submit Take-Private Proposal for C$9.45 per Share in Cash”.

Almost anybody investing in this company from 2018 back will have lost money.

Today, HBC announced a very tepid quarterly report (this surely is not coincidental to the timing of the take-private offer – gives it some urgency to accept it). Sales down, gross profits down. Not good.

The takeover offer gives a $1.74 billion valuation to the equity, which I think existing minority shareholders will take in a heartbeat. I can’t see anybody else step in and give a better offer.

I think it is pretty inevitable that HBC will cease ordinary retail operations very soon – they either have to go very specialty or just get out of the business – a struggle not unknown to other retailers which have also been hammered to death as purchasing trends continue to shift.

Atlantic Power / Williams Lake

There is a staggering degree of government regulation with any projects of significance. This creates competitive barriers to entry for would-be entrants.

The most public of these projects are oil pipelines, but even operating power plants are subject to a ton of public scrutiny and the wrath of the public.

Atlantic Power operates a biomass power plant in the northwestern outskirts of Williams Lake, BC, generating up to 66 megawatts of power.

They had applied in 2016 to amend their permit to accept the chipping and burning of used railroad ties. The BC Ministry of Environment approved this, but it was appealed on behalf of certain residents of Williams Lake, BC. The BC Environmental Appeals board ruled on April 11, 2019 that Atlantic Power could burn an average of 35% rail ties as its biomass each year, up to 50% on a daily basis. The community group that effectively lost the appeal took it to City Council, but council denied their request (which, in any respect, would be non-binding).

In 2018, Williams Lake generated $8 million in EBITDA. The main power purchase agreement expired on April 1, 2018 and has been extended on less favourable terms on a short-term basis.

Finally, for those that are willing to get into the nitty-gritty of the technical assessment of Atlantic Power’s biomass power plant in Williams Lake, you can read the 2016 technical assessment concerning their request to burn rail ties.