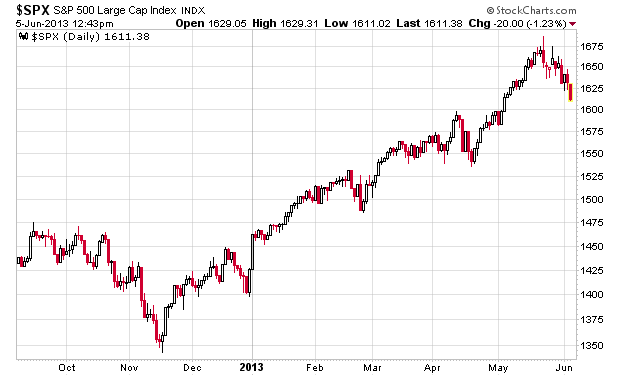

Pay attention to the S&P 500.

My underlying impression at this point is that asset values are generally being propped up by the fact that there is really nothing else to fuel speculation into. The actual value within the index is not tremendously overvalued at the moment, but it is frothy.

I believe we’re setting up for a moment where both equity and fixed income are going to get hammered simultaneously, which is not a very common market event – normally the two assets are anti-correlated.

The only safety will be cash. Equally acceptable will be short-term treasuries although considering the yield (nearly zero) of anything less than 1 year of term, is more or less a proxy for cash.

That said, when analyzing the data and also analyzing sentiment, my guess at this point is that we’re going to get one more intermediate market rally. However, this will continue to be a good opportunity to liquidate holdings and raise cash.