Why blind index investing doesn’t exactly work – or beware the TSX Venture Exchange!

Typical free advice you hear on other channels talk about the virtues of passively investing in indicies. While putting some money in the S&P 500 or TSX Composite (generally speaking, close-to-the-top 500 and 60 capitalized companies in the USA and Canada, respectively) will likely represent a broad proxy for the corporate profitability of those two countries and over the long haul you will make profits in line with the growth of the overall economy, there are also bad indicies one can invest in.

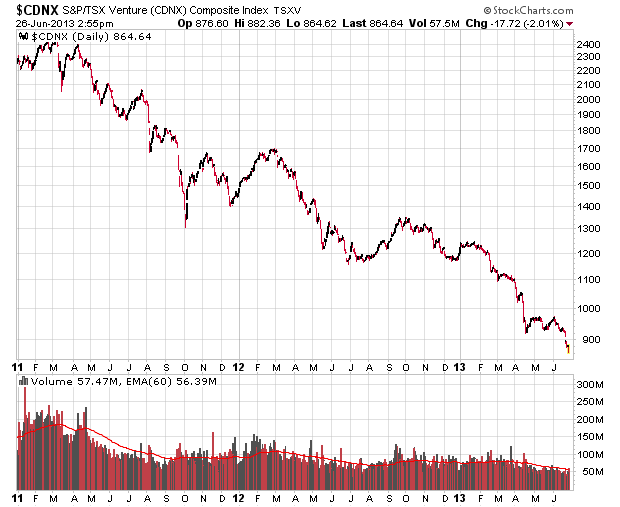

Such as the TSX Venture Exchange.

Right now it has 385 constituents, and they are not doing so well:

An investor in the TSX Venture index will have lost roughly 2/3rds of their investment over the past two years, while TSX Composite investors would have lost about 15%.

It goes without saying that if you invest in a basket of junk, it doesn’t matter how much diversification there is in that basket, you will get junk results. And this is indeed the case for the TSX Venture – it is an utterly failed index.

If you do have to dip your toes into the index, I would highly suggest cherry-picking for firms that have nothing to do with the mining sector. This leaves about 15% of the index (capitalization-weighted). Fundamentally, it seems nothing has really changed since the Vancouver Stock Exchange era where seemingly half the companies involved were just simply there to defraud investors.

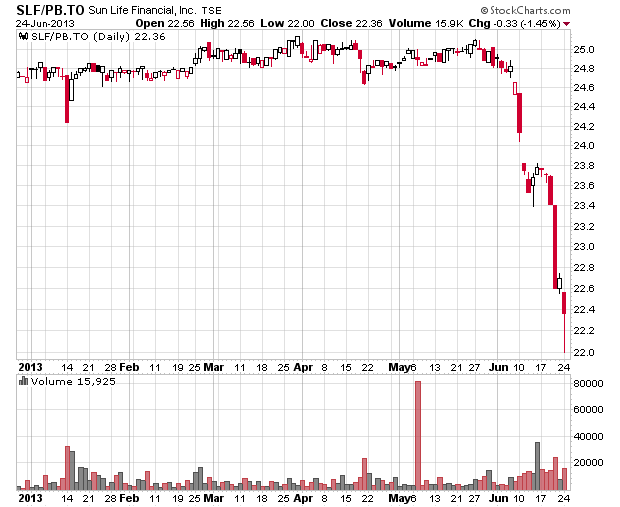

Preferred shares getting hammered

Investors that are doing the simple “borrow at 2%, invest in a fixed income product at 5%” are getting a lesson on leverage today when they see charts like this:

I just chose Sun Life Preferred Series B for just a complete random example and is no way an endorsement of this security – however, this series of preferred shares gives off a lazy 30 cent per quarter dividend and just one month ago was trading near par value, which would have given its investors a 4.8% yield.

Now, investors are waking up to see they have lost 10% of their capital, which is about two years’ worth of yield if the price doesn’t subsequently appreciate.

The odd thing is that predicting when the bottom ends is a very difficult guessing game of how desperate everybody is to liquidate income products in exchange for capital. If people are still leveraged and their equity is running low to the point where they still need to raise capital to maintain their positions, then we will still see further dumping into the market and lower prices.

We do have a good example of what happens when this occurs – in the depths of the economic crisis in 2008-2009, this preferred share traded as low as $13 – or 52% of par value.

All of this is likely a function of the underlying fixed income instruments (30-year, 10-year treasuries) getting bidded up in a volatile fashion and the subsequent capital losses there are reverberating into the more junior markets in terms of balancing portfolios. In other words, anything with a yield is getting liquified.

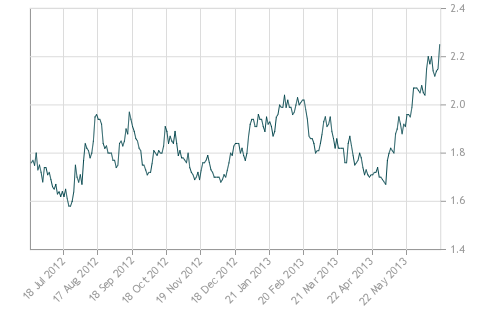

Bond prices – inflation, deflation

Yields are finally rising. Canadian yields on the 10-year bond:

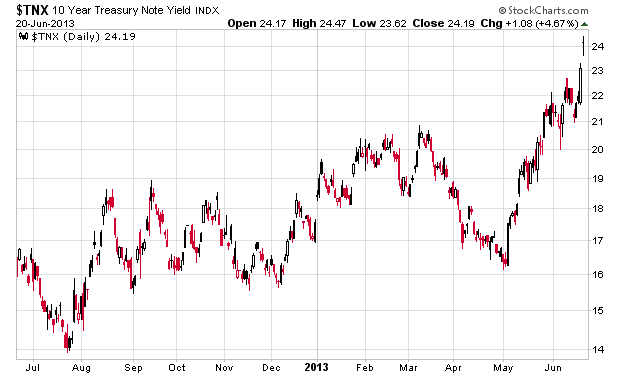

Yield on the 10-year US treasury note:

While this may look dramatic, it should also be noted that yields on the 10-year note in the middle of 2011 was hovering around the 3.2% level, so the current yield of 2.5% isn’t not that high – indeed, it makes the 1.7% range that things were trading at before the spike up appear to be that much more low.

That said, the question remains on how this is going to impact the rest of the credit market, especially the corporate debt market. Spreads between treasuries and BBB-rated type issues are still at relative historic lows and I wonder if we will start to see a pricing of higher spreads once more.

If this is the onset of a market panic to get out of any assets (fixed income, equity, commodity, real estate) then the only safe haven will continue to be zero-yielding cash. The beneficiary in such an instance would be the US dollar.

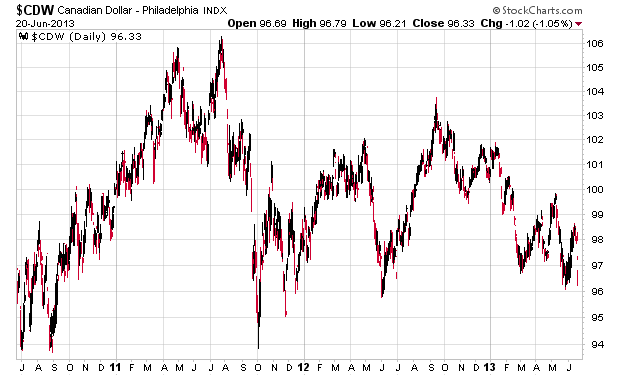

We have the last three years of trading on the Canadian dollar and could this mean a weakening of Canadian currency, relative to the US dollar? Time will tell. I have been more or less positioned 2/3rds in US currency since 2012 so this tells you how I think this is going to be resolving itself.

Markets finally getting interesting again

Today continues the trend of the decoupling of correlation between the main equity indicies and the bond market – both are down today, heavily. Along with Gold and other commodities, my guess at the moment is that this is going to be the start of some significant downturn.

I have continued to sell shares and am anxiously awaiting a proper time to pounce. These sorts of mini-developments take time to work their way through the technical trading side of the marketplace, so it is far too early. I still had the belief that there would be an intermediate rally up to the S&P 1700-ish level but obviously this is mistaken. That said, I am decently positioned and 2/3rds of the portfolio are in things that are trading under tangible book value, so I am quite defensively positioned.