There is a strong possibility that Genworth MI (TSX: MIC) will make some sort of announcement this month, specifically with respect to what they are going to be doing with their excess capital.

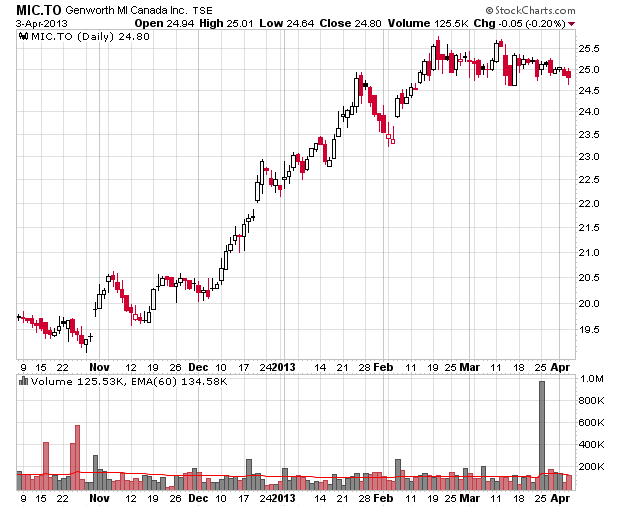

A chart of MIC shows that it has gone nowhere over the past month, but this has been since quite a run-up since last August when it traded all the way down to about $16/share.

At the beginning of January 2013, MIC had about 210% of the minimum capital test that is required and the company has an internal target of 190%, which means that they had about $287 million in excess capital available. This does not include the additional capital that has accumulated in the first quarter of 2013.

Having this extra capital (noting that $337.87 million was in very low-yielding cash and short-term equivalents at the end of 2012) is lowering the return on equity, reducing portfolio yield and is producing a drag on performance. The cash can be safely returned into the hands of investors.

There are four options available, noting that it is unlikely that acquisition is a possibility given the very narrowly-defined scope of the industry the company is in:

1. Buy back shares: Likely through a dutch auction tender and at a higher level than existing market value. They have done this two times in the past.

On July 15, 2010, they announced a $325 million buyback between $24 to $28/share and on August 24, 2010 they announced that $26.40 would be the tender price. The stock closed on July 15, 2010 at $23.07/share and the day after it opened trading at $24.25. The market price on August 24, 2010 was $25.79/share. Genworth Financial proportionately tendered its shares to keep its 57.5% ownership stake in MIC.

On May 5, 2011, they announced a $160 million buyback between $26 to $29/share. The market value was $25.25 on the day of the announcement, and the stock opened at $25.55 the day after. On June 27, 2011, they announced that $26 was the price and the closing market value that day was at $25.77/share. Notably after this buyback, the market value fell in the subsequent months.

Given the current market value of the company, if they were to proceed with a similar tender, it would be almost on similar terms as the previous one, with perhaps a tender range between $26 to $29/share. This would be close to book value and this would achieve about a 10% reduction in share count and subsequent 11% increase in earnings per share.

2. Give a special dividend: A special dividend of $287 million would be equivalent to a $2.90/share dividend. The only special dividend declared to date was announced on November 3, 2011 of a $0.50 dividend, payable on December 1, 2011.

3. Some combination of the two;

4. No decision, keep the cash, and wait for less stormy days later.

Influential in this decision will be the needs of the parent company, Genworth (NYSE: GNW), whom is looking much more financially stable than it was back in 2010 and has no pressing need for an infusion of capital either way.

My guess at present is that Genworth MI will launch a tender for its own shares this month. They are still trading under my own estimate of its fair value.

As readers are aware, I have been long on Genworth MI since last July.