No positions after the Spruce Point debacle, but reviewing the year-end GFL Environmental (TSX: GFL) statements, they are still a huge train wreck.

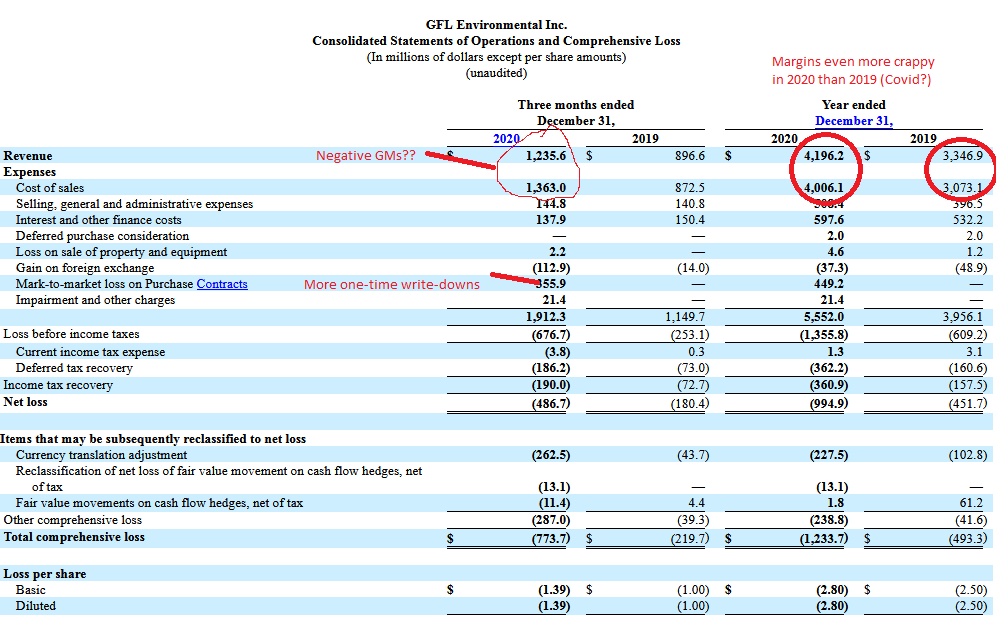

Income statement, with some colour commentary:

The gross margins are exceedingly thin (and indeed in the last quarter, negative). We can’t make money per unit of revenue, so we’ll make it up on volume!

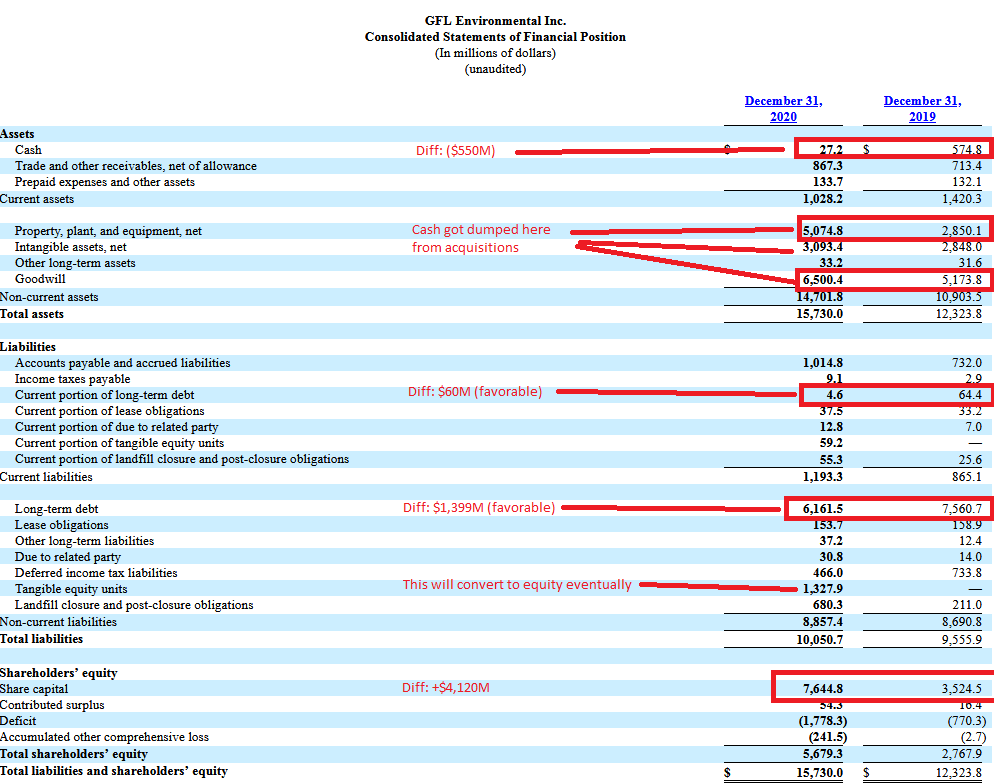

The balance sheet tells more of a story:

From the end of 2019 to 2020, the company:

Raised $4.1 billion in equity financing (and another slab of money in “Tangible Equity Units” which trade as GFLU; these will be converted to equity).

They also were able to pay down a net of $1.46 billion in debt with the above line.

However, on the outflows we have the following:

Cash: negative $550 million

PP&E, intangibles, goodwill: $3.8 billion net

So about $4.3-$4.4 billion out the windows in a year. These were to complete the WMI acquisitions. This is a lot of money out the door. I’m also ignoring the $1 billion or so in the increase of the deficit, which I’ll very generously dismiss and chalk up to one-time contract adjustments, foreign currency translation, and operational issues. Presumably the prior expenditures went for the purpose of building a return on equity it would be a good expenditure of capital.

Management claims guidance for an “Adjusted Free Cash Flow $465 million to $495 million” for 2021 and an “Adjusted EBITDA $1,340 million to $1,380 million”.

The question for an investor is whether they can produce an un-adjusted free cash flow, full stop. The historical financial statements are at complete odds with what management is saying. It doesn’t mean they won’t be able to produce positive financial results in 2021 and beyond.

I truly don’t know.

They still appear to have a very good ability to raise capital. On December 2020, they closed another US$750 million financing of senior secured notes at a 3.5% coupon, good until 2028, and also sliced another 50bps off their $1.3 billion credit facility. Their common stock is also near their all-time highs, about CAD$38/share.

Again, I’ll just leave this one up to smarter people than myself to evaluate, but this is one fascinating case study.

EBITDA adjusted by the cost of sales? 🙂

“Environmental adjustment” to share price seems to be in the same bucket as other modern price multiplicators like “crypto”, “renewable”, “fintech” etc.

Within cost of sales for 2020 is $1,237mn of depreciation vs. acquisition of PPE of $428mn. So bulls are essentially betting that depreciation overstates the true cost to maintain the business they have today.

Even if that is true, if one takes CFO of $502mn less $428mn of acquisition of PPE, one is left with $74mn of levered FCF. On a $12bn market cap it’s not very impressive. If one then adds back interest expense of $443mn, one gets to $517mn of unlevered FCF on an EV of $19bn, also pretty lousy.