Corvel (Nasdaq: CRVL) announced their year-end results (10-K). The company has such fanfare that it has precisely zero analysts following it, so the automated news generators couldn’t even tell you whether they ‘beat’ or ‘missed’ expectations. There are few (USA) domestic companies that have billion dollar market capitalizations that have zero analyst coverage.

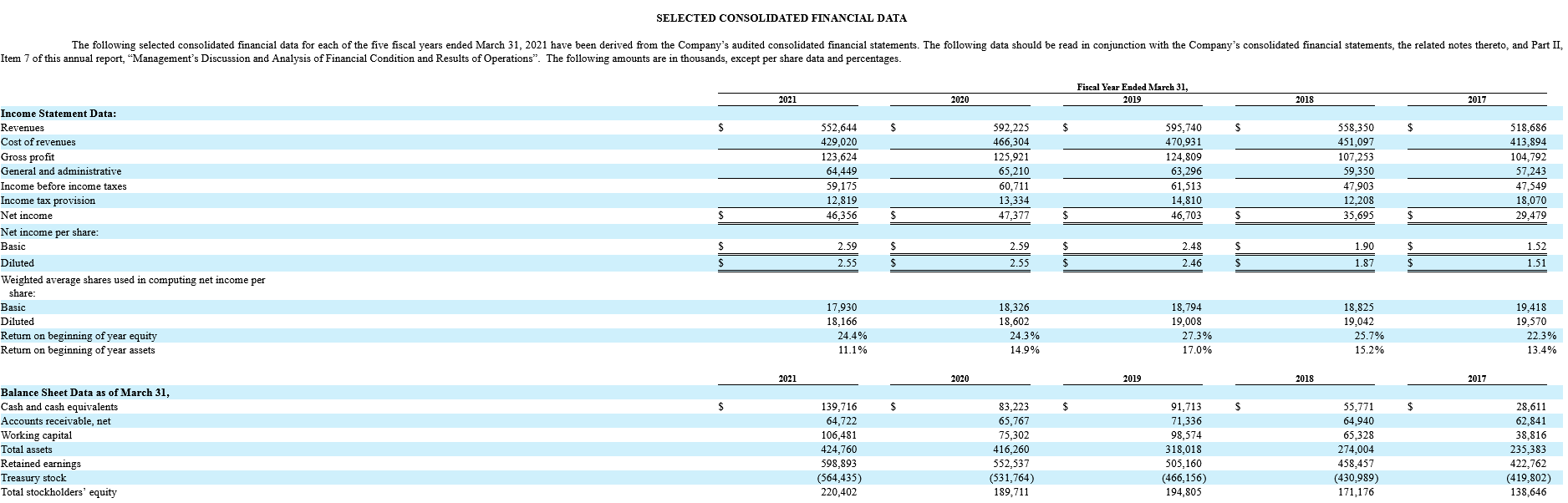

Their fiscal year ends on March 31st, so this was their Covid year. Revenues dropped about 7%. Margins, however, remained consistent. They made reference in their last quarterly conference call to streamlining real estate leasing costs as they were able to seamlessly ‘go online’. This can also be seen in the recent dramatic drop in IFRS 16 asset/liability for leases vs. the previous quarter. Year-to-year, lease obligations are down by half, and this is explained by the company projecting that renewals will not be exercised.

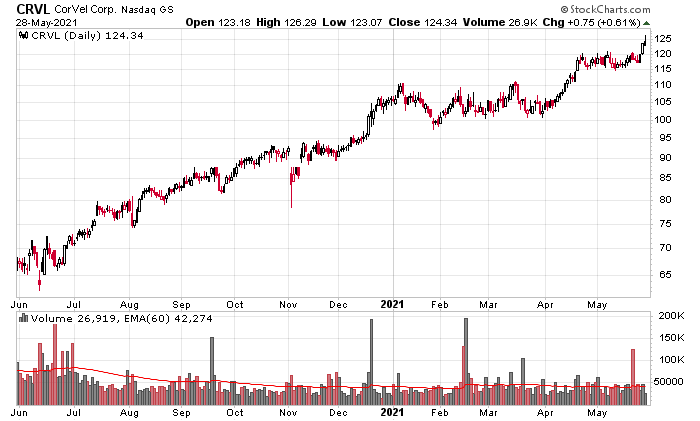

The company has nearly doubled in share price since last year. Valuation-wise, they are at about 50 times the previous twelve months of earnings. Needless to say, this appears to be rather rich, but the earnings should accelerate in the upcoming fiscal year as employment in the USA continues to expand, especially as Covid supports terminate.

Although it looks like that revenues and net income has flat-lined over the past three years, there will likely be an upward trajectory going forward. In addition, note the historical ROE numbers of 20%+. The ROE number next year will be down as the amount of cash on the balance sheet will serve to be a drag on the denominator, but this will likely be transitory.

I also believe the stock has been a positive recipient of automatic index buying. Trading of the stock is thin, with spreads typically a dollar or so. The company is currently on the S&P Smallcap 600 index, although it is well below the liquidity threshold for the index. Their market cap, over $2 billion, is creeping up to the point where they are getting into mid-cap territory.

Historically, the company has engaged in a capital allocation policy of repurchasing shares (they repurchased approximately 100,000 shares, or about half a percent of their shares outstanding in the past quarter at an average of US$104). Despite this, the company has been building up cash on the balance sheet, and the US$140 million they have at fiscal year end is an all-time high. I do not think management is of the type to suddenly declare a treasury policy of purchasing Bitcoins with spare US dollars. They also have little use for excess capital – they continue to engage in the usual R&D that software companies should be doing. In a paradoxical sense, this lack of capital reallocation is a negative in that the corporation cannot “snowball” retained earnings into more fruitful endeavours (unlike an acquisition machine like Constellation Software (TSX: CSU)). CRVL management is very happy to stay in their niche and only make the tiniest steps outwards from their strategic niche.

Operationally, they are in a dominant position, which explains the valuation. Indeed, when compared to companies like Constellation, they are trading at 85 times past earnings. On an absolute level they are expensive, but relatively speaking, it is in the ballpark. Another metric is price-to-sales, and also this makes Corvel cheaper than CSU. I would make the claim that CRVL’s niche has a much stronger competitive moat and justifies a premium valuation as a result. Their management is even more reclusive than CSU’s Mark Leonard. This is a trivial analysis, but a few of the factors swimming in my head when I look at this company in my portfolio and wonder if I should reallocate.

For many reasons, I will not be. I do not know what price the shares will rise to before I say enough is enough and seriously think about the sell button. I can easily see them staying where they are currently for a lengthy period of time, but I can also see reasons for them to head up to $200 and higher.

My only regret was not picking up a little bit more when I did, but at that time in the Covid crisis, there were many other things floating on my radar at the time. This is probably the least dramatic investment in my portfolio at present. They consume a disproportionately lower amount of attention in relation to their size in my portfolio, which is in the top 5.

Three months after I post this, CRVL is up another third. The underlying business is indeed doing very well – their last quarterly report was very good. But this is one of those rare cases in my portfolio where valuation is getting further and further into nosebleed territory.