How much spare change should you keep behind the couch? You need a little bit in case if you want to head out to the grocery store to pick up some beer and popcorn, but too much of it and it will be wasting away earning a zero yield, which can be more efficiently thrown into the short term treasury bill market where you can skim off a rich 25 basis points. Depending on how much you actually have in the couch, that could translate into an extra beer!

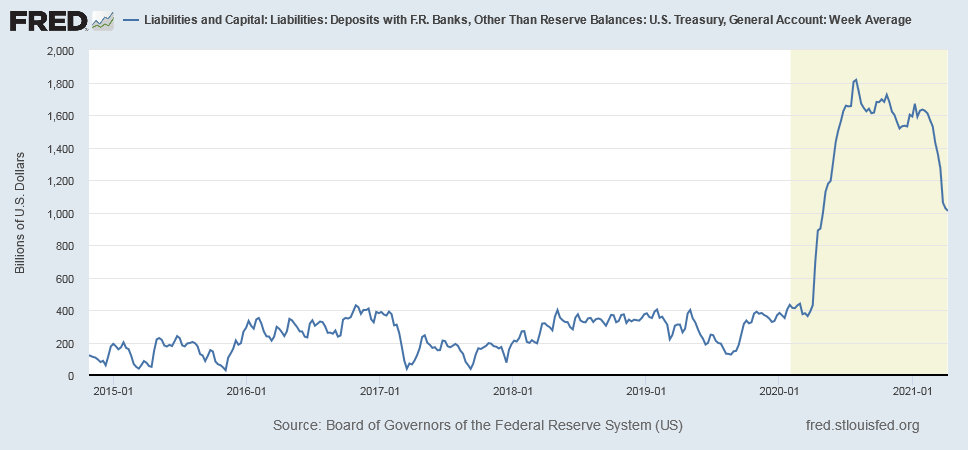

Sarcasm aside, in the case of the US government, they raised a ton of money during the COVID-19 crisis as illustrated by the following chart:

In recent history, the US treasury normally keeps $200-$400 billion in cash available for day-to-day operations (noting that the annual US deficit in recent years typically hovers around the trillion dollar range), but they raised about 5 times this much during Covid-19.

However, now that the worst of things presumably are over, they have begun to bleed away this excess cash balance, approximately half of it. This can be attributed to some factors, but I would estimate the stimulus spending bill has accelerated the distribution of this cash, coupled with the necessity of keeping a high float due to the even further elevated deficit the government is incurring (estimated $3.3 trillion in 2020).

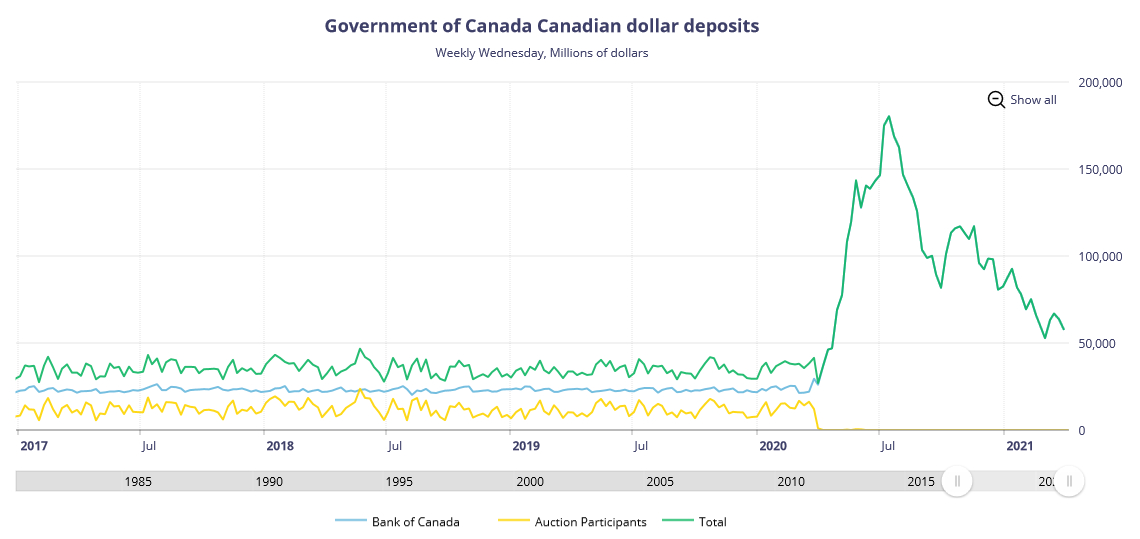

I don’t know what to make of the implication of the US government bleeding off the cash balances, but I will also note that the Government of Canada appears to have a similar trajectory:

Balances held by auction participants have presumably been zeroed because participants could get higher yields on their capital from other areas.

My understanding is that with the BoC still engaging in a very healthy amount of quantitative easing (‘at least’ $4 billion a week) interest rates will continue to be suppressed. I will note that the 10-year yield has almost reached to the range of the pre-Covid yields and the financial overlords are probably trying to manage some fine balance between the level of QE vs. what is truly going on in the economy. However, the current course of action (accumulation of massive amounts of debt and monetary suppression of interest rates) will come at a cost of economic growth being lower than what it could be – it is sort of like strapping additional weights on the ankles of a marathon runner.