One rewarding aspect of finance is that participants that correctly perceive reality are eventually rewarded with additional capital, provided you stay solvent longer than the market remains irrational.

As markets are an amalgamation of sentiment, there is an element to psychological timing with regards to asset prices. The prices that are currently seen represent the baked in assumptions of marginal buyers and sellers, each trading with their own motivations – some extremely short-term, some extremely long-term. Another vector is the advent of environmental, social and governance (ESG) driven investing. Formerly labelled as “socially responsible” or “ethical” investing, ESG has generalized this to refer to politically correct practices.

As the politicization of financial markets continue, it is obvious that a focus on ESG and politically sensitive institutional investors (e.g. public pension plans and the like) will take a factor in investment decision making. This has long-since been baked into certain asset prices. Political favourites, such as renewable energy initiatives, have resulted in such assets receiving premium valuations and hence low returns for current investors. Such assets are typically aided by government subsidies (in the form of attractive power purchase agreements, or in the case of Tesla, outright tax breaks and subsidies).

This sort of gaming goes on all the time in most industries, as participants jockey for position. Large entities try to assert control through rent-seeking techniques. Nothing is a better example than how various entities are reacting to COVID-19 – companies such as Amazon are cheering for continued lockdowns as they continue to eat away at conventional retail. The medical industry, both private and public, are cheering their nearly unassailable position as nobody can question the quantum of spending in relation to the overall benefit – “anything to save a life” is the current expectation. By the time it comes to pay the bills, the blame will be attributed to other factors.

On the flip side, we have the ‘enemies’ of ESG, which generally constitute a list of firms in politically incorrect industries. One of these industries that are deeply politically incorrect at present (especially in North America and Europe) is oil and gas exploration.

When looking at core valuation of the major Canadian oil and gas firms, there is a major valuation gap between what the ambient market is offering versus what cash is being generated by the companies in question.

For instance, Canadian Natural Resources (TSX: CNQ) gave out guidance on May 6, 2021 that assuming a US$60/barrel of West Texas Intermediate (right now it is US$63.50 on the spot contract), they will be able to generate around $5.7 to $6.2 billion in cash flow, and this is after their capital expenditure and dividend payout (which is another $5.4 billion). Backing out their $2.2 billion annualized dividend to zero, that’s around $8.2 billion in free cash flow (FCF).

Recall that CNQ’s enterprise value is currently around $67 billion, so a rough valuation would be an EV/FCF of 8 times. This means if things continue at current prices, CNQ could pay down all their debt and buy back all their shares outstanding (at current prices) in 8 years. This isn’t an isolated case. The other Canadian large players, Suncor, Cenovus, Tourmaline, are roughly the same (plus or minus one or two points). There are no other ‘substantially Canadian’ plays that have a market cap of above $5 billion at present (Imperial Oil is 70% owned by Exxon, and Ovintiv, the former EnCana, is now primarily a US producer).

You cannot find valuations like this anywhere else on the large-cap market. A typical utility such as Emera (TSX: EMA) trades at roughly 18 times EV/operating cash, never mind capital expenditures! Royal Bank (TSX: RY) trades at 15 times earnings. Perhaps the only outlier I can find in this respect is E-L Financial (TSX: ELF), which posted a 2020 net income of $129/share (on a current share price of $948).

Needless to say, Canadian Oil and Gas looks cheap, and one reason for this (other than the horrible regulatory climate) is the investment ineligibility due to ESG. The irony is that this creates opportunity for returns for those that want higher returns, such as international investors that do not take North American ESG into their investment consideration.

I can think of one analogy in the past which reminds me of today – the plight of tobacco companies in the late 90’s. Tobacco companies (most specifically, Philip Morris) were vilified in the 90’s for having the gall to produce a product that caused lung cancer and collectively denying it until they had lost all public support. The watershed moment was a US$200 billion settlement with the states in 1998, but in reality, this agreement secured incumbency rights for the existing players. The Philip Morris example (now known as Altria) has them earning $3.20/share in 1999, while the stock closed at $23/share for the year. They bought stock like mad during the dot-com boom and shareholders got very rich. Incidentally, Philip Morris was right up there with Microsoft in terms of generating shareholder value over decades (not really the case today anymore, although tobacco continues to remain very profitable).

I’m going to make a much looser analogy with Warren Buffett buying Apple stock in 2017 and 2018 (at his cost basis of $34/share to the tune of some 907 million shares he currently holds today) is giving him a current earnings yield of about 15%. There are of course key differences – with Apple, you have to assume they can continue selling iPhones, iPads, Macbooks and ‘iApps’ at their monstrously high margins indefinitely. With oil and gas you have to make an implicit assumption that the underlying commodity prices will stay steady. This is another argument for another post, but please humour me by granting this assumption.

Buffett, by virtue of his size and relative fame, is constrained by political considerations. The cited justification for selling off his shares in airline companies at the onset of the COVID-19 crisis was politically motivated – the chances of airlines getting public money bailout with (deep pocketed) Berkshire being a 10%+ shareholder was much less, so they had to sell (I am not sure if this is retrospective analysis that actually went on during the sale, or whether it was a simpler case of the original investment thesis being broken). This is not the only example.

In the most recent 13-HF, we had Berkshire disclose that it had sold half of its Chevron stake and all of its Suncor. Chevron is obviously going to be completely divested by next quarter. There is nothing in Berkshire’s public holdings that relate to oil and gas production going forward. This is very intentional, and I believe it is for political reasons.

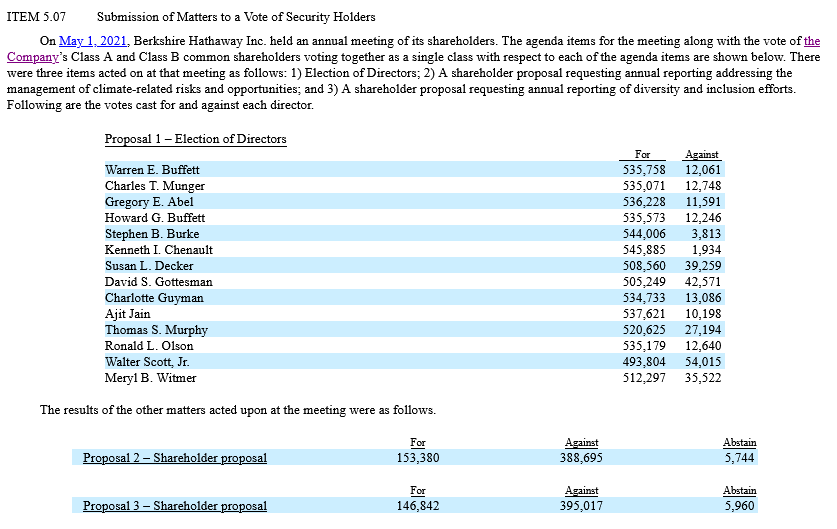

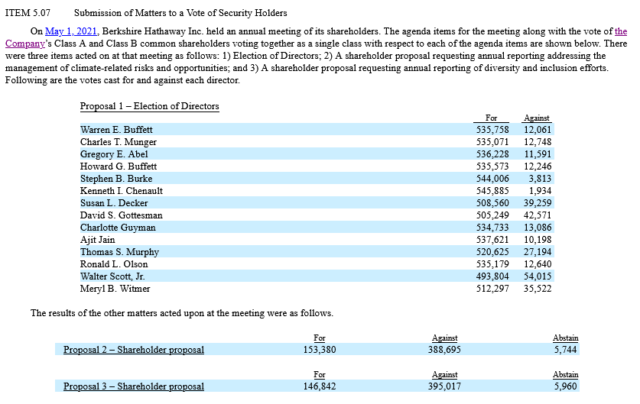

Buffett is the son of a former US Congressman and should know a lot about the political dynamics that is going on with ESG currently. There were two shareholder resolutions that came up during Berkshire’s last annual meeting. One was from Calpers and the Quebec Pension Plan, two very credible institutional investors:

In order to promote the long-term success of Berkshire Hathaway Inc. (the “Company”) and so investors can understand and manage risk more effectively, shareowners request that the board of the Company publish an annual assessment addressing how the Company manages physical and transitional climate-related risks and opportunities, commencing prior to its 2022 annual shareholders’ meeting.

The other (from a generally unknown proponent) was:

Shareholders request that Berkshire Hathaway Inc.’s (“Berkshire Hathaway”) holding companies annually publish reports assessing their diversity and inclusion efforts, at reasonable expense and excluding proprietary information.

Normally such shareholder resolutions get voted down, heavily. The Board of Directors almost universally recommend a vote against such resolutions.

However, the actual results of the votes got somewhat close:

There were approx. 548,000 votes cast in the meeting (some votes are not cast due to them being held by brokers that do not vote). The directors control 272,900 of the votes (the vast majority of this is from Buffett himself). So the vote result was a foregone conclusion.

However, excluding the directors’ votes, both resolutions passed with a slim majority.

This has to be interpreted to be a warning shot across the bow to Berkshire and almost any other corporation out there with a large public presence. They are not immune from activist politics and the politics driven behind institutional shareholders.

You can imagine how Buffett might be frustrated in not being able to deploy capital into a field that is liquid enough to make an impact on Berkshire. However, with the world examining his holdings every quarter, he must take politics into his investment considerations.

ESG, just like most political interventions, cause market distortions between perception and reality that can last for years if not decades. Hundreds of billions of dollars of capital are being invested not with a return in mind, but rather with a heavier consideration to other factors, including those that are acceptable today (which may or may not be acceptable tomorrow). Pharmaceutical companies were completely vilified before COVID-19, and now they are being showered with immunity from Covid vaccinations and have a gigantic regulatory shield to work with (until they are no longer in favour again for making outlandish profits). Today’s enemies are those relating to climate change, but this may change in the future as demand for fossil fuel energy outstrips available supply.

I am not making a moral judgement on ESG and its intentions. I am claiming, however, that ESG-driven considerations are causing significant distortions in the returns of investments that would have not otherwise existed.

Ultimately for equity investors, cash flows will dictate returns. It might take some time for political fashions to turn, but just like Philip Morris investors in the late 90’s, they were very well rewarded. Eventually the paydown of debt and payments of dividends and buyback of shares trading at single digit multiples will result in higher equity pricing, no matter which trends are politically correct.