The most underperforming stock in my portfolio in 2020 has been Atlantic Power (TSX: ATP, NYSE: AT – note you would have done much better had you invested in AT on the TSX!). My original write-up on Atlantic Power was in July of 2018. I’ve owned the common and preferred shares since then, but currently hold only the common shares.

Rule one of investing is don’t lose money, and rule two is to look at rule one. The reason why this company is still in my portfolio is because they haven’t lost (too much) money, and because there is opportunity for appreciation that hasn’t yet been reflected in the equity value of the company. People investing in the preferred shares (specifically AZP.PR.B and especially fixed-rate AZP.PR.A) would be sitting on a higher quantum of capital by virtue of dividends and some minor capital appreciation, but I do suspect the better days ahead will be for the equity owners. Since January 2015 (which is when the current CEO, James Moore, was hired), the stock has meandered around the CAD$3/share level and has been relatively uncorrelated to the overall markets.

In my original post, I posted the basic metrics from 2012 to 2017 and they were in a reasonably positive trajectory. I will update this for 2020:

Debt / Revenues / EBITDA / Shares Outstanding (millions, and USD)

Year-end 2012: 2071 / 440 / 226 / 119.4

Year-end 2017: 821 / 431 / 288 / 115.2

Year-end 2019: 649 / 282 / 196 / 108.7

TTM 2020-Q3: 585 / 267 / 180 / 89.2

The highlights here are that revenues are dropping (because of the expiry of the power purchase agreements) and this will continue. Management continues to spend much capital paying down debt and repurchasing a huge amount common stock for roughly US$2/share, and to a lesser degree, preferred shares. There was a fire at the Cadillac biomass power plant that caused a few million in damages (the remainder was picked up by insurance) which didn’t help, coupled with the usual COVID-19 theatrics (which didn’t affect the company too much operationally). Power supply drama in California also is giving a lifeline to the company’s sole plant in the state, which is a natural gas plant.

Biomass is not a preferred form of energy which lead to the company pulling the trigger on the acquisition of some biomass plants. Year-to-date, this consists of about 8% of the company’s EBITDA; due to the Cadillac fire, the Williams Lake re-start (which a power purchase agreement was finally reached with BC Hydro) and some maintenance issues at the newly acquired biomass plants, the rest of the segment’s performance has been mediocre, although this will likely pick up in future years.

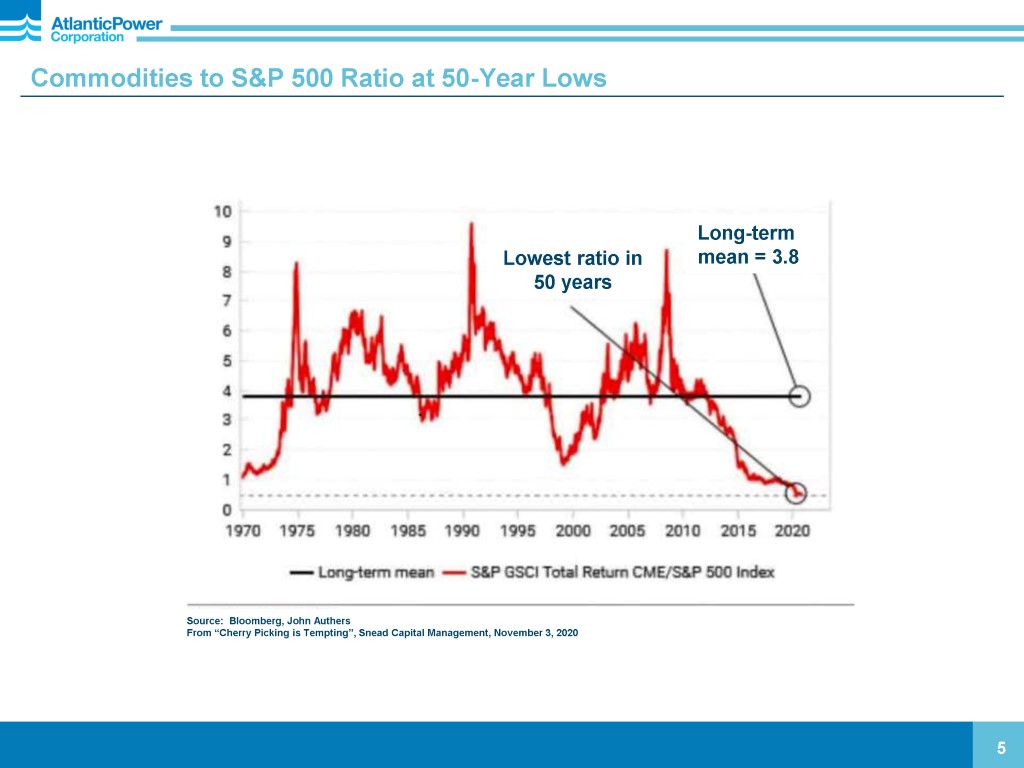

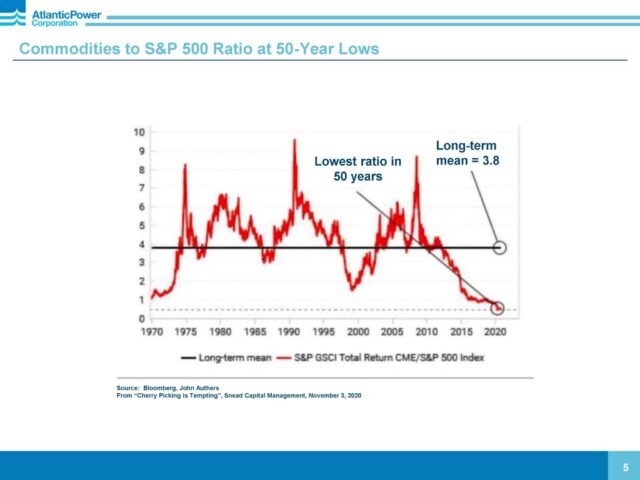

The CEO continues to say all the right things, and unlike a lot of others that talk about capital allocation and give the Buffett talk, I believe he walks it as well. One interesting highlight from his previous quarterly report is the following slide:

With the following remarks:

We continue to see signs of slight improvement in markets as reliability issues from an overreliance on intermittent power sources emerge. On a broader level, we may be near a bottom in the long down cycle in commodities. The chart on page 5 shows the relative performance of a commodities index against the S&P 500. The ratio is at its lowest level in 50 years.

Considering that to recent memory he hasn’t reflected upon the valuation of the broad commodity environment (he has commented on relative valuation of various power generation methods), this was worth noting they’d take 10 seconds to dwell upon it. ATP does hedge natural gas exposure with commodity futures so it isn’t entirely unrelated.

Atlantic Power is a relatively boring company from a cash flow perspective – a lot of it is locked in, so most analysts leave it alone since they believe the market has predicted the future of the company with the stock price – indeed, there are only three covering the company. The downside appears to be relatively low, and there does appear to be a few pathways for upside. So I continue to hold.