When a company pays back debt, its enterprise value drops (or more specifically, the cash generation which leads to debt paydown is the cause of the enterprise value decrease because EV is market cap minus net debt, but I’ll insert this in before somebody comments on my illogical statement!). All things being equal, when material amounts of debt are paid back and the underlying entity is cash flow positive, it should eventually reflect an increase in market capitalization. This process sometimes takes a long time.

Atlantic Power today announced a revision to their credit agreement, which dropped the interest rate payable by another 25 basis points (to LIBOR plus 250bps), and if they can get their leverage ratio to less than 2.75:1 then it will go down another 25 basis points further. Atlantic Power had US$400 million in term loans outstanding in September 30, 2019 so this will result in somewhat less than a million a year in annualized interest rate savings going forward.

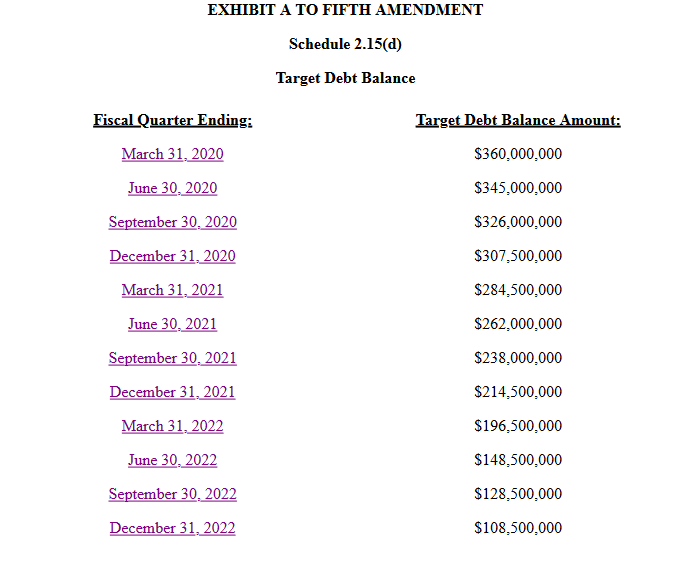

Reading credit agreement amendments (original April 13, 2016) might not be exciting, but sometimes a few nuggets of information here and there come out which are interesting. Section 2.15(d) of the agreement has the following debt paydown table:

The term loan component is extended to April 2025 which completely eliminates short term credit risk. The de-leveraging is mostly finished. The question is when the market will start to price in equity appreciation – after 2022 the company still has 12 power plants that are under power purchase agreements and generating considerable amount of cash flows.

I’ve been following ATP closely and steadily increasing my position over the past 6 months. However I only give so much weight to their debt repayment table. They repeatedly say how they are always looking at acquisitions and I can’t imagine they won’t use cheap credit to buy if the right opportunity appears.

My guess (as you’ve stated before) is that introducing a dividend will really be the catalyst that draws interest to this company. Not holding my breath yet…

Current management thus far has shown themselves to be relatively prudent stewards of capital, so I trust that if they do employ the revolver that it will go for shareholder benefit. They also openly stated that if somebody wants to buy the company, they’ll sell at the right price. Their investment hurdle rate appears to be around 15% from what I can glean, and they continue to park cash in their own preferred shares, which considering the roughly pre-tax 10% rate they get on it, is not a bad decision.

ATP filed their January share buybacks – 1.703 million shares at roughly US$2.36 a piece, this is their largest buyback in quite some time. Would be equal to a US 3.7 cent per share dividend if they gave it that way, instead shares outstanding went down 1.56%. At today’s closing price of US$2.41/share, it is up 2.1% from the purchase price, so reflected in the share value so far…..

EV is market cap minus net debt? That seems to be at odds with the standard formula (market cap plus debt minus cash)…

Ahhh, NM. I see what you mean by net debt.

Guessing ATP bought some more AZP.PR.A today.

A cross of 247,800 shares at $16.40 (7.39% yield, effectively 10% pre-tax) which will save shareholders about $300,000 a year in after-tax cash, assuming it is actually them doing it. They can buy back up to 384,700 shares this year. Guess the market for power generation out there isn’t that great if they’re spending $4 million on what more or less amounts to perpetual debt reduction.

Do you factor the reduction in EV in to your return calculation? Do you think we should?

My own model is devoid of any impact of future reinvestment of cash (aside from anticipated future debt reduction) until it occurs so every incremental improvement is a slight plus. For instance in this case, assuming the AZP.PR.A was actually repurchased, I’d throw in $300k less cash going out the door for preferreds. I don’t model interest on the cash balance either, I just assume it is a zero.

This is, however, the least exciting stock in my portfolio. You perform enough of these incremental cost reductions and eventually it will rise. Shaving off a quarter point on LIBOR – $1M/year at YR2019 debt loads, for example. All of these things add up. ATP also has a large tax shield which doesn’t materially start to expire until 2028.

I guess I was thinking for every share they purchased today, they reduced the EV by $25 for $16.40. Doesn’t that value of $8.60/share also accrue to the equity holder?

Accounting-wise there would be a gain, but unless if you’re winding up the company it isn’t really relevant, the PV of the cash outflow reduction is.

Doesn’t it reduce EV same as paying down debt?

EV calculations typically don’t involve preferred share as debt. If you’re doing some calculation on the basis of liquidation value then the preferred share value is much more relevant.

…

Sacha,

Do you use or know of a way of getting email alerts when a company files SEDI reports? That system is cumbersome to constantly be looking through despite the useful information you can sometimes find on there. Thanks!

I subscribe to CanadianInsider for this. Perhaps they should give me a referral fee!

James Moore (CEO) picked up 25k@US$2.22 bringing his ownership to 1.08 million shares.