Today is the start of these newly-found daytraders getting flushed out of the market.

What has happened is that apparently half of the cohort of unemployed people have entered into the casino known as the stock market with their unemployment/CERB cheques (this is a bit hyperbole – $2k isn’t going to move the market too much, but when you consider $43 billion in CERB has been handed out so far, not a trivial amount of money!), signed for accounts on RobinHood and WealthSimple, and suddenly turned into stock market geniuses buying shares of companies in Chapter 11. This is a by-proudct of many factors but very loose monetary policy is one of them. When you couple this with every institution on the planet trying to get into equities because they can’t make a return on their fixed income portfolios anymore, you will have days like today where the people with less conviction get flushed out.

Throw in a spooky headline like this:

Second wave! Second wave! Fear the second wave! Must sell because the news is bad!

Anyhow, this is why I suggested to lighten up last Friday and take some chips off the table.

This isn’t going to be a one day thing, the effect of flushing people out of the market involves having sharp down days (people getting caught long), and sharp up days (people getting caught in cash). This process rinses and repeats until monetary policy eventually kicks in, swamps the whole system with liquidity, and this gets pumped into the asset markets once again. Things are a lot faster than they were 22 years ago when this sort of thing happened in 1998 after the LTCM bust, but I’d guesstimate a week or two before the flush is completed.

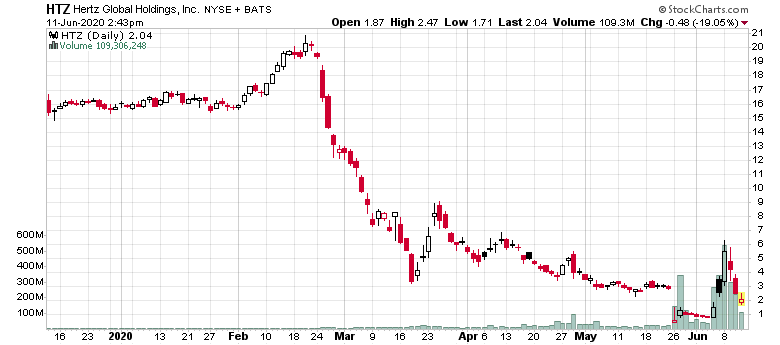

I’m going to use Hertz as an example.

Visualize this. The equity of a company like Hertz (Chesapeake, Pier 1, etc., you name it) is fundamentally going to zero after it restructures out of Chapter 11. They have a fixed number of shares outstanding that are trading, and they have to be somewhere. Just because people sell it doesn’t mean the shares vanish – they are transferred to somebody else. The same goes for the cash. The only difference is that the asset value (the stock) changes.

Any sane institutional manager (I am not talking about the day traders, or high frequency traders that would have a rational reason to be purchasing the stock, but this would be for a very short term period) would have dumped out on Hertz equity if not on May 26th when Chapter 11 was announced, but they would have been guaranteed to bail out by June 8th, where there were 523 million shares traded and the stock topped out at over $5/share. Keep in mind that Hertz has 142 million shares outstanding!

So this leaves the question of – who the hell would want to own the stock after this? The institutional demand for Hertz equity will be zero – they are all cashed out and not interested in getting in. The answer has to be retail investors, where currently (at a share price of $2.10 as I write this) US$300 million of client capital is locked up. There will be some other retail investors that look at the chart, not even realizing what Chapter 11 means, and purchase the stock, and some of these retail investors will be able to get out, but you can be sure that the only bids you will be receiving will be of other retail investors, or short sellers covering the trade. (Edit: Or perhaps the RobinHood/WealthSimple brokerages simply are making a mint speculating off of their clients by selling any Hertz their customers buy and then they have a very cheap borrow!)

In these ‘flushing’ processes is that after it is done, the garbage of the market will lose asset value, while the entities that have value will later receive a wave of demand – aided in part with the cash from their sales of Hertz at US$5! The people remaining will be true bagholders, and will eventually flip the stock around to a diminishing pool of demand until it gets cashed out at zero once the Chapter 11 process is completed. The inevitable result – wealth gets transferred – from the buyers of worthless Hertz to the sellers, who will move the asset value into something (presumably) more productive.

I’m also very thankful I cleared out my VIX shorts at around 26 and change last week.

1998, LTCM… easy here, millennials are reading you. 😀

I hope the debentures start taking a hit….I would like to load up some more.

Watching Hertz lately… makes me realize that stock prices do not truly reflect value, at least some of the time.

What’s funny is they proposed in their bankruptcy filing to sell their stock at the market to raise money as it would be cheaper than raising debtor-in-possession financing. The ultimately irony is that if they did raise equity capital in Chapter 11, the funds would still go into the creditors’ hands…