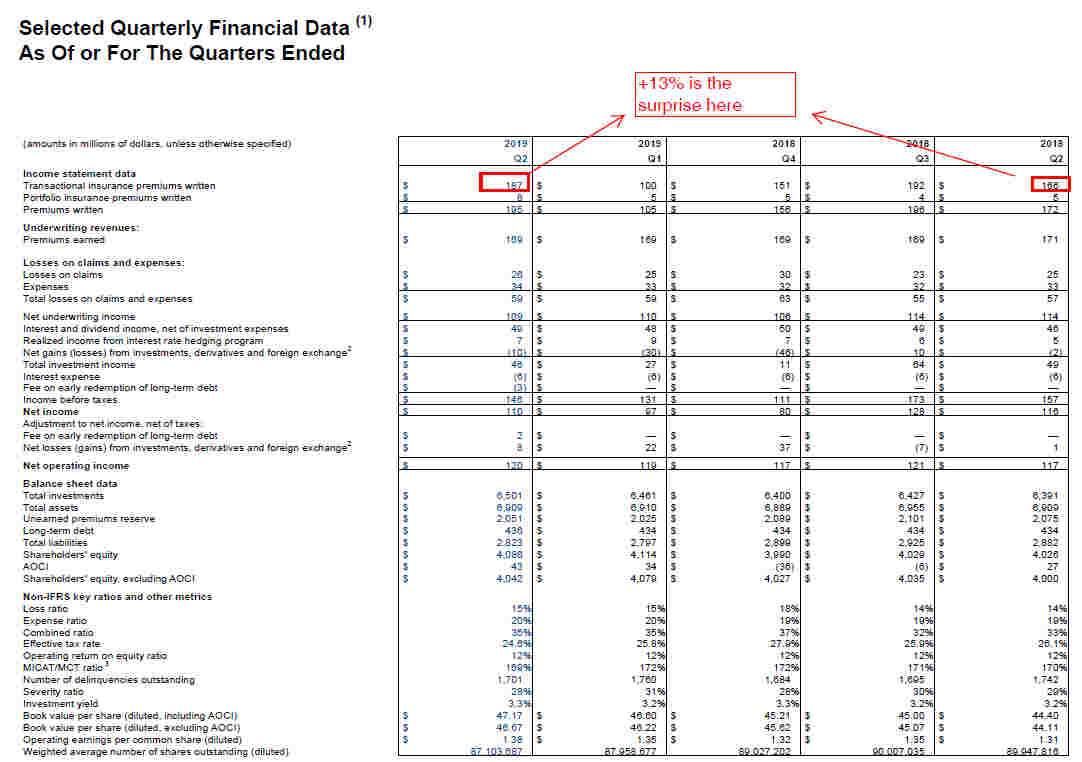

Genworth MI (TSX: MIC) yesterday announced their quarterly results. If there was one figure in the report that was surprising, it was the following:

I do not think many people would have expected year/year quarterly growth in transactional premiums growing. This is a fairly strong result, and would suggest that Q3-2019’s number will also be up around 10-12%. In the MD&A, it is cited that it is “primarily due to a modestly larger transactional mortgage originations market”.

With a combined ratio (loss ratio plus expense ratio) of 35%, Genworth MI makes 65% pre-tax margins on their written premiums – assuming that residential real estate market conditions don’t change.

With interest rates now being held low by central banks, this is a reasonable proposition.

The number of delinquencies also remains relatively steady, down to 1,701 from 1,760’s previous quarter – which is white noise given the 2.17 million units of real estate they have on the insurance books.

For Genworth MI, the good news has gotten even better. I thought this would be a story of ‘steady as she goes’, but things are surprisingly good. This probably is the reason why the stock is up some 7% at present.

However, all of this is overshadowed by parent Genworth Financial (NYSE: GNW) which is now actively trying to unload their 57% stake in the Genworth MI subsidiary. My original post speculated that they’d not get more than $50 from a transaction, but given today, I’ll shade this higher to around $55/share.

Any comments on Brookfield getting Genworth?

https://divestor.com/?p=8839

Don’t think my new post here has much value added. I’ll close this comment thread so if there are any remarks post it on the link above.

[…] will receive regulatory approval by the end of 2019. I had speculated earlier that Genworth would not receive more than CAD$55/share for the unit (and my initial opinion was CAD$50) and this appears to be right on the mark. Genworth […]