Skimming the Q2-2019 financial results of Kinder Morgan Canada (TSX: KML) –

Entity is 30% owned by the public (roughly 35 million shares outstanding) while Kinder Morgan (USA) owns roughly 81 million shares.

Because the public only owns 30% of the operating entity, even if the company reports $10 million in earnings, the public effectively receives $3 million. The $7 million is a “minority” interest (of course, this is no longer a minority!).

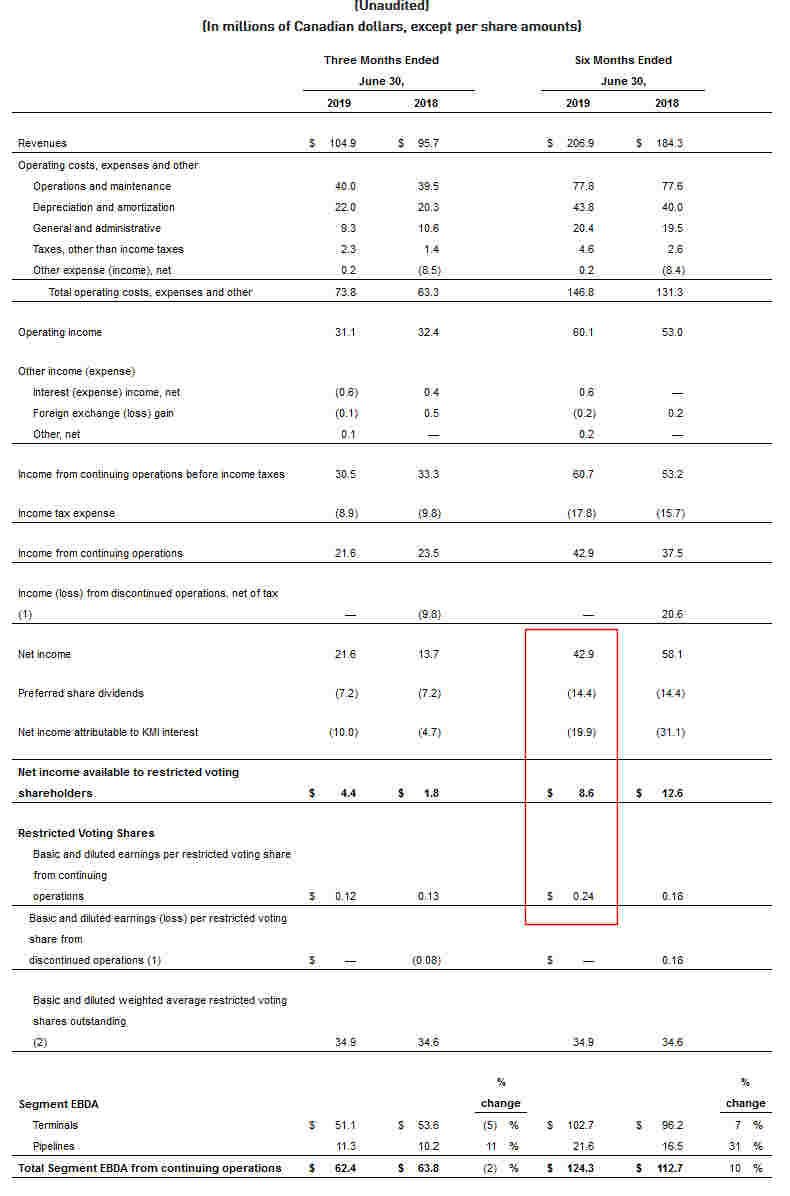

When looking at the first half of the year, we have the following (and I have highlighted the relevant area in a box).

The entity is pleasantly profitable – $43 million in net income for the first half.

However, the preferred shareholders (entirely held by the public) get the first slice of income. Their take is $14.4 million. This leaves $28.5 million for the entire entity. Kinder Morgan’s slice is $19.9 million. This leaves $8.6 million left for the 34.9 million shares that are publicly trading on the TSX – about 24 cents per share for the half.

Do some quick math – 48 cents a year for a stock now trading at CAD$12, which is a net return of 4%. It’s obvious this isn’t strictly about income, there is some pricing potential in the assets.

The preferred shares are at around 5.6%, and also get priority when KML finds a buyer at an acceptable price for their Canadian assets. The CAD$550 million is a drag on KML’s balance sheet, but they are virtually first-in line (as KML got rid of most of their debt after the Trans Mountain Pipeline sale).

For the most part, the income stream is stable. There will be some reductions in 2020, but otherwise they will easily cover the preferred shares.

I bought some preferred shares in early June as a cash parking vehicle. This is a very low risk, low reward type situation where you can watch paint dry for a maximum upside of par – and in the meantime, you can clip your coupons.

Is there change of control protection? Just wondering if the pref could be left stranded.

Nope, the fine print is typical for preferreds (as long as those dividends are paid the company can do anything it wants), although if it goes to liquidation then they get priority over commons. What if they pull an Aimia and sell off everything, do a giant dividend but keep the preferreds outstanding – up to the courts to decide if this was a constructive liquidation.

The likely scenario is if they sell out, part of it will be an offer/redemption at par, or the acquiring entity will just take on the preferred shares and continue paying.

I was able to pick up both preferreds, under 22 this week, thanks for the suggestion Sacha.

@Marc: You’ll be watching paint dry, but at least at a better and tax-preferred rate than a typical HISA. On Wednesday it looked like some guy really got hit with a margin call and these prefs got cleaned from his account on a market sell.

One thing I didn’t write about was the minimum rate guarantee. 3 years away from the nearest reset is a bit early to be thinking about it, but if the 5-year government bond trades under 1.6 and 1.69% (for the As and Cs respectively) it kicks in. Rates are 1.23% currently. There’s a pretty good chance there will be a liquidation event before then though.

Interesting idea – thanks. Does the equity appeal to you if it slides closer to $10? Thinking relatively safe ~4.5% with potential upside from a sale.

Thanks,

Kevin

@Kyle: Before I answer, can you explain how you believe it is a “relatively safe ~4.5%?” Thanks.

Aug 21 (Reuters) – Canadian pipeline operator Pembina Pipeline Corp said on Wednesday it would buy smaller rival Kinder Morgan Canada in a transaction that values it at about C$2.3 billion ($1.73 billion), as deals in the country’s midstream segment heat up.

Last week’s unsolicited bid for Inter Pipeline Ltd highlighted the potential of Canada’s midstream companies, which own key infrastructure such as gathering pipelines, gas-processing plants and storage tanks, to offer insulation from volatile oil prices.

Though such companies have been in high demand, and reported record second-quarter profits, they are sometimes overlooked, because of the wider energy sector’s problems of congested export channels and low prices.

The all-share deal values Kinder Morgan Canada at about C$15.02 per share, representing a premium of 36.8% to the stock’s Tuesday close.

Nice call Sacha

surprising today that KML.PR shares didn’t go up to $25 par value or am I missing something?

Posted thoughts on KML/PPL takeover here:

https://divestor.com/?p=8852

Will close these comments now. Post on the link above if you wish to chat. Thanks.