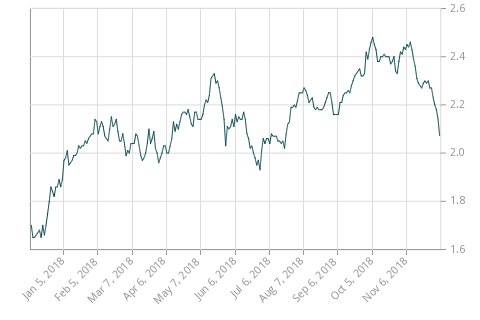

The Canadian 5-year government bond rate has compressed significantly:

As most Canadian preferred shares are linked to this rate, we are seeing a huge selloff (which interestingly took place about a month before 5-year interest rates really started to drop):

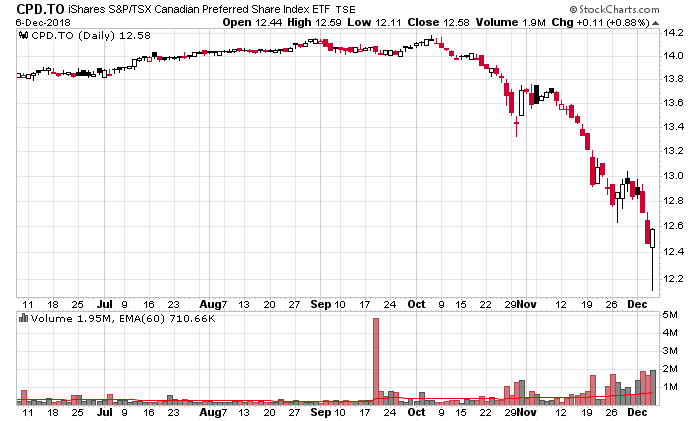

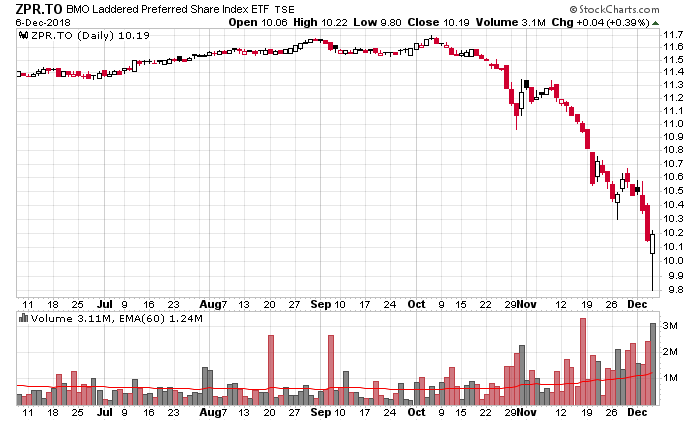

ZPR is a BMO ETF tracking preferred shares. CPD is an ETF tracking a preferred share index holding most of the investment grade preferred shares trading on the TSX (mostly concentrated in Financials and Energy). Holders in these “safe” funds will have had around 13-14% of their capital value evaporate over the past two months of trading.

It is indeed ironic how the equity components of the preferred share indexes have fared generally better – as an example, Toronto-Dominion equity has declined about 10% in the same period of time.

So much for preferred shares being a safer vehicle to invest in!

The big difference this time around is that a lot of the rate-reset preferred shares have already had their yields reduced to a minimum due to the 5-year Canadian bond rate being so low for an extended period of time. Subsequent rate rises will have less impact on the dividend rates paid for preferred shares.

It remains to be seen whether this will continue or not. Back in February 2016, we had seen double-digit dividend yields on very credit-worthy issuers, but this was also when the 5-year bond rate was trading at around 100 basis points.

I’ve also been doing some research on preferred shares that are not held by these two funds. I would suspect that less liquid preferred share series on the main two ETF indexes would be more prone to auto-selloff algorithms when people inevitably decide to panic and try to liquidate everything.

Very often, people hold cash in their portfolios for too long and then get itchy. They then instead think of investing in “safe” preferred shares, or an index, thinking that the 5-6% yield they realize is adequate compensation for the risk in lieu of holding cash.

It is these situations where they rethink this notion and decide to liquidate. Eventually the capital losses become too much to bear.

It is very difficult to time when the maximum moment of panic is, but doing so will result in outsized risk/reward ratios, which is why I’ve been paying careful attention in these very volatile couple months.

Do you think it makes sense for preferred yields to move opposite to bond yields? I think it’s perverse.

When they are linked to the very same rates via the rate reset? Yes.

Straight vanilla perpetuals? Nope.

What is interesting is that despite the flattening yield curve, floating rate preferreds in most cases are still discounted from the fixed ones. It is a lot better than it used to be, however.

I don’t understand why a rate reset preferred that resets in 5 years goes down when a 5-year Canada bond goes up. Why wouldn’t they move together with the same duration?

If you look at a longer term chart of CPD versus XIC you can see that the correlation between the preferred share market and the stock market itself is very tight. I think that preferred shares are reacting to the stock market much more than interest rates. In May/June of 2018 the bond yield fell almost as much as it has in the previous couple months, yet preferreds barely reacted. I would guess that investors are treating preferreds more as stocks than bonds and are making a rather large mistake.

Is a list of Canadian fixed rate reset PF’s with all relevant info available such as Dividends, terms of reset etc?

CIBC’s reports are pretty good.

https://www.cibcwg.com/c/document_library/get_file?uuid=34cb7dd9-a90b-44e2-bb59-b1af4196da4f&groupId=82580&version=1.0

Sacha, when I follow that link I get a 8 month old report…..is that what you intended. If you trade or invest at CIBC, do you get a more recent report?

I don’t but I do find their reports (when they can be found) are quite comprehensive with the various ticker symbols and the relevant reset parameters.