(rest assured, I have never been paid to post anything on this site, and this will pleasantly continue)

ETF marketing is clever as always. Did you want a 13% yield? Introducing the Hamilton Canadian Financials Yield Maximizer ETF!

They politely inform you that they are “Canada’s Highest Yielding Financials ETF”, featuring a “13%+ target yield”.

Not just 13%, 13%+.

Who can resist?

They also inform you, in bold font, that “HMAX does not use leverage.”

Is this a dream come true?

Digging into the much dryer prospectus, we get the following:

HMAX will seek to achieve its investment objective by investing in the top ten Canadian financial services stocks by market capitalization (each, a “Financial Services Company”, and collectively, the “Financial Services Companies”).

…

To mitigate downside risk and generate income, the Portfolio Adviser, in conjunction with the Sub-Advisor, actively manages a covered call strategy that will generally write at or slightly out of the money call options, at its discretion, on up to 100% of the value of HMAX’s portfolio. Notwithstanding the foregoing, HMAX may write covered call options on a lesser percentage of the portfolio, from time to time, at the discretion of the Portfolio Adviser. The Manager has retained Horizons to act as sub-advisor to HMAX solely in respect of the writing of such covered-call options on its portfolio securities. HMAX’s strategy seeks to generate attractive option premiums to provide increased cashflow available for distribution and reinvestment, downside protection, and lower overall volatility of returns.

Here lies in the secret sauce. They invest in highly capitalized Canadian financials, and then try to make up the differential with selling call options. You can actually replicate this fund at home if you wanted to.

Here’s the problem. Essentially the fund is taking the worst of both worlds of split share funds and covered call ETFs.

The call options simply aren’t going to make that much money, especially if the fund starts to scale up in size.

The top holdings of the fund is the Royal Bank, at 23%. The “big five” Canadian banks consist of 71.4% of the fund. If your throw in National, it’s over 3/4 of the fund. Let’s concentrate on Royal.

Royal Bank has a 3.9% dividend. So you need to make up 9.1% over the course of a year to get your quota.

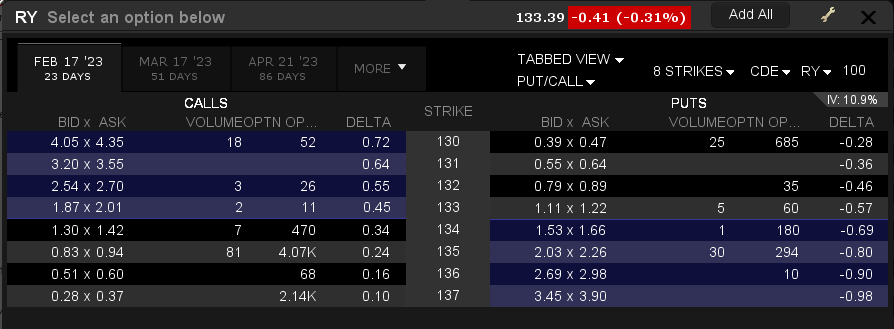

The front-month for Royal Bank options is trading at a Black-Scholes implied volatility of 11%:

So your strategy is to buy stock and sell the next nearest strike at the money, which in the case of RY would be a 1% premium over 23 days (16% annualized!). If you take the next month, you get a 2% premium over 51 days (14% annualized!).

The math goes like this – you repeat this every month and you suddenly earn 3.9% in dividends and an additional 12% yield, you can “easily” get to your 13% quota. Free money!

Forget about capital upside with this strategy – it is a guaranteed “ratchet” that can only click down in price.

Let’s tear this apart a bit.

The above chart is the 30-day historical volatility of RY and the implied volatility. The IV index in this chart is normalized to fixed tenors (30, 60, 90, 120, 150, 180 days) using a linear interpolation by the squared root of time, and does not represent the “spot month”‘s implied volatility, which is why the IV index is higher than the front month at the moment.

The point I am trying to make here is that covered calls are being sold cheaper than the likely actual forward volatility of the stock.

Most, if not all, of these covered call strategy funds are, at their core, leaking value through selling call options below intrinsic value because the covered calls are being sold blind to their value. The same style of arguments have been levied against index funds in general in regards to the price insensitivity to the equities in their respect indices. I am sure the initial covered call fund realized a reasonable semblance value, but when you have hundreds of millions or billions of dollars of assets under management employing a strategy into a less than robust Canadian options market that is not going to fundamentally support the liquidity, the response is that the option market makers are going to price the options cheaply.

This is not limited to Hamilton Funds, there is plenty of this going on in the overall marketplace. Volatility can be ‘harvested’ by selling theta on a variety of securities out there. It appears like “free money”, until the market rips up.

Essentially is the other side of the market will be able to “rent” the stocks for relatively cheap rates.

What I project happening is that this fund will discover that making its 13% quota through covered calls will become progressively more difficult to achieve and inevitably distributions will come from return of capital to make up the difference. While the fund will be able to distribute its mandated $0.185 monthly distribution, it will come at the cost of its capital value. It will take a few years for this effect to be apparent.

The easiest way to measure this effect over time is to make a comparable index basket with just strictly the equity (with dividends reinvested) and no derivative trading on the portfolio, and compare the performance between this index and HMAX.

Notwithstanding the 0.65% MER, I predict that the index of straight equity ownership would outperform. This is the inevitable result of employing price insensitive derivative strategies.

However, I have to commend Hamilton for their marketing. I am sure there will be another fund along the way that will promise 15% returns, and 20% returns, and 25% returns until it all busts. This is kind of reminding me of the chase for yield that occurred in the mid 2000’s when you had a huge proliferation of Canadian income trusts going public, which many of them were simply return of capital vehicles.