Words you never want to hear if you’re an equity holder:

Xebec Adsorption Inc. (TSX: XBC) (“Xebec” or the “Corporation”), a global provider of sustainable gas solutions, announces that it will file today an application with the Superior Court of Québec (the “Court”) for an initial order (the “Initial Order”) under the Companies’ Creditors Arrangement Act (the “CCAA”) and seek recognition of the Initial Order in the United States under Chapter 15 of the Bankruptcy Code.

Since Xebec isn’t exactly a household name, here is a description of the business:

Xebec Adsorption Inc. (“Xebec” or the “Company”) is a global provider of clean energy solutions and specialized in the design and manufacture of cost-effective and environmentally responsible purification, separation, dehydration and filtration equipment for gases and compressed air. Xebec’s main product lines are biogas upgrading systems for the purification of biogas from agricultural digesters, landfill sites and waste water treatment plants; natural gas dryers for natural gas refuelling stations; associated gas purification systems which enable diesel displacement on drilling sites; hydrogen purification and generation systems for fuel cell and industrial applications; on-site oxygen and nitrogen generators for industrial, energy and healthcare applications; and services for compressed air and gas businesses.

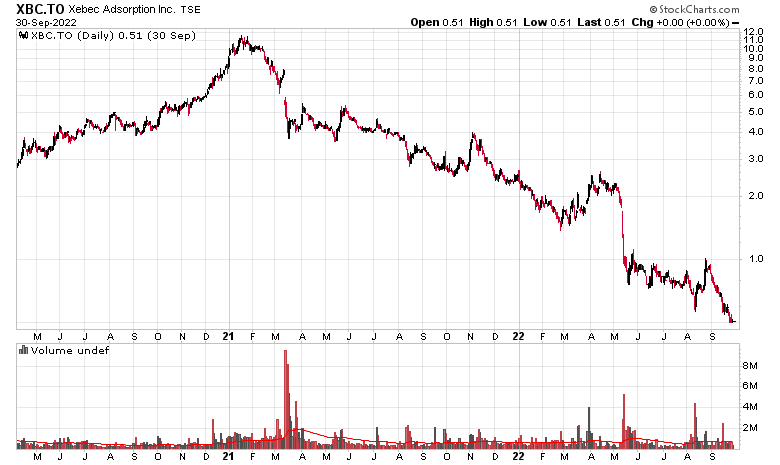

Since the beginning of 2021, the stock chart does not look pretty:

At its final demise, the company had 155 million shares outstanding, which means at 51 cents per share, it still had a market cap of about 79 million.

Financially, the company was bleeding cash this year and they had blew a covenant on their credit facility (their total liabilities to tangible net worth ratio was exceeded) and thus people reading financial statements would have had some sort of hint this would happen. Goodwill and intangibles amounted to $237 million on their balance sheet, while total equity was $260 million and needless to say the $42 million in net losses for the half year tipped the balance.

It is not a complete loss, however – they have $50 million of cash and restricted cash on the balance sheet, offset by $85 million in debt. While their business is awful (gross margins were less than 10% of revenues in the first half, while SG&A was about 40%!), balance sheet-wise it is not a huge train wreck. Perhaps after restructuring they might make a better go of it, but I doubt equity holders will get any recovery from this one.

While the increasing interest rate environment will likely contribute to further CCAA and bankruptcy filings in the future, in the case of XBC, this one looks to be entirely by self-inflicted wounds. The business isn’t profitable.

I did not own any shares at any time.

It will be interesting to see how many of the fully renewable utility/energy companies are viable with higher rates? I suppose same will be said for any indebted company that isn’t renewable. Algonquin sure didn’t do we’ll latest quarter.