This is a quick refresh of the Divestor Canadian Oil and Gas Index (DCOGI), created on February 5, 2021.

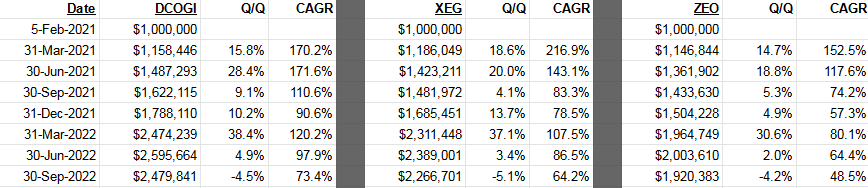

From a notional 100 value on February 5, 2021, it ended Q3-2022 at 248, working out to a 74% CAGR.

It has fared well against its ETF competitors, XEG (index: 227) and ZEO (index: 192), although the latter has 40% pipelines and will be lower return and should be lower risk by design. Both ETFs, however, have a 60bps friction involved in the form of MERs.

The DCOGI has suffered its first quarterly loss, losing 4.5% for the quarter. Perhaps when WTI crude goes from CAD$130 to CAD$110/barrel had something to do with it (not to mention the increasing WCS-WTI differential).

Of note is that dividends received year-to-date in the DCOGI have amounted to 8.2% of the original cost base. This will likely increase in the future as Birchcliff Energy has indicated they will raise their dividend from 2 cents to 20 cents quarterly starting in 2023, and I speculate Cenovus will probably double theirs at the same time. CNQ and Tourlamine have given special dividends, while ARC and Whitecap will continue to raise as they achieve specific net debt amounts.

The only dividend holdout is MEG Energy, which continues to buy back its own debt at a frantic pace from the open market – at quarter-end they disclosed a US$97 million debt purchase of their 7.125% 2027 notes. Of note is that this issue was US$1.2 billion at the end of Q1 and at the end of Q3 is US$735 million outstanding. They have a stated capital allocation goal to dedicate 75% to debt retirement and 25% to share buybacks until their net debt goes below US$1.2 billion, after which they will go to a 50/50 model. They will transition to 50/50 sometime in the 4th quarter.

I struggle with the financials on the pipelines. TRP for example every year debt and share count rises. Their book value is basically the same over 10 years and their fcf 10 yr cagr is -1.9% (quickfs.net). They keep raising the dividend but with the increase share count the amount paid is growing faster. I just don’t see why they are so favoured. Am I misreading the data Sacha? Not looking for a breakdown just a simple yes you’re wrong 🙂

FCF is low simply because they spend a ton of CapEx on new pipelines. Your general concern over their balance sheets, however, I agree with. I’m not a fan of pipeline equities at current pricing myself.