Sometimes an investment stares at you in the face and it is so obvious that it makes you wonder why others do not see it this way.

This is the case with Birchcliff Energy (TSX: BIR). Now that it has appreciated well beyond its Covid lows, I’ll write a little more about it in detail. I’ve been long shares of this (both common and preferred) for quite some time.

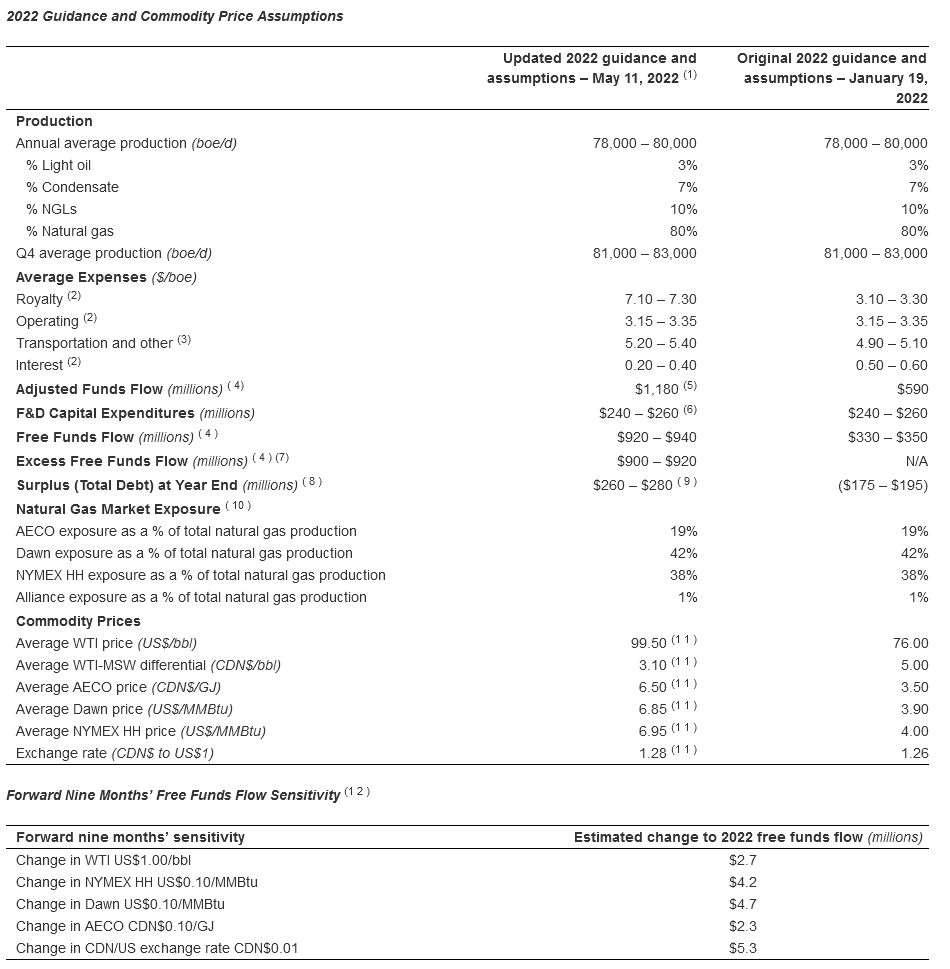

In 2022 it will produce about 79,000 boe/d equivalent (exit 2022 at approx. 82,000 boe/d), of which 80% of it is in the form of natural gas. All of this production is in the northwestern Alberta area, right up to the BC border.

Thus, the primary driver for this company is the state of the natural gas market. It has exposure to Dawn, Henry Hub and AECO.

Birchcliff is an unusual company in that they do not host quarterly conference calls. Instead, they issue information through large press releases and make it very easy to look at the assumptions. Although I have no problem sharpening my pencil and doing the leg works to do a proper pro-forma projection given various commodity price environments, Birchcliff expedites this process considerably.

There is some fine print to wade through, but the point is that BIR will generate $910 million in “excess free funds flow” (effectively cash flows after capex and projected dividend payments) with the average commodity prices as displayed in the release.

Notably, spot WTI and the spot Henry Hub price is well above their assumptions (US$114 and US$9.2 as I write this). Dawn typically tracks Henry Hub. Let’s ignore that spot is higher than modeled rates in the press release.

$910M of “excessive free funds” translates into $3.43/share.

At Wednesday’s closing price of $11.56, that is 3.4x or a yield of about 30%.

Normally companies are constrained with leverage and debt servicing. At the end of 2021, Birchcliff had $539 million in net debt (which includes BIR.PR.C) and another $50 million for the redemption of BIR.PR.A. The redemption of the preferred shares will result in a $6.8 million annualized savings on dividends (3 pennies a share, every bit counts!).

This will leave the company with a positive net cash amount of $270 million at the end of the year (the “Surplus”), unless they decide to blow some money on acquisitions and the like. Importantly, the math does not have to be adjusted for a leveraged return (indeed, it has to be corrected in the opposite direction).

The company will also be making enough money to eat through most of its tax shield ($1.9 billion at the end of 2021) and start paying income taxes in 2023, if the current price environment continues. Still, at US$88 oil, and US$5.50 Henry Hub for 2023 assumptions, the projection is for $535 million or about $2/share in free cash flow.

The stated policy on what to do with the cash surplus is to dividend it out beyond that which is to be used for strategic purposes. Management does not appear to be big on share repurchases other than to offset dilution that which has been issued from option plans (which is a real cash cost and will drag cash flows accordingly).

They will increase the dividend to $0.80/year in 2023, which is a $212 million outflow. This dividend can be maintained at price levels that are unlikely to be seen barring a great depression.

If they dividend the rest of their cash flows, when plugging in current commodity prices, they can give out far more than $0.80/year in dividends. It would be closer to around $2.80, or about $0.70 per quarter. Needless to say, if this is what they did, the market would find the yield (24%) tough to resist.

This is a very similar situation to Arch Resources (NYSE: ARCH), where the company will be giving out half of its free cash flow as a dividend and the other half to buy back shares. Considering its Q2 dividend will likely be around US$11/share, the obvious value of a share buyback is apparent. I wish Birchcliff would more actively consider it, at some cut-off threshold. For example, they can buy back shares until the price gets to a point where it is at 15% projected long-term free cash flows, a very conservative metric for a beneficial buyback. Right now that would imply that buying back below $15/share will clear that hurdle. At 12%, that number is about $19/share. There’s quite a way to go from current market prices.

None of this is a huge secret. It’s all in plain sight. It all relies on elevated commodity prices.

Thanks for the update Sacha…you haven’t posted on BIR in quite a while.

Good stuff, thanks Sacha.

I looked at the analyst recommendations on this. 16 buys, 3 strong buys, 3 holds. Clearly the analysts are already “in”. What about insiders?

https://www.marketbeat.com/stocks/TSE/BIR/insider-trades/

No insider sales during COVID, but now selling has ramped up. 300,000 shares sold this year. What is it that they are seeing? Is it just profit-taking? One of the insiders has sold half of their holdings.

I think that the energy markets could stay robust for quite some time because of Russia/Ukraine but perhaps others are less sure of that.

Almost every fossil fuel company has seen significant insider sales. After this much of a run-up (especially being beaten to a pulp from 2014-2020) it would be shocking to see if insiders did not take some chips off the table.

BIR.PR.A & BIR.PR.C : Intention to Redeem

https://prefblog.com/?p=43588

This was already announced in BIR’s last quarterly report.

This means the best GIC alternative is off the market. First DRM.PR.A and now this. So sad!

I expected some volatility in natural gas prices, but would never have guessed that US prices would fall by 80% from its recent high. And this with the war in Ukraine still raging. The company lived up to its promise to raise its dividend, but now the question is whether it can maintain it.

Not at current gas prices. Fortunately for them, they managed to get rid of most of their debt and are mostly a de-leveraged entity now. My model has them about $50 million short of their dividend at today’s average strip pricing. But it is really sensitive to that HH/Dawn pricing. The market seems to think it is temporary as well given that EV/FCF has gone from like 3x to (my estimate) 12x today.

Thanks for the estimate Sacha. Are you assuming a reduction in capex spending from the midpoint forecast of $270 million they publicized?

I just stick to the assumption that Capex will be the mid-point of their range. I am particularly interested in the capex to maintain production, but you can only indirectly infer roughly what it may be.

Also my prior comment I made a memory error, when I wrote it my model was $30 million short of the dividend, not $50 million.

And what a difference a day makes, at today’s HH strip, my model now has them barely able to cover the dividend. Goes to Stusclues’ comment below about the volatility of natural gas pricing.

“I expected some volatility in natural gas prices, but would never have guessed that US prices would fall by 80% from its recent high.”

Why not? Wild swings in O&G prices are the norm, not the exception. O&G prices are highly sensitive to far too many moving parts to ever get very comfortable about future prices – and, therefore, too attached to a specific narrative about the future.

You’re right. I am new to the NG world, but as this chart shows, price declines of 60%+ have occurred about once every two years in the past twenty.

https://www.macrotrends.net/2478/natural-gas-prices-historical-chart

Which makes me wonder what Birchcliff was thinking when it promised the dividend raise?

I know, right? O&G companies really ought to make better use of special dividends IMO. Establishing fixed dividends usually ends in tears and/or too much or too little FCF leftover. Much more common is the share buyback which too often (not always of course) ends up destroying shareholder value.

You have to keep in mind when reading these charts they use spot pricing, which will organically display volatile price swings between the January and July months, for example. June to December this year is about $3 and $4, respectively.

Stusclues is right, especially about companies buying back stock at cyclical highs. BIR only buys back stock to offset option issuances. ARX on the other hand…..

Just to tell you how volatile this is… Now the HH strip and spot WTI has BIR making $1.11/share (hence easily covering the 80 cent dividend).

Now BIR’s $0.80 dividend seems like a stupid idea. Even with OPEC cut, natural gas is still down.

They are projecting basically $0 of Excess Free Funds Flow for 2023.

CEO was very cocky on BNN last year about no hedges and increase of dividends, there is no way they will acknowledge their mistake and cut them back.

If natural gas prices stay depressed, isn’t it a recipe for disaster?

Right this very second, they will be about $70 million FCF negative with the dividend factored in.

At 2024 HH strip, they will be able to cover the dividend.

Since they delevered so extensively in the past couple years they have the luxury of deferring capex and waiting for CGL and the other North American LNG projects to get online.

You’re right, they likely won’t back down on 80 cents but this investment has effectively turned into a high yield income trust linked to NG pricing. Treat it as such.

It’s kind of comic but yeah, they won’t cut the dividend because that’d mean they made a mistake. This is an argument for having ChatGPT run the executive suite 🙂