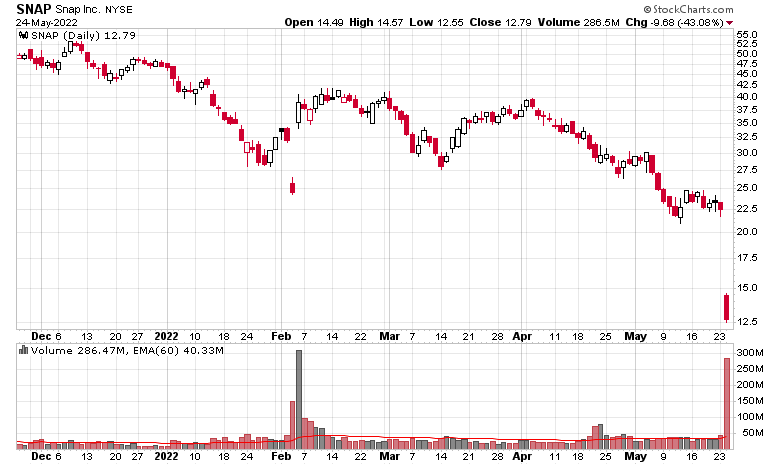

I look at the carnage going over in technology (today’s slaughterhouse featured SNAP, down 43% on an earnings report I never bothered to read) and ask myself if I am vulnerable to any of this.

I am guessing all of the tech-driven spending, including advertising, is just falling off the proverbial cliff. Everybody’s starting to tighten.

Economically, experiential spending will dominate 2022 (hospitality/entertainment) entirely due to Covid, the deferment of this type of stuff for the past two years is causing this year’s demand.

Just get on Expedia and look up prices of car rentals and hotels, they are higher now than I have ever remembered them. Just as an example, looking here in the Vancouver area, your average 2.5 star hotel is going for roughly C$250/night plus taxes (domestically), and it isn’t even peak summer season yet. Car rentals are $100 a day, even for a compact vehicle.

The demand/supply dynamic is causing these huge price spikes. People have money to throw at ‘experiences’, while providers are short-staffed and facing the same increased costs for labour, supplies, food, etc., hence everything is going to be at a premium.

This goes on until people’s money runs out.

2023 will probably be a better time to take a vacation. After all these tourist agencies increase capacity they will discover that nobody’s coming next year.

The flip side is that discretionary goods in the second half of this year will go on a huge sale. Home renovation season this summer will be totally dead.

Portfolio-wise, the best thing for me to do at the moment is to just sit on my rear end and take no action. It helps when I do not own anything like SNAP, although I do note the closest thing I have to a technology holding is down about 30% peak to trough. I am not particularly concerned for this holding, which used to be my largest last year. What happened instead, however, is that fossil fuels started to take over the portfolio through appreciation.

I see people switch from large cap to small cap energy names, but I am quite happy with the mish-mash that I’ve selected from my DCOGI index. I have no desire to deal with the sub-50k boe/d sector.

As long as the commodity price environment continues, these companies will continue to make a fortune. It will get to the point where governments will try to steal more shareholder profits and when they start to make their cash grabs, it probably will signal a time to lighten.

In the meantime, I think the fundamental argument for oil and gas continues to be very good. Chronic under-investment since the 2014 boom for various reasons (economics, ESG, Covid) has significantly changed the demand/supply dynamics in a manner that will take years to rectify itself. Only now some people are dimly waking up to the possibility that “renewable energy” is not going to be replacing fossil fuels in any substantive amounts and that there is an insatiable and growing demand for energy. This energy is functionally a first claim on any input in society – even before the taxman, which is saying a lot. You only generate taxes through income or consumption and you don’t get either without energy!

Totally agree on the vacation! We haven’t had a vacation since covid began, and were thinking of spending a week in Banff / Jasper area. I knew the hotels in the area are not cheap, but the prices I’ve looked are beyond insane! 1k a night for a 4 star hotel? 450 CAD a night for a rented condo some 20km outside of Banff?

Regarding Canadian O&G – BC already pioneered the movement by increasing royalties: “But those resources, (we) have to be reminded every now and again, belong to all of us. And for too long, the system of royalties for oil and gas has set us up to a situation whereby rather than British Columbians benefiting completely from these resources, we’ve seen extremely large profits for oil and gas companies, while British Columbians have had to pay more for their heating costs as a result.”

BC, of course, is known of its irrational attacks on O&G sector, so I’m more interested in Trudeau’s reaction.

Btw, speaking of portfolio diversification: I know you are not a big fan of financial sector, but I would start looking at insurance companies right now. Recent Manulife 10% drop on their very honest and extensive IFRS 17 disclosures only demonstrates that analyst and investor community does not understand IFRS 17 at all! And while ROE, EPS and other earnings-driven benchmarks are going to be affected at transition, the cash side of business stays the same as before + favorably affected by increased yields on investment portfolios.

I would not be surprised to see top 3 lifecos repurchasing shares like crazy in 2023 onwards, as I’m pretty sure these companies are going to be hit hard by general market before it really gets an idea that IFRS 17 is just an accounting headache (similar to what new Leases standard was a couple of years ago).

Yup, just like how IFRS 16 (leases) did not change the economic substance, but for non-accountants it is yet another annoying thing to make financial statements even more unreadable!

I’ve been eyeballing MFC/SLF/GWO/etc., relative to the big banks (TD, RY, etc.) I like the insurers a lot more, but don’t have any position in them. If I had Buffett constraints (e.g. a billion minimum), MFC sure looks attractive…

Same here, I’m treating MFC and GWO as defensive stocks to cover more risky positions in my portfolio. Both have a significant upside potential however, especially after inevitable drops as a result of transition to IFRS 17 in Q4 2022 – Q1 2023.

When you have folks like Klarman buying Google and Dropbox maybe it is time to lighten on energy and dip ones toe into the tech sector carnage… maybe.

I would not be shocked to see a ‘summer of fun’ for tech, especially in relation to the lows they had, before it continues to head downhill again. I am sure that whenever the whole sector hits the “baby flushed out with the bathwater” phase that there will be great bargains to be had, but I honestly don’t believe that even with the price corrections we have seen that much of the sector constitutes a good value as of yet. There may be a few niche companies here and there that prove to be the contrary at present (CRVL, talking my book) but why bother buying at 20x when there’s a reasonable chance everything goes half-off again next year?

with today’s announcement in England about windfall tax on O&G companies to fund a energy rebate to consumers one wonders if Liberals/NDP will follow suit. Not looking forward to my Enbridge rates for upcoming winter heating season (mind you have held Enbridge shares for a decade so that helps)

The tools the feds have are more blunt than the Brits, mainly because of the divisions of powers in the Canadian Constitution. Perhaps they can raise the carbon tax further, that’ll solve the issue!