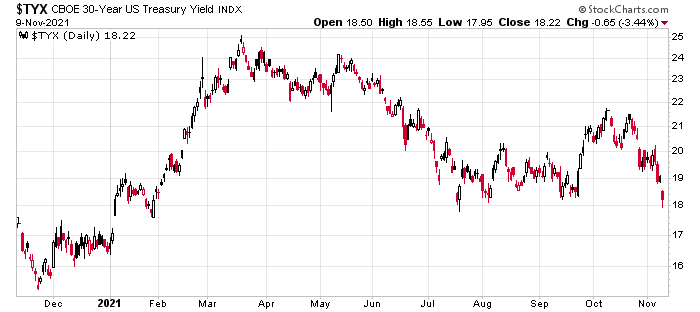

If we’re going through a period of mass inflation, then how come the 30-year treasury bond (at least the American one) is at 182 basis points yield?

The “long term” Canada government bond yield is sitting at around 198bps on November 8, 2021.

Even though short-term rates are projected to rise in 2022, you do not see this in the long-term bond yields.

A flattening yield curve does not bode well for the overall state of the economy.

There will be a day when simply holding cash will beat all the other asset classes. I don’t know exactly when that will be (indeed, anybody holding a good chunk of cash over the past 18 months, scared by Covid-19, will have made a catastrophically bad decision) but when it happens it will be swift and surprising to many.

In the meantime, the party continues.

The market seems agree with the Fed and Macklem, current inflation is sticky but ultimately transitory. Deflationary forces are still real and CBs will do whatever it takes not to let them take hold. CBs also need to fight (and are fighting) the narrative that low rates are “guaranteed” for a very long time in order to make market participants more sober about taking on debt.

I checked to see whether this might be driven by Fed purchases. It looks like the Fed owns about 20% of the outstanding at long maturities. Hard to model what that might do to prices – it doesn’t “feel” like enough to really compromise price-setting. You don’t expect goods markets to be seriously noncompetitive because there’s a single 20% player. And the Bank of Canada owns barely anything out past 8 years, so they’re not really directly distorting long-bond prices either.

On the other hand, you get articles like this https://www.ctvnews.ca/politics/little-room-for-feds-to-issue-long-term-debt-unless-central-bank-steps-in-documents-1.5613335 saying that the government is consistently feeling out debt markets and unwilling to issue more long-term debt because it might raise yields notably, which suggests that the holdings are not by price-sensitive individuals but mostly very passive holdings that don’t care about yields, in which case the market signal is pretty dulled and we shouldn’t trust it in terms of expectations.