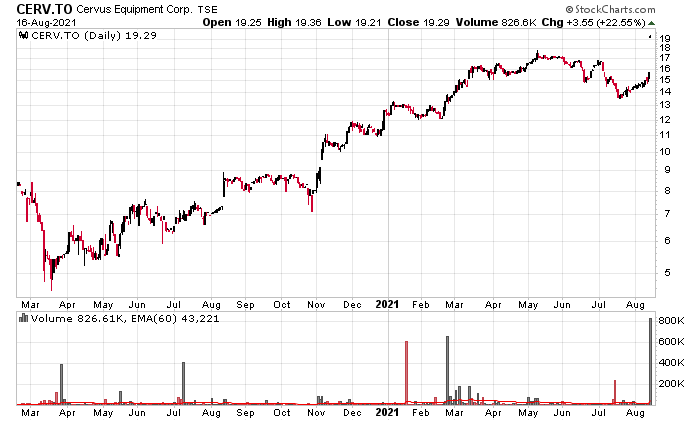

It has been an exciting 2021 with my third company getting receiving a takeover solicitation. Cervus Equipment (TSX: CERV) announced it was being acquired by Brandt Tractor for CAD$19.50/share in cash.

This is still a dirt cheap valuation.

Not surprisingly, they want to close the deal pretty quickly:

Cervus expects to hold the Special Meeting of shareholders to consider the Transaction in October 2021 and to mail the management information circular for the Special Meeting in September 2021. Subject to the conditions set forth above, the Transaction is expected to close in the fourth quarter of 2021.

A two-thirds vote is required, with the chair holding 18% of the stock, coupled with Brandt holding another 9%. Unless if there is some organized opposition to this deal, it looks like it is going to proceed.

The price that is being paid is cheap. CERV has 15.4 million shares outstanding and from the first half alone has generated about $1/share in earnings. Cash-wise, in the first half they have generated about $23 million (about $1.5/share) in free cash. Full-year, they’re probably going to pull in something around $2.50-$3.00/share. Balance sheet-wise, they are at around $40 million net cash, and approximately $13/share in tangible book value, or $16.85 if you include the intangibles and goodwill. Brandt is paying a slight premium over the balance sheet value, but given the earnings power of the company, they are getting a very good price. It is too good a price.

A fair deal would be around $23-24 in my estimation, but who am I to say?

There is some precedent for a small boost up in price – Rocky Mountain Equipment (formerly TSX: RME) was taken over in the middle of the Covid crisis last year for what could be considered a total steal of a price. The original all-cash $7.00 management takeover was boosted to an all-cash $7.41.

In a final slap in the face, the following:

Pursuant to the Arrangement Agreement, the Company has agreed not to declare or pay any common share dividends until the completion or termination of the Transaction.

That said, overall, if the deal goes through at the $19.50 price, I would have made around a 150% gain on this over a year. It was a small position (obviously should have been larger, but the liquidity was awful and there was other stuff on my radar at the time), but just like most good trades, you always wish you took more of it.

I’ll be voting against the deal if I still have my shares. The price of $19.29 presently is a 21 cent merger arbitrage on an October closing and at 6.5% annualized, I’ll hold and hope that there is a minor increase in the takeover price. Other than the Chairman, the greater than 5% owners holding this, at least according to TIKR, are Invesco Canada (7.3%), Burgundy Asset Management (7.2%), Fidelity (6.6%) and Van Berkom (5.8%). They will have to get together to extract another few dollars out of this thing before it delists.

Unlike Atlantic Power and its convoluted capital structure, I have no fears that this deal won’t be closing. At worst, it’ll be cashed out at $19.50/share in October and the capital will go to another happy home.

I’m voting against the deal. This is a take-under.

Me too!

Thanks Sacha for the post!

Hi Sacha, are you planning to post any predictions on federal election?

“If all of the necessary conditions to the Transaction under the Arrangement Agreement are satisfied or waived in a timely manner, Cervus expects that the Transaction will become effective in mid-to-late October 2021.”

Merger arbitrage is about 13 cents on $19.37, for a 1.5 month holding, which gives a 5.4% rate of return… sigh.