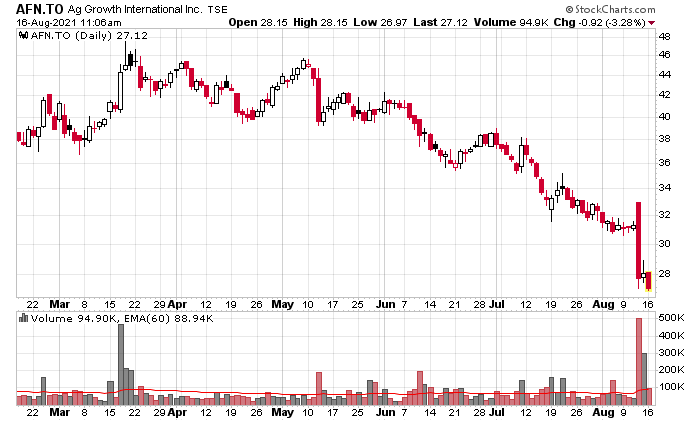

Ag Growth (TSX: AFN) used to be my largest portfolio component, but by virtue of depreciation and something else in the top 5 that has appreciated, is no longer. The company’s stock has taken a beating over the past 3 months:

The market was spooked by their Q1 (May 2021) announcement on their conference call regarding the pricing of steel (indeed, when looking at Stelco (TSX: STLC) you can see what they mean) – companies quote projects and their quotations typically remain open for 30 days, but this is like giving your customers a free one month call option on steel pricing, so they had to tighten this up. They said the high-cost backlog would cost them some margin in Q2 and Q3 but it would normalize in Q4 onwards.

In Q2, there was some margin degradation, and besides this, the quarter was reasonably decent. Sales up, gross profits up, margins slightly lower but this was to be expected. However, the killer payload was this line:

In 2021, two legal claims related to the bin collapse were initiated against the Company for a cumulative amount in excess of $190 million, one of which was received subsequent to the quarter ended June 30, 2021. The investigation into the cause of and responsibility for the collapse remains ongoing. The Company is in the process of assessing these claims and has a number of legal and contractual defenses to each claim. No further provisions have been recorded for these claims. The Company will fully and vigorously defend itself. In addition, the Company continues to believe that any financial impact will be partially offset by insurance coverage. AGI is working with insurance providers and external advisors to determine the extent of this cost offset. Insurance recoveries, if any, will be recorded when received.

I had a massive due diligence failure, especially considering one of these two events was within a car ride of where I am. Fibreco sued Ag Growth International and also the professional engineer that signed off on it, in BC Supreme Court on June 4, 2021. There was also a news article on the matter which I totally missed.

This is probably the biggest contributor to the stock getting tanked over the past quarter. $190 million is close to $10/share, but the larger impact is the balance sheet threat.

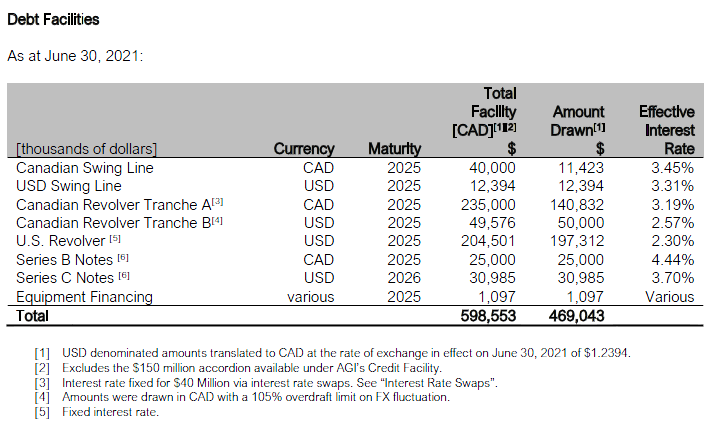

Ag Growth relies a lot on low cost debt capital to fund its operations. Given the nature of its business, their cash flows are relatively predictable and there is a seasonality with cash collections that require the usage of credit. Their debt structure is funded by unsecured debentures (AFN.DB.D, E, F, G and H) each of which is around $86 million in quantity. The unsecured debt is termed out, with D and E maturing in June and December 2022, while the rest of them are out in 2024 and 2026. They also have some tranches of first-in-line bank debt as follows:

Note that they all term out in 2025 and there is about $95 million of availability on the Canadian revolver and $29 million on the CDN swing line.

However, all-in-all, given there is a total of $900 million of debt between these two series ($430 million of unsecured, and $470 million of secured, roughly at an average weighted cost of around 3.9%), the company’s leverage position is quite extended. Tacking on another $190 million on top of that is a tall order. An increase in the cost of capital, needless to say, will be adverse for the equity holders (a 1% increase in capital cost is about 50 cents per share, pre-tax).

The risk has definitely increased due to the number of unanswered questions.

1. How much will insurance actually cover, especially in the event that AFN is found to be at-fault? What is the maximum coverage? (God forbid if the majority of it was self-insured).

2. When will these proceedings resolve themselves (typically it will be by settlement, but a trial would take a couple years to clear out undoubtedly)

3. (by far, the biggest factor of these three, in my opinion) Because AFN screwed up (whether it is their fault or not, doesn’t really matter at this point) building two grain towers, are there any other towers of like composition that are waiting to crumble down?

4. Will re-financing risk be a factor (specifically with AFN.DB.D, and E)?

Question number 3 could literally be a case of waiting for another time bomb to go off, in the form of another grain silo collapse. Another such event would tank the equity by 20% in a day. This is a sort of unknown-frequency, high severity event that elevates risk.

On the flip side, we have the following:

1. The market for AFN’s unsecured debt is still strong (trading just slightly above par at the moment across the entire term) although the whole point of doing this market analysis is to determine when the market is wrong! That said, if there is some debt distress, it isn’t being reflected in these prices;

2. The company, at least on a basis when grain towers aren’t imploding, should be able to generate around $45 million in cash this calendar year, and in a more normalized year, should be able to generate north of $100 million and de-leverage. This is…

3. … fueled by the fact that agricultural products have had their supply chains really disrupted and the demand for product should create demand for capital spending on agricultural equipment.

4. Lawsuits, especially in Canada, very frequently settle for below the “face value” on the claim.

My last comment is that there was some premium valuation in AFN on the basis of “Ag Tech”, but it appears that this bubble has popped with Farmer’s Edge (TSX: FDGE) cratering (it’s down 75% since its IPO and indeed closer to where it should be trading!). This part is healthy.

The current dividend, at 60 cents per share, or $11 million a year, is not particularly onerous to maintain, especially in the case of ‘normal’ business performance, which should be a lot higher than what they have been doing in the past.

If the overhang on the stock is purely on the basis of this lawsuit, the stock is at a price level where it is attractive. If there are more structural issues with the industry that AFN is in, then my original investment thesis was flawed. I do not believe this to be the case, but definitely the elevation of risk is reflected in the stock price. I’m not happy with this situation, nor am I happy about how it was presented in the past few quarters.

are there any other towers of like composition that are waiting to crumble down?

This is indeed the big one! Further, since they won’t want to comment on the cause of the collapse during the law suit, it will difficult to assuage investors concerns here. Time without further problems will help and the share price should begin to reflect less concern as the market absorbs the potential balance sheet impacts.

Great post Sacha.

thanks Sacha – after reading sold my 2024 debenture for a slight capital gain. Too many questions and other possible other worms in the woodwork.

Thanks for that Sacha…my avg cost is just under 32, and I’m confident enough to have more bids in at 26.75. I’ll also hold on to my debentures with an avg cost just below 79.