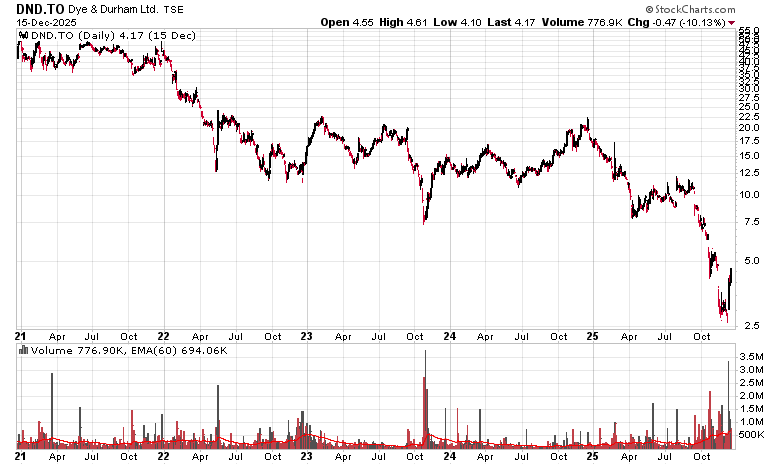

Dye and Durham (TSX: DND) has an interesting story but sadly it may be coming to a close simply because they couldn’t produce financial statements and creditors tend to not like it when the entities they lend money to aren’t in any position to pay back, let alone knowing how much money they are making! As there is a possibility it may be delisted in the near future, I will post its 5-year chart:

During the Covid era the company made many software acquisitions and paid for it with debt financing – amassing about $1.6 billion net from their last reported date, albeit generating $150 million in free cash flow in the past 12 months they have reported. Other than the software they have acquired (amounting to $1.8 billion in goodwill and intangibles) and the material amount of debt, there is nothing else of note on the balance sheet – tangible book value is about negative $1.5 billion.

However, reporting is one of the issues going on – their last financial statement available is from March 31, 2025 (their Q3-2025 as they have a June 30 fiscal year end!).

After they produce the audited financial statements (if they do!), it would not surprise me if there was a massive writedown in the goodwill.

The other issue is that they have been perpetually at war with their shareholders. The drama is simply too much to repeat here, but just giving a scan of the press releases over the past couple years should give a good indication of what is going on.

Notably, despite any lack of financial reporting, one significant shareholder (Plantro) reportedly was going to offer CAD$5.72/share for the entity.

However, just yesterday the TSX finally halted trading on the stock for prolonged non-reporting. Pretty much whichever shareholders are in the stock are locked in until the company either produces audited financial results, or their creditors lower the boom on them.

One interesting data point is that despite the stock not being tradable, their corporate debt is – their 8.625% issue maturing April 2029 (senior secured!) is currently trading at a yield to maturity of just over 12%, about 90.5 cents on the dollar. Given the seniority status of the debt, if DND does go into CCAA, there will likely be some form of recovery by the debtholders (they share the status with the bank creditors, for a total of about USD$905 million plus whatever is on the revolving loan facility).

There is no point for a small fish like myself to get involved with this, but it is interesting to watch. It is also a cautionary tale of companies that expand themselves with debt financing too rapidly.

Thankfully, no positions.

Investing rule #0 – never invest in companies that are declaring death by selecting / keeping an absolutely dumb name

DND opened for trading once again today. They have a crapload of debt. I’m not sure how they can make it without languishing in interest expense hell for a long, long time…

Noteholders 99% tendered their bonds at par for a mandatory offering. Talking about crowding at the fire exit!

DND’s CEO suddenly resigns and steps down from the board (sounds like he was fired).

Right now the senior secured debt (April 2029 maturity, 8.625% coupon) is trading at a 21% yield to maturity. Any excess proceeds of asset dispositions trigger a mandatory offer at par for this debt. There’s no real good way for retail to play this but it should be a sign of the embedded risk in the whole company at this point.

Don’t you think it’s likely they sell CFS during this ongoing strategic review? They already fielded bids for the division and this would cause a massive re-rate in equity value.

Seems somewhat insane for the Prouds to muscle their way back in to then lose all their money in a bankruptcy.

How much leverage do you think DND has in these negotiations?

A lot more than people think. On the surface, it doesn’t look good, but that’s somewhat deceiving. One, you have to reconcile the recent Credas sale with this statement, as the company’s trajectory was foreseeable when it sold Credas. Moreover, the bid history of Matt Proud, especially his November bid (3.5x current equity price) shows that he saw a viable path forward by selling the CFS division (even after expressing concern about the debt). This path has been partially validated by the company’s ability to meet its covenant requirements as of June 30, showing that some of the stabilizing steps it’s taking are working. Moreover, the Prouds, now working together, can bridge loan this for quite a while, especially if the ship is stabilizing. Even a $500M CFS sale would re-rate the equity drastically from its depressed evaluation, and this is below the first round bid range. If DND had no leverage, why would any buyer waste their time and money submitting a bid and syndicating loans that will need to be renewed as negotiations go on. Additionally, a bankruptcy would attract new entrants, not even necessarily securing for the buyers a better deal given how attractive some of the assets are when unencumbered by debt.