Bitcoins are once again making headlines, for exceeding US$1,000 per Bitcoin on various exchanges.

I wrote about them back in 2011 when they were trading at around US$20 a piece. The analysis is really still the same.

The debate here should not be whether Bitcoins are useful as a currency or not, but the lesson here is strictly one in economics – people see value in very strange things, and when people do see value, there will be markets created. In this case, the product is a currency that is only valuable because of its rarity and difficulty of generation, and is not too different than trading artwork or collectibles which have similar appeal.

More people are seeing something valuable in something very odd and this is apparently spreading world-wide to anybody with a computer.

As for answering the question as to what Bitcoin’s peak is, I do not know for sure. This reminds me of when I asked myself when the dot-com bubble is going to burst, or how far the US stock market was going to plunge in late 2008/early 2009.

There are a few headwinds I see for Bitcoin, and they generally deal with hitting the law of large numbers.

The first deals with liquidity.

There are 12 million Bitcoins outstanding, but the reported liquidity is quite thin. Right now if you wanted to liquidate 5,000 Bitcoins and raise a cool $5 million, according to the liquidity chart you would move things about 13% if you wanted to hit the bid with everything you have. Obviously you would want to fragment the order and leak it out over a period of time over multiple exchanges, but I would suspect that there are some component of technical traders that are simply out there to scalp dollars and not actually give a hoot about the currency.

The reported market cap of Bitcoin is about $11 to 12 billion and when looking at a typical equity trading with the equivalent capitalization, Bitcoin’s liquidity is nowhere close. How many dollars can you actually extract out of the market if you had 100,000 Bitcoins and wanted to liquidate in a timely manner?

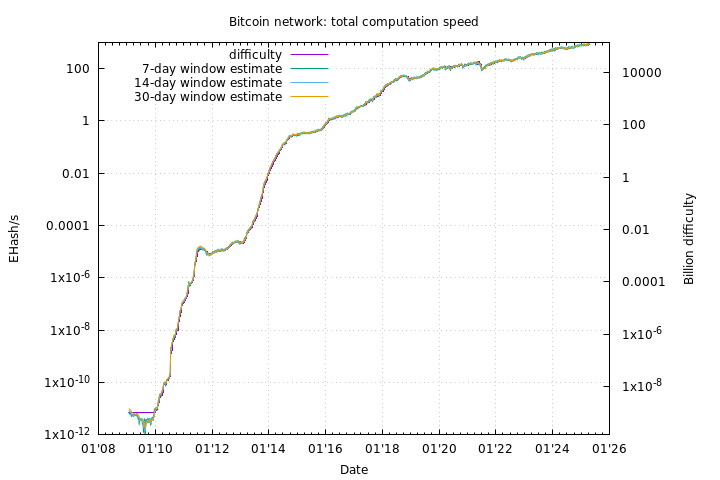

Another issue deals with the ability to control the blockchain (the accounting equivalent of the general ledger, with the notable exception that the blockchain contains ALL information of transactions since the history of Bitcoin). Without getting into a lot of technical details, there are collusion opportunities to corrupt the blockchain if you control a majority of Bitcoin miners. Bitcoin mining has become a very specialized art and to effectively compete in mining, you need to own arrays of specialized devices for the purposes of mining Bitcoins. Since the difficulty of Bitcoin mining increases as a function of both time and the amount of computational power on the Bitcoin network, there has been a technological arms race, with the following result:

Please observe the y-axis is logarithmic – mining Bitcoins has been over a hundred times more difficult than it was at the start of the year. This is like your typical 10MBps residential high-speed internet connection scaling down to twice the speed of a dial-up modem.

The technology to do the proper calculations are application-specific integrated circuits (ASICs) that have their sole purpose in life to mine Bitcoins, but as these are permeating the Bitcoin marketplace, there are limited opportunities for exponential improvement to Bitcoin hash rates through technological innovation – most performance improvement from this point is going to be linear as more machines get added to the cluster networks that are solely dedicated to Bitcoin mining.

I note with amusement the announcement that somebody is producing a 20nm process ASIC rig that can do some insanely high hash rate, but this will be the end of the line: 20nm semiconductor processing is the peak of the current technology limit – even Intel is still working on perfecting the 14nm process. Even then, the company has already announced the product (which apparently will be shipped in Q2-2014) will be at the threshold of the limits that a typical household power supply can handle.

So when you get into industrial-level operations to run arrays of computer hardware solely for the purpose of mining Bitcoins, some group is going to consolidate a majority of miners and be able to corrupt the network. With billions of dollars of market capitalization, it is getting to the point where that group is probably thinking about implementing some scheme to control the blockchain.

The blockchain concept also creates a scaling issue as eventually it becomes impractical for it to be maintained by distributed “retail” computers – “institutional” resources are increasingly employed to maintain the blockchain as they will be the only ones to have sufficient computational muscle to be relevant.

When will this blow up? I’m not sure, but I’m reasonably sure we’re within an order of magnitude (i.e. not higher than US$10,000/Bitcoin) just because of the law of large numbers – liquidity (the quantity of dollars Bitcoin is able to extract from others) and blockchain dynamics.

The current phase in Bitcoin is still adding people with money into the system, which is required for the scheme to continue, but those that have caught onto the scheme earlier will presumably be continuing to diversify their Bitcoin holdings into harder currency.

When reading Reddit’s Bitcoin chatter, I see a lot of financial illiteracy out there, which doesn’t bode well for those that have high hopes for Bitcoin.

I do not own any Bitcoins, nor will I, but I am watching this with curiosity. It is indeed is fascinating to watch non-financial people get involved in what is inherently a financial specialty product with a touch of well-designed technology sprinkled in. Whoever conceived of this did their homework and never would have guessed the technology arms race that has developed as a result.