First of all, Merry Christmas to my readers. Even if your financial health is suffering due to this very exciting quarter, be thankful if your physical health is in good stead. I won’t blame you if your mental health is somewhat suffering simply due to all of this calamity going on.

My “stock radar” is coming up with so much material to look at right now that, coupled with the other usual obligations that go along with the Christmas season, I am running out of time to properly look at everything.

I’m going to summarize a lot of information in this post and it will be in no particular order.

S&P Volatility

Volatility is anti-correlated to the price index and past history would suggest that if this index reaches to around 50-60 it would probably be a good time to deploy capital. This happened last in early February, but going back in time, the previous opportunity was the Euro-crisis in the Summer of 2015.

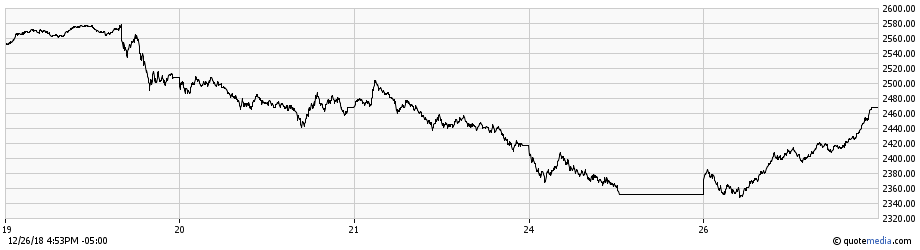

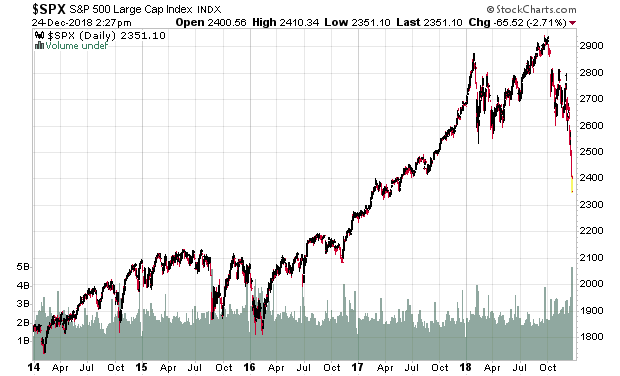

S&P 500 itself

Technical analysts will point to a very obvious price target – around 2,100. If this happens, that equates to nearly a 30% plunge in the S&P 500. From a high of 2940.91 (September 21, 2018) to 2351 today, the index has dropped 20%. The big factor is that this has happened in a very short period of time – about 3 months.

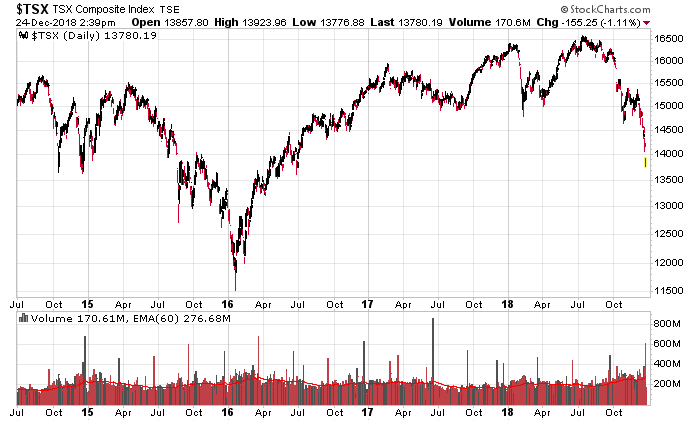

TSX

The longer-term chart for the TSX doesn’t look nearly as bad simply because the commodity-heavy capitalization of the index never took off in the first place. Despite appearances, the high was 16,586.50 on July 13, 2018 and at today’s value of 13,780, that’s a 17% drop, so mirroring pretty much the same that happened to the US major index. There’s still another 15% or so from present prices before getting to the commodity plunge pricing in February 2016.

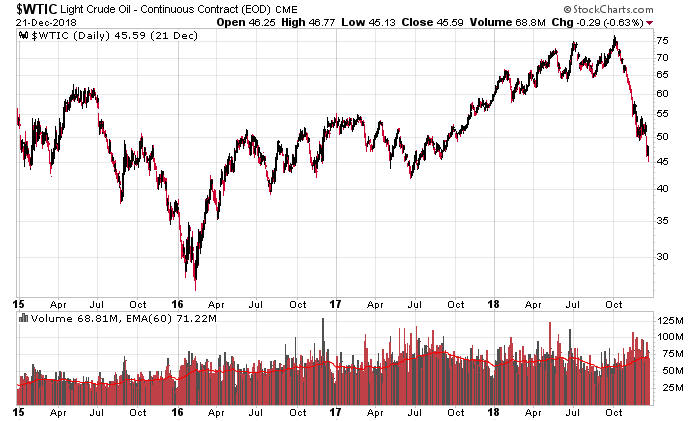

Oil and Production

US producers have crushed everybody else into oblivion. Coupled with an economic slowdown, there is going to be a lot more financial pain in oil markets if pricing does not improve. The commodity price is getting to the point where it is nearing the marginal cost of extraction at the volumes of crude required, but a longer term analysis of commodity trends says that prices can actually go below marginal extraction costs for quite some period of time before normalizing. Just look at the Uranium market as a good example.

Western Canadian select is around US$30, which is a healthy recovery from the dark November days when they traded as low as US$12. The differential has narrowed to US$15/barrel, but this was probably not what they wanted – there isn’t a lot of profitability in Canadian oil at US$30/barrel.

If we are going into a recession and consumption does decline, we are still going to see further pain in oil and gas. That said, a lot of oil and gas stocks, especially Canadian producers, are trading like the businesses are going to go bankrupt. At current prices, some will be, but successful timing of the commodity cycle and maximum pessimism should be rewarded with handsome capital gains. Getting this timing correct is never easy.

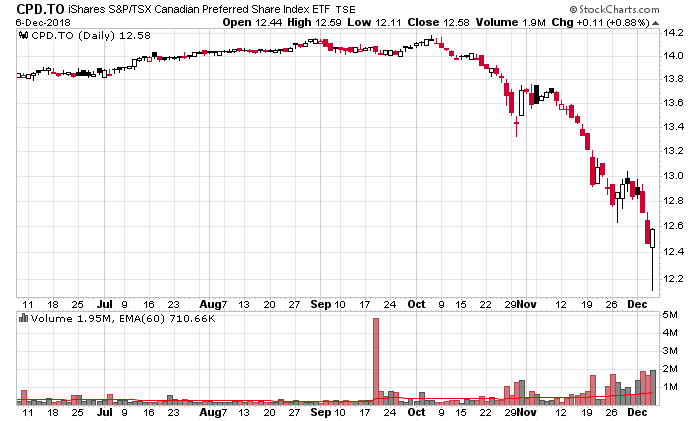

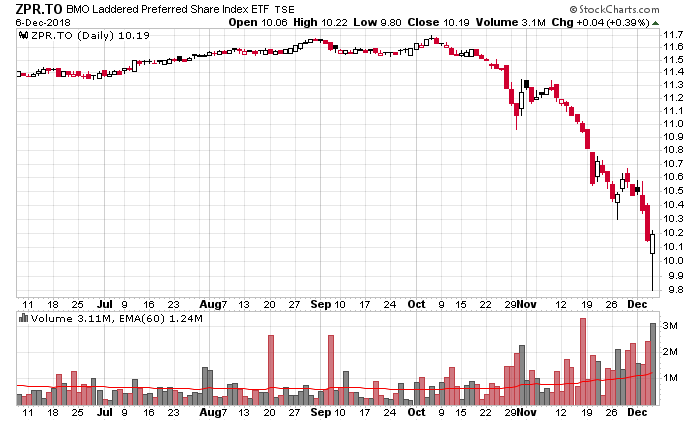

Safety of various well-known issuers

Many people out there, especially on the retail side of things, are looking at major Canadian banks (BNS, BMO, etc.) and high-yielding utilities (e.g. Enbridge) as bargains at present. While they sport high dividend yields, they also sport liquidity risk that I do not believe these investors fully appreciate.

A good metric for how dangerous these companies truly are is represented in the junk bond market (e.g. HYG:US) is a reasonable proxy for the junk bond market.

If BBB credits (and worse) can’t get good debt financing, then most other debt-sensitive sectors are going to face higher refinancing costs. Leveraged entities are going to face earnings reductions.

Canadian Convertible Debenture sweep

I’ve done a sweep of the entire TSX exchange-traded debt market. Only two issuers really caught my attention out of the entire universe that is trading. I’ll be doing some more research on it later.

Some other gems that I will mention in the TSX exchange-traded debt space: the fiasco at Zargon, and you can always pick up some debentures of Lanesborough (TSX: LRT.DB.G) for less than a penny on the dollar if you believe Fort McMurray real estate is going to make a swift comeback from the dead. This REIT is so deep into the hole, the only question is how the present controlling management will be able to siphon any value out of it before they pull the CCAA pin and euthanize the publicly trading entity.

In general, I’m surprised how little value there is in this space given the calamity going on in the equity side.

Short-term cash management

US Dollar:

Little duration risk –

BSCJ earning 3.18% (minus MER 10bps), 0.5 year duration

IBDK earning 3.16% (minus MER 10bps), 0.46 year duration

Both these ETFs terminate at the end of 2019 and contain mostly Baa-A corporate debt scheduled to mature in 2019. Duration risk will drop as their bond portfolios mature (good for a rising rate environment, although one suspects it won’t be rising for too much longer!).

Some more duration risk can be had with SHY, 1.88 years, with a 2.65% YTM, and 15bps MER.

Interactive Brokers gives 1.9% on USD, so one takes about a 1.2% pre-tax sacrifice for holding it vs. a near brain-dead bond fund.

Canadian Dollar:

RQG earning 2.54% (minus MER 28bps), 0.65 year duration

XSB earns 2.45% (minus MER 17bps), 2.75 year duration, slightly safer bond selection than RQG.

Interactive Brokers gives 0.71% on CAD, so the spread is about 1.5-1.6% pre-tax.

Home Capital Group and Equitable Bank’s short-term savings accounts give a 230bps yield for on-demand money, so if one is willing to do the paperwork hassle and is willing to take some deposit risk (remember the imminent solvency worries about Home Capital Group earlier this year?), this is not a bad place to park capital in relation to having to suffer through the hassles of trading the above. Indeed, if you feel brave and want to lock in for a year, they will offer 310bps.

Considering the Government of Canada 3-month rate is 1.67% and 5-year rate is 1.92%, this is telling. The competition for deposits is likely to increase and this would explain why banks are not going to do so well in the future.

Canadian / US interest rate environment

BAX quotations have flat-lined. The current 3-month Bankers’ Acceptance rates are 2.23%, and with the March 2019 BAX futures trading at 2.26%, the market is now projecting that Poloz will hold steady on his January 9, 2019 rate announcement. I’m somewhat thinking that the demise of at least one future rate increase is mis-guided, but we will see.

The US interest rate environment has changed dramatically over the past couple weeks. Now the Federal Funds rates are locked at 97.60 (2.4%) through December 2019, plus or minus a very minor chance of one rate increase. The two-year treasury bill yield is down to 2.63%, and the 10-year is at 2.75% – very slim differential.

Future market projections and where to make outsized returns in the future

Am I going to give away all my financial secrets for free? Sorry!

But needless to say, I think there are a few areas with very low-lying fruit that is getting sold off in forced-liquidation type trading. Figuring out when there will be a bounce-back will be difficult. This isn’t a 2016-type environment where you have the federal reserve willing to throw hundreds of billions of dollars into the market – we are facing the opposite environment and thus must act accordingly.

I’ll have my year-end update posted sometime near the new year. Barring a significant market event, Q4-2018 will be my first quarterly loss since September 2015!