Per the December 14, 2021 reinvestment policy, the Divestor Canadian Oil and Gas Index (DCOGI) has the following reinvestment of cash proceeds as received from dividends, as based on the opening prices of the first trading day of 2022:

Divestor Canadian Oil and Gas Index - January 4, 2022 Re-Balancing

| Ticker | Fraction | Reinvest$ | Price | Shares | Residual$ |

|---|---|---|---|---|---|

| ARX | 5% | 1,908.34 | 11.75 | 162 | $4.84 |

| BIR | 5% | 1,908.34 | 6.51 | 293 | $0.91 |

| CNQ | 20% | 7,633.38 | 54.2 | 140 | $45.38 |

| CVE | 20% | 7,633.38 | 16.01 | 476 | $12.62 |

| MEG | 5% | 1,908.34 | 12 | 159 | $0.34 |

| PEY | 5% | 1,908.34 | 9.6898 | 196 | $9.14 |

| SU | 20% | 7,633.38 | 32.5 | 234 | $28.38 |

| TOU | 10% | 3816.69 | 41.25 | 92 | $21.69 |

| WCP | 10% | 3816.69 | 7.6014 | 501 | $3.88 |

| XEG | 27,147.19 | 10.83 | 2,506 | $7.21 | |

| ZEO | 47,693.04 | 47.35 | 1,007 | $11.59 | |

| VCN | 29,228.59 | 43.25 | 675 | $34.84 |

(Updated February 5, 2022: Please note that I forgot to incorporate the Tourlamine special dividend of $0.75 in the 2021 results. This has been incorporated into the table and values edited accordingly.)

The total sum available for re-investment was $38,166.89.

The share counts have been revised on the index accordingly.

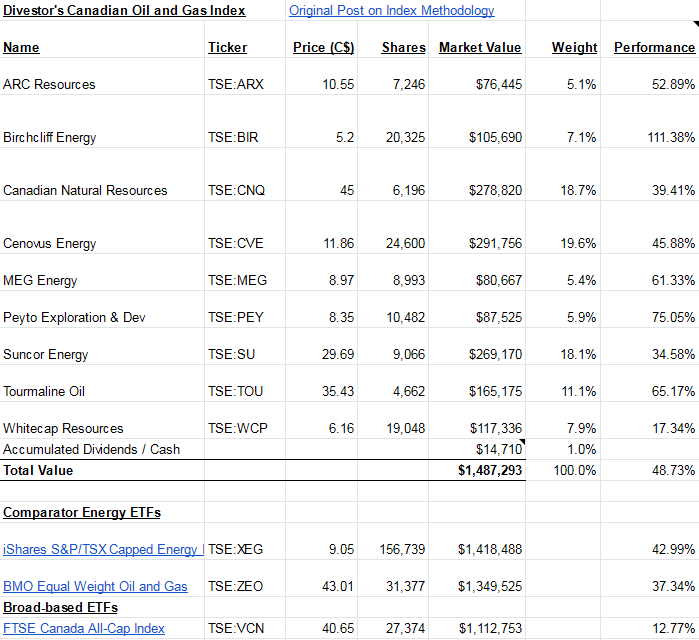

From February 5, 2021 to December 31, 2021, the DCOGI earned 78.8%, while the nearest comparator, the XEG.TO ETF, earned 68.5%.

While the DCOGI is not mirrored by real money, given the liquidity of all of its components, it is fairly easy to “replicate at home” if you wish.