Major holders of institutional money are likely on “autopilot” for Christmas so it is likely no major changes in investment policy decisions will be made until the new year, short of some geopolitical calamity.

Canadians have until December 29 to sell securities that are sitting in a loss position to claim a capital loss. Americans have until December 31st.

The real question I’m grappling with is how much more can monetary and fiscal policy continue to drag the powder keg up the hill before something breaks and it all comes tumbling down. Japan has shown the western world the way how you can run massive deficits for a very long period of time without catastrophic consequences. It might go on longer than most people think.

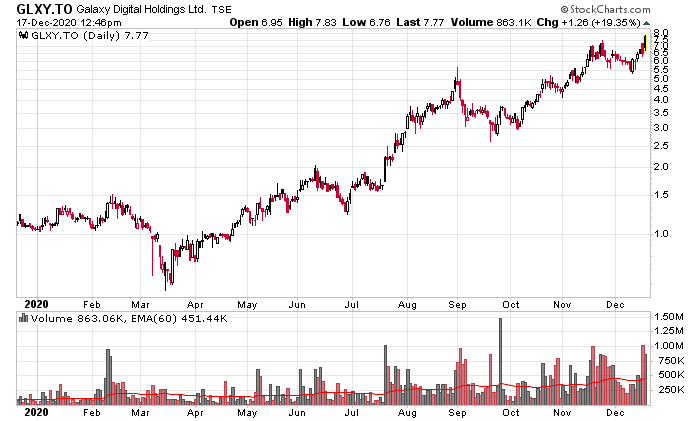

With the rampant speculatory valuations seen in many sectors (for two great examples, look at Peloton (PTON) and Chipotle (CMG) – yes, fast food that should be trading at over 100 times normalized earnings), there is quite clearly a degree of misallocation that hasn’t been seen in quite some time. The origins of such speculative fervor can likely in part be attributed to the supply-demand dynamics with passive indexation coupled with momentum – for example, the larger your market cap is, the more you will be included in the respective indicies. This creates price insensitive demand, and this is all too willing to be sucked up by the marketplace.

This could be the stock market equivalent of Chinese condominium towers being built in the middle of nowhere – to be sold as “stores of value” in absence of other opportunities. Maybe if you’re lucky, in a few years you can AirBnB and make a few RMB of income with it.

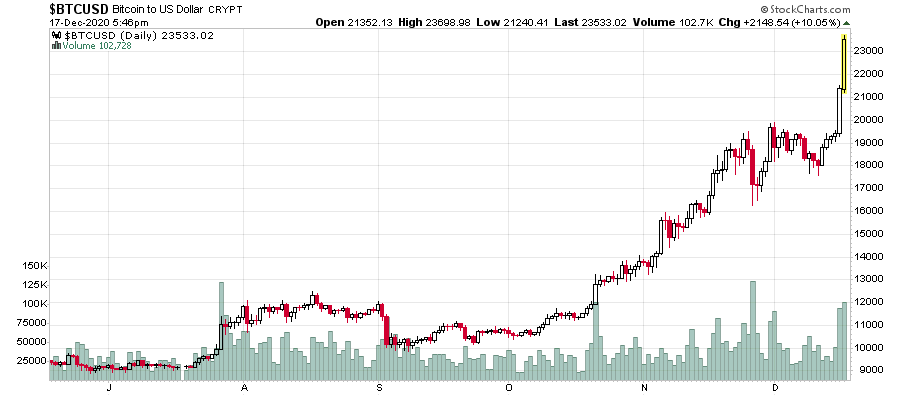

You can’t short them (what’s crazy can get crazier), you can’t long them (don’t know when the music will stop), all you can do is get them out of your mind. The mental return on brain damage is too low, although there is a huge gambling appeal which is witnessed by the whole locked-down millennial world discovering Robinhood and thinking they are stock-picking champions as they swap CERB money with each other, with the market makers skimming pennies a transaction. You don’t have to read me anymore, just pay attention to everything these TikTok millionaires do.

Relative performance managers that are indexed to the S&P 500 will have had to reach a +14% hurdle so far in order to justify their pay. Hypothetically, if they put their entire portfolio in Apple for the year, they’d be sitting on an 80% gain. Considering Apple is about 6% of the index, it makes you think about the other parts of the S&P that must be underperforming Apple. Something makes me think Uncle Warren B. was onto something when he ploughed nearly a hundred billion of his capital into Apple stock – it was his version of going into Bitcoin.

Managers indexed to the TSX will have seen a +3% gain this year. Your ticket to glory was Shopify, which did reasonably well during the COVID crisis, but had you held on from the beginning of the year to present, you would be up triple your original investment. My god, what do I do all this investment research for when these superior returns are just staring you so blatantly in the face?

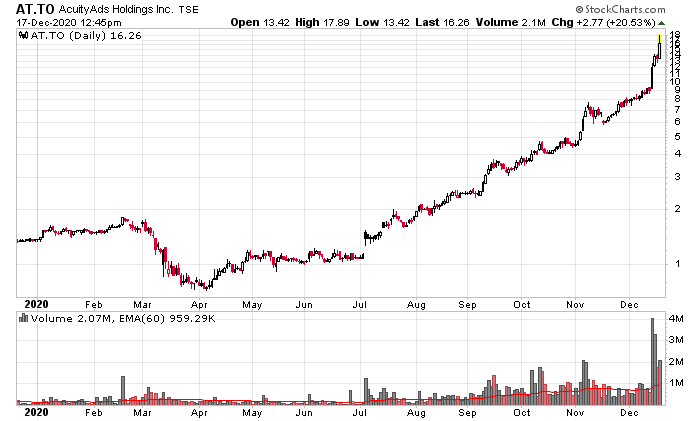

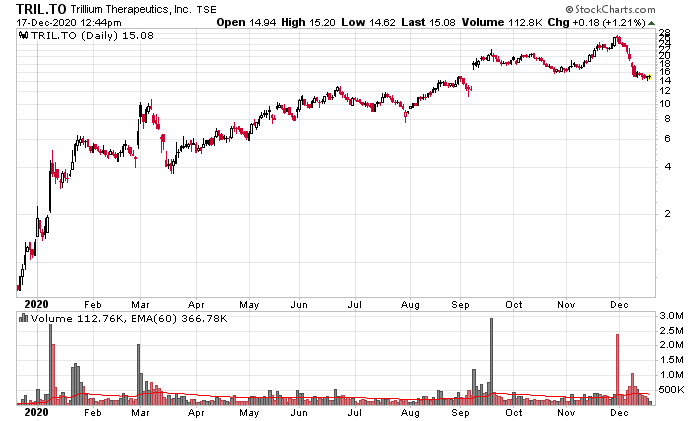

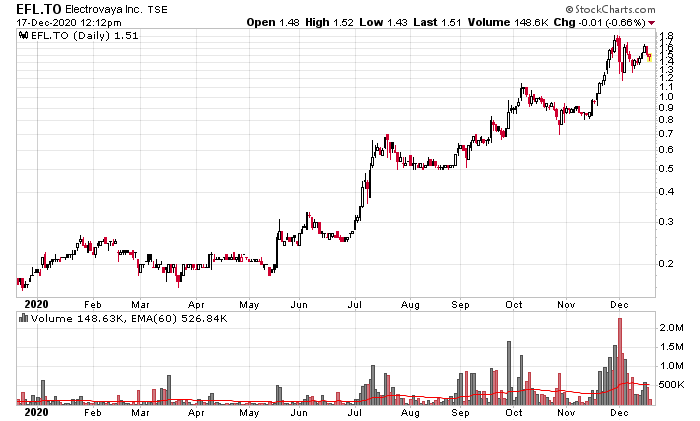

I’ve done a cursory scan of the entire TSX on the loss side and earmarked and looked into a few issues that are of interest, but I’m not at all close to pulling the trigger on any of it.

In fact, when I look at my own portfolio, the most clearest speculative component is the one that is doing the best percentage-wise from cost. The most obviously “value” stock is not doing that well at all (you can probably take a guess which one this is).

For the past couple weeks, I have been trying to visualize how 2021 will emerge.

With infection rates, coupled with vaccinations to bring the SARS-CoV-2 episode to a close in 2021, people are going to have outlets for their money from avenues that were previously inaccessible. Travel, entertainment, socialization, etc., will continue to be demand sinks for consumer capital and this may have impact on the asset side. One big looming question is upon the restoration of the full slate of economic services available, will there be demand, especially after government stimulus programs run out? Or will there be wave, after wave, after wave, as long as central banks functionally pay for it by interest rate suppression? How long can this last?