It might be a sign of the times that over the past half year or so I have been less focused as of late on my investment research looking at individual companies, and more about playing the role of “closet macroeconomist”, hence the focus of my posts being mostly about macroeconomics lately.

I am not intentionally trying to hide secrets (although there are a couple picks here and there in the non-oil and gas space that are still sitting on my research queue after passing my initial smell test) but in an environment where my baseline investment criteria is that it can earn 25% free cash flow to enterprise value, what’s the point in looking for other stocks?

The answer of course is there will be a time that fossil fuels will become politically correct once again (perhaps when all the lights and crypto farms shut off) and one will then have to dip into the watchlist bucket for other suitable investment candidates. That said, fossil fuels are still going very strong and hence why bother when the thesis I wrote back in 2020 (roughly summarized as being long anything ‘real’ and avoiding anything ‘financial’) is still very much intact?

The reason for the macro focus is simply because it is increasingly a dominant variable in today’s investing climate. To give an analogy, let’s say your choice was investing in established large cap gold miner X and gold miner Y. Ultimately you can talk about mine reserves, operating practices, all-in sustainable costs, capital structure, and on and on, but the dominant variable is much more simpler – the price of gold.

Likewise, the macro situation is creating a dominant variable environment where if you cannot get on board with the correct solution, it doesn’t matter what else you invest in – for instance, back in November 2021, it did not matter one bit which portfolio component of ARKK you invested in – you would have lost money no matter what. Perhaps the magnitude of loss would have been different had you chosen wisely, but it would have been a loss nonetheless.

The macro focus that requires meticulous attention is monetary policy and energy economics. Both right now are more dominant than ever as we are experiencing ‘the turn’ that has caught people flat-footed (including Covid, and the sudden realization of geopolitical instability in eastern Europe), coupled with an incredible amount of monetary mismanagement and dismissal of energy physics that has all translated into really terrible policy. Playbooks that worked in the past will not be working in the future.

One of these playbooks is a sacred tenant of portfolio management. It states that a correctly managed portfolio will have an equity and bond split, say 60/40. If you are young and want to take more risk, then 70/30 or even 80/20, but the point is there is some bond component. The notion is that when equities fall, bonds will rise, and if you maintain a consistent percentage, you will be able to rebalance and extract better value in the process.

We insert in the new macroeconomic reality where inflation is running hot and fast, and your bond portfolio is still trading at a negative real yield. This means that the bond component of the portfolio is losing purchasing power for the investor and only depends on other people purchasing bonds to keep its capital value in the event of an equity drawdown.

With the Bank of Canada, US Federal Reserve, and soon the EU engaging in quantitative tightening, coupled with increasing yields (that would also be impacted by QT in addition to inflation), bonds are going to be terrible investments if the next logical conclusion comes. What is this?

Continued monetary debasement. Amazingly despite everything, because the US dollar is the last one standing, it still wins by default. For now.

This brings up a rather interesting quandary for most institutional fund managers. You can’t hold cash (real negative yield, not to mention that you are hired as a portfolio manager to deploy cash and not stuff it in your mattress). You can’t hold bonds (take a look at the idiots that bought Austria’s 100 year bond with a 50bps coupon for twice par!). You can’t hold equities (take a look at the S&P, for example) although this is the least worst of the three options. Don’t even get me started on cryptocurrency as an asset class – although I do see that Luna is CAD$0.000101 a piece, so perhaps you want to buy one of these as an inflation hedge.

There is no escape at an institutional level. One workaround has been to shovel money into private assets and real estate and infrastructure, but these asset classes are very sensitive to rate increases although of course they do not mark them to market until it is too late. Private assets are a brilliant way to defer those losses, however!

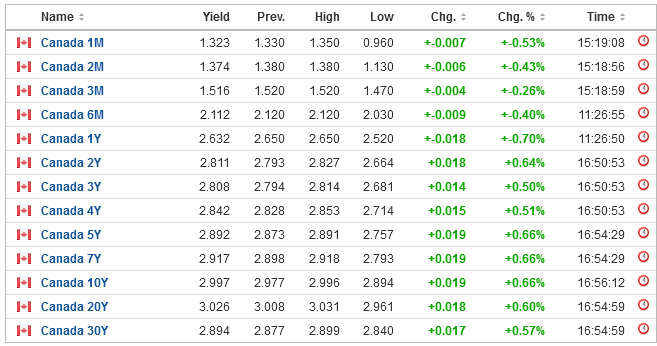

Interest rates themselves are another matter. There has never been a point in history where we have seen such monetary manipulation to the point where real rates of interest have been driven this low without massive reverberations. The “consensus” scenario is that we’ll get a 50bps rate hike in July and then some more minor tightening before things ‘normalize’ and are back to normal.

But consider that your baseline input to the economy (energy) is at sky-high levels with no real material notions that more capacity is being brought online – what if this input to inflation keeps rising further? Everybody cites ‘demand destruction’, and indeed there will be a point where energy inputs will become so expensive that collectively we will be forced to stop using them, but until that point, we will see the trickle-down (or perhaps rain torrent) effect of these costs getting baked into everything we consume.

Likewise, salaries will be escalating, and inflation will start on its trajectory of a self-fulfilling prophecy – labour costs will rise because of inflation, and inflation will drive up the cost of labour supply. Already in British Columbia, we are seeing the seeds of this with the upcoming strike vote by the main BC Government Union – they are apparently miles apart from the government. This is one of many cases that will be resulting in significant wage increases going forward.

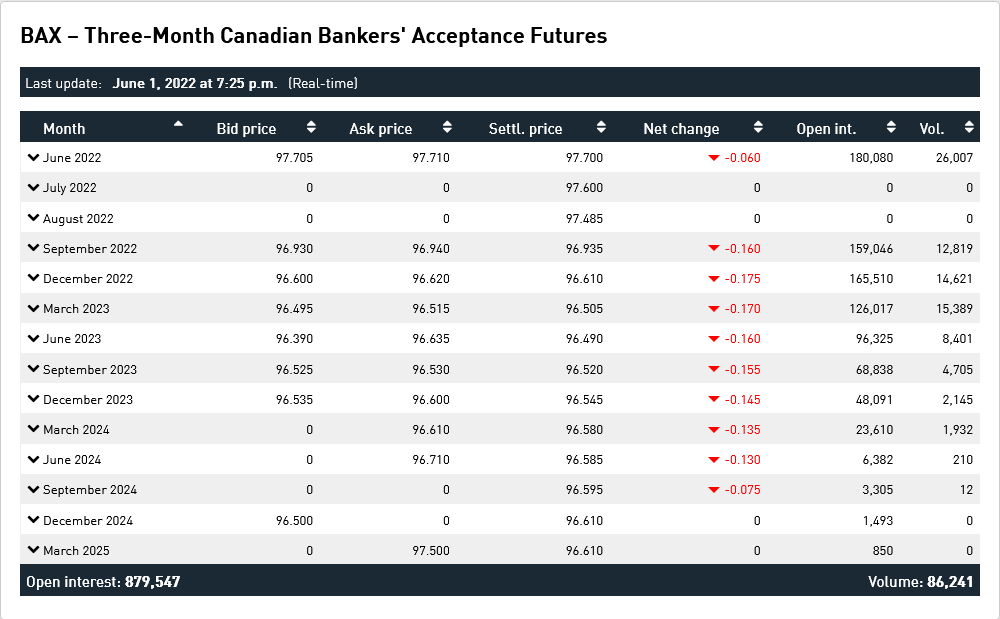

In a recent Bank of Canada speech (one day after the June 1st 50bps rate hike), we had the deputy governor talk about inflation. They’re now now talking about “avoiding entrenchment” of inflation. Note that derivatives of the word “entrench” is like the new “transitory”.

You don’t avoid entrenchment with small steps. You need shock and awe – something that goes beyond letting the market guess whether the next rate increase will be 50bps or 75bps. An example would be having an unplanned rate announcement with a 150bps increase “to get things back to the neutral rate”. The current short-term policy rate of 150bps is still at near-record lows (historically), and still below the ambient level the Bank of Canada had before Covid-19 (which was 175bps). The big mistake that people can make is this natural assumption of the “regression to the mean”, and currently that scenario right now is the bank will raise to 300bps and keep things there.

Consider the scenario where they will need to raise even further, to around 600 to 700bps to achieve the destruction of this “entrenchment”, and figure out the financial consequences. I am not saying this will happen, but it is definitely something that one should keep in their minds going forward – that inflation will be running away, just like how global warming activists claim that an increase in the Earth’s CO2 beyond a threshold point will cause a run-away greenhouse effect. Ask yourself what components of your portfolio get killed in a world where short-term rates are 700bps, we live in an inverted yield curve where the 5-year mortgage rate is 600bps and almost every asset out there is slashed in half. It isn’t pretty – practically everything other than cash loses in such a scenario (yes, including fossil fuels).

I am not entirely sure what is going to happen. Things are incredibly fluid right now, and I continue to remain very cautious. If there is any general prescription I could give to people, it is the following – if you’re leveraged, get at least flat.