The title of this post were the words used in the last sentence of the Bank of Canada’s interest rate announcement.

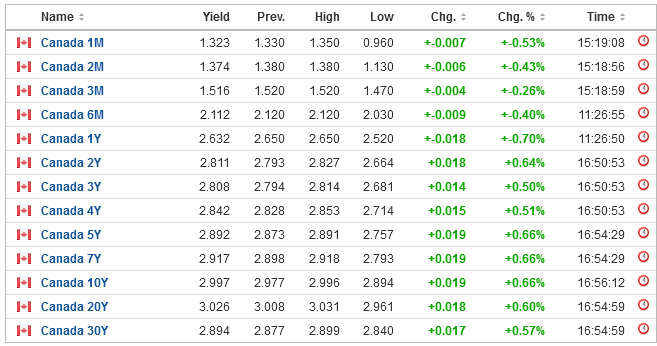

They did not surprise many with a 50bps increase (to a 1.50% target) although the yield curve regardless jumped up a little bit across the entire tenor.

Barring any catastrophic events, it is highly probable that July 13th will feature another 50bps rate increase. The yield curve continues to flatten.

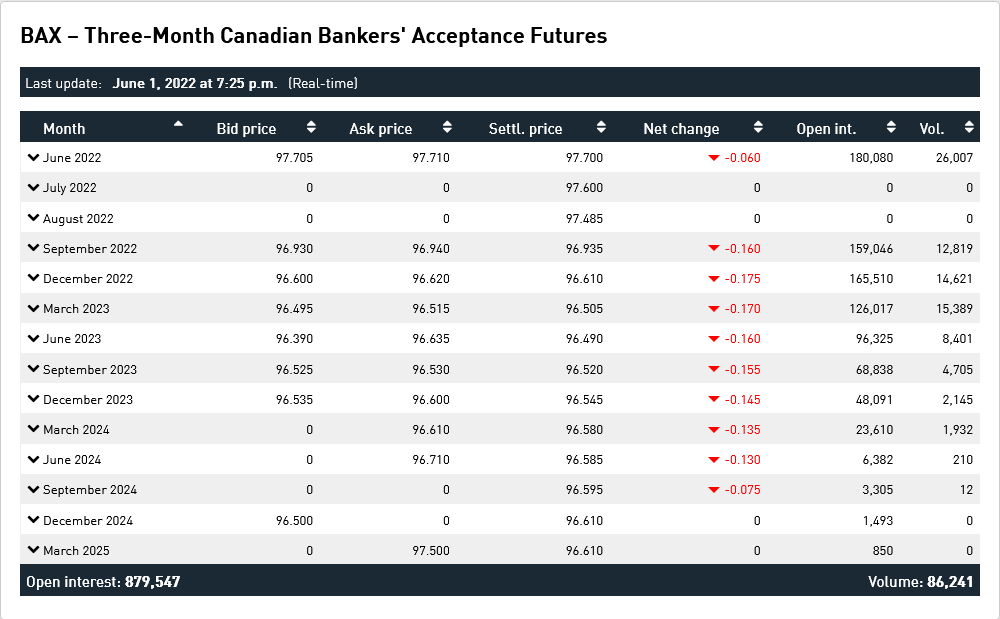

Reading the BAX futures, over the next 12 months we have another anticipated 150bps or so of rate increases – instigated likely by ‘forcefully’. Today the 3-month banker’s acceptance rates is 195bps (98.05) and the December 2022 futures have it at 96.61, a 144bps difference. This very roughly corresponds to 3 50bps rate hikes (July 13, September 7, and October 26) before the Bank of Canada decides enough is enough.

After the July 13th rate hike is where things get interesting. There is this pervasive prediction of an inflationary course of mean reversion, under the theory that the inflation is caused by supply chain disruptions, Russia going to war and the like. Making this assumption can be hazardous to one’s financial health. For instance, if interest rates rise and inflation continues to remain elevated, the central bank will have no recourse other than to continue raising rates further (and possibly at a more rapid pace) to bat down inflation to a 2% target.

The temporal aspect of measuring inflation has an odd effect – for instance, in year 1 if the price of bread is 10 cents, and in year 2 the price is 20 cents, you’ve just experienced a 100% inflation. If the price of bread is 20.4 cents in year 3, you can declare victory as you’ve met your “2% target”, but the damage has already been done – that bread is going nowhere close to 10 cents no matter what your monetary policy is!

I suspect this is what will happen (get used to those high prices remaining… forever!), but there are some economic scenarios where we really start to see some very strange distortions, where despite high rates and monetary policy liquidity withdrawals we still will see rising long term interest rates. Right now the 5 year government bond yield is 289bps, but what if this goes to 400bps, 500bps or even 600bps? The implication of the real estate market seeing a 7% mortgage rate would completely crush the market and negative equity headlines would become rampant in the media. I’m not saying this will happen, but it is in the list of possibilities. After the summer of post-Covid fun is over with, there is going to be a sobering period which will be painful for many, even more so than what we are seeing today.

Be prepared to act more forcefully in the event that the landing is not so soft.

Hilarious that BoC is trying to halt fiscal-generated inflation using purely monetary instruments. Maybe somebody should have listened when approving helicopter money galore…