The Federal Reserve and Bank of Canada’s desired effect right now is to deflate the asset markets, creating a ‘reverse wealth effect’ which will hopefully stamp out some amount of inflation.

We are already seeing this rush for liquidity. It’s been going on for months now, but it’s getting to the threshold where it is actually being noticed by most people as they check their brokerage account balances.

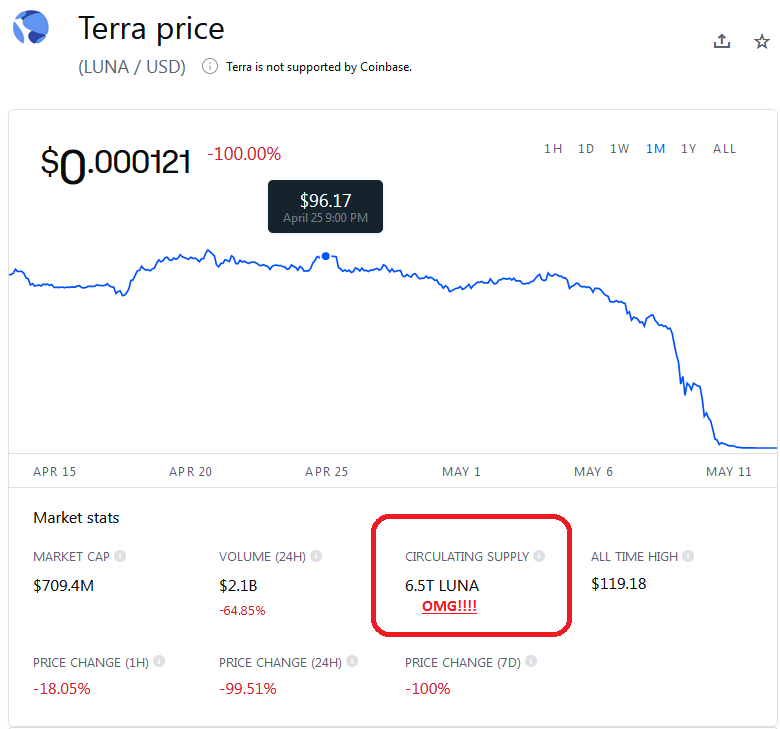

As funds start to face redemption orders as people continue to want liquidity and demand US dollars to pay off their debts, we see asset prices drop as a result, across the spectrum (especially “stablecoin” Luna holders!). Very little gets spared in these market situations.

Companies that have long track records of producing cash are taken from a higher multiple to a lower multiple. A company that was previously trading at a (truly!) stable 15 times earnings will be re-valued at 12 times – that’s a 20% haircut in price. You haven’t lost value in the company – it will still continue earning the amount of cash it has been earning, but instead your capitalized value of it has been re-rated so if you want the entire sum of those cash flows today you will be receiving less money.

Lower prices bring higher returns for reinvestment. That company previously trading at 15 times would give you a 6.67% return – today those same dollars would give you 8.33%. The company can then look at its ledger for reinvestment opportunities. In a perfect world, it will invest capital externally in those projects that can earn better than 8.33%, and if it can’t, it will buy back shares (or give it to shareholders as a dividend). Real world conditions are never as black and white or clean, and hence a market exists.

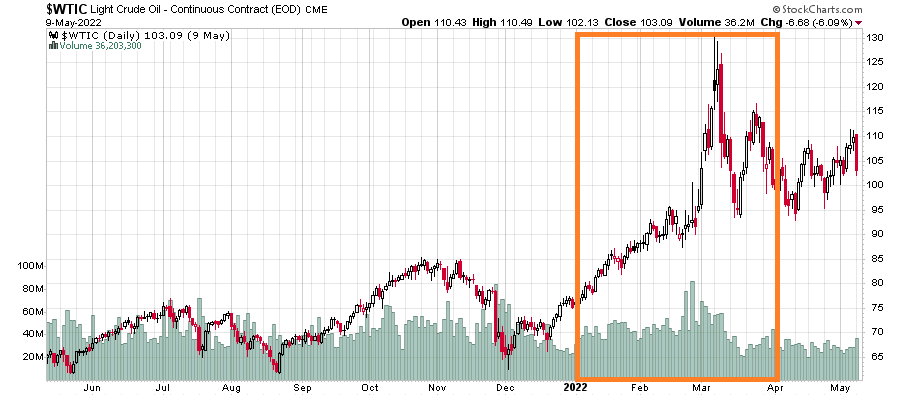

We look at another real-world situation where a company like (TSX: CNQ), at US$107/barrel oil, trades at 4.7 times free cash flow (21%). The opportunity for them is obvious – buy back their own shares – and in a day like today, they will easily be able to post a bunch of bids and get hit as their stock is down 3%. Will the market take them down 20% to 3.8x (27%)? If so, it will make their buyback program that much more accretive – if you take the assumption that this commodity price environment will continue.

This price environment cannot be and is not assumed to last by many, hence the very low price to cash flow multiple given to these companies. Indeed, a big destruction of demand would cause commodity prices to tumble and will correspondingly take down equities with it.

There is also a propensity by many to take gains on stocks trading at 52-week highs – either to cut down your percentage allocation (anybody with fossil fuels in their portfolio have most certainly seen them bloat to high percentages) or as a manner to ‘take chips off the table’, perhaps to invest in beaten-down technology companies.

These are financial considerations. You can make these transactions by clicking buttons in front of a computer. The real-world physical market is a different story.

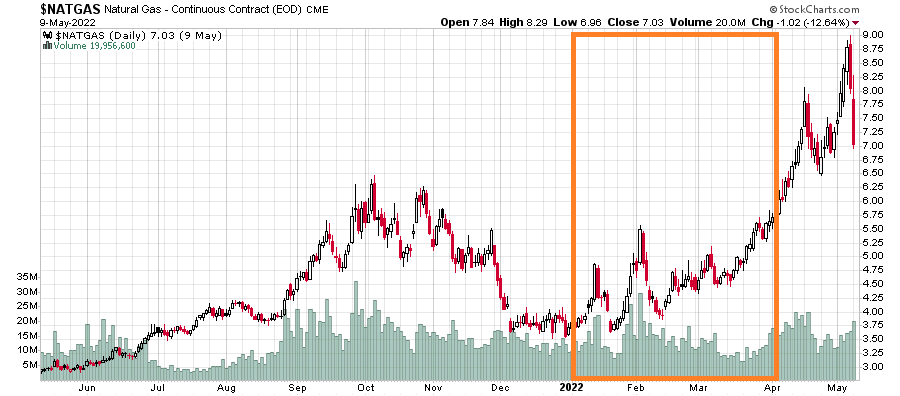

With the physical commodity environment showing few signs of retreat (Russia’s oil and gas exports will surely drop in the upcoming months, and US strategic petroleum reserve releases do not appear to be making any dents on US crude inventory levels), for now, it appears that the physical environment is favourable for continued high prices. Coupled with massive amounts of cash flows being poured into share buybacks, should put a limit to the downside of the fossil fuel complex. Indeed, investors should be cheering on price drops as moments where more shares can be taken off the open market when the physical market is still showing great demand in relation to supply.

The physical environment of a relatively inelastic commodity is very telling. It is best illustrated with an analogy.

Let’s pretend that we have an island of 100 people, a food factory, and cash. Initially this island produces 110 meals per day of food, and this food is of the non-perishable variety, so you can store it somewhere for rainy days. Everybody is happy, the price of food is low, and everybody can go and watch Netflix since there is nothing else to spend your capital on in the island other than buying food and maintaining the food factory. Netflix makes a fortune since they can raise their prices continually, although there is a fraction of people that prefer to just watch the waves crash against the beach. However, over time, there is a belief out there that the food factory causes a slowdown of video streaming resolution, so many of the island residents manage to pass a policy framework that chokes maintenance investment in the food factory. Initially this doesn’t have much of an impact as food production went to 105 meals a day, but over the past few years, it has slipped below 90 meals, but there was a sufficient surplus to keep people fed.

Indeed, there was a disease that struck the island that caused residents to eat half as much as normal for many months, but they slowly managed to recover from this disease, and now are back to normal eating levels. The surplus of meals that was built up by the food factory that is now producing 80 meals a day was immense, but that surplus is now running low, and residents are starting to get fearful that they will not be able to purchase food much longer. The price of the meals slowly starts to climb as this awareness creeps in, and now that this surplus is approaching critical levels, prices on this inelastic good is very, very high and everybody on the island is now noticing the price of food, and talking about how we need to subsidize people to purchase food. There are also talks about how the food factory is unfairly engaging in price gouging, and how the factory should be “islandized” to ensure a fairer equitable distribution of food. Nowhere is it mentioned that capital should be invested into the food factory to increase its output – as this would slow down people’s video streaming resolution (no way you can watch those videos at 1080p when you’ve been watching it at 4K all your life!).

Hence the situation we are in today. It doesn’t end very well.