NYSE Data has margin borrowing at $401 billion, which is an all-time high.

The record level before this was back in July 2007, about 9 months before Bear Stearns went belly-up. The amount of margin debt then was $381 billion.

Canadian Finance and Economics

NYSE Data has margin borrowing at $401 billion, which is an all-time high.

The record level before this was back in July 2007, about 9 months before Bear Stearns went belly-up. The amount of margin debt then was $381 billion.

Does it feel like 1999 to anybody out there? Basically if you invested in high beta, momentum type stocks (especially those .com companies with as little revenues and high negative incomes) you would have made like gangbusters. If you actually invested in anything that made financial sense, you would have seriously underperformed, if not seen depreciation in your asset values.

People investing in Apple currently must feel like that. There is a lot of stuff out there that has seen substantial price appreciation and very little change in the fundamental thesis in the first place – e.g. has the story with Netflix (a triple since the beginning of the year) changed any over the past 10 months? Priceline (nearly doubled)? Even old technology, like Hewlett Packard, has seen appreciation that doesn’t seem to correspond with any real change in their underlying structure.

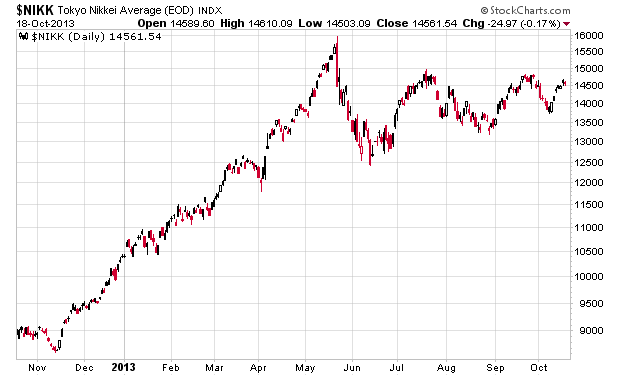

Just because markets are trading wildly higher doesn’t mean that they won’t stop doing so – momentum in the marketplace has amazing power that will confound even the most seasoned of investors. Its already happened elsewhere, such as the Nikkei 225:

Investors in the month of May saw appreciation and depreciation of nearly 20%.

We are in strange, strange times. The trick is to not lose money on the way down.

Genworth MI (TSX: MIC) will be reporting earnings at the end of the month. They are likely to continue seeing historically high rates of mortgage conformance and as a result, they should be reporting a decent quarter as they continue to book earned premiums. Canadian unemployment continues to be steady (if not trending slightly down), which also suggests continued mortgage conformance in the future.

The other financial note is that the company spent $55 million repurchasing 1,892,643 shares at an average price of $29.06. They did this between September 3, 2013 to September 23, 2013. Not factoring in any dilution, this repurchase is about 1.96% of the outstanding shares. There is a market value to their share price where returns of capital are probably best given in dividends rather than buybacks, and it is very close to the $30 price range where I’d consider dividend increases would be a more efficient mechanism. Notably this time around, trading volumes were considerably higher than average. The public float of Genworth MI is only 43% of the total shares outstanding because the parent Genworth Financial owns 57% of the company, so the net buyback from the float was about 810,000 shares.

The buyback will alleviate the company from paying out $2.4 million a year in dividends at their current rate, or about a 4.4% yield, which is slightly better than their own investment portfolio, which at the end of June 30, had a book yield of 3.6% and coincidentally, a duration of 3.6 years.

I still believe the market is still placing a significant discount on the general perceptions of the over-valuation of the Canadian real estate market and other factors. While some of these concerns may have mid-term validity, they do not today.

I’ve been doing some stock research on the Canadian side and have been doing a little in the REIT sector and generally finding very little. However, of note was this press release from BTB REIT (TSX: BTB.UN) which caught my attention. Note the bolding of font below is theirs and not mine:

BTB’S payout ratio stronger than ever!

MONTREAL, Aug. 13, 2013 /CNW Telbec/ – BTB Real Estate Investment Trust (TSX: BTB.UN) (“BTB” or the “Trust”) releases today its financial results for the second quarter ended June 30, 2013, and announces the following highlights:

HIGHLIGHTS OF THE SECOND QUARTER OF 2013

66 properties

Over 600 tenants

4.5 million sq2 of leasable area, rental income growth of 24%Improvement of:

Payout ratio to 76.7% from 92.5% in 2012

Weighted average contractual rate for mortgage loans payable, from 5.15% to 4.67%

The message here is “Our payout ratio is higher, invest in us!”

I will leave it as an exercise to the reader why I would not invest in BTB.

The current game of chicken going on in the US Congress is good for media and may be financially profitable. I think most participants going into this negotiation concerning the debt ceiling thought that it would be a foregone conclusion that there would be some sort of settlement on the matter, but both parties seem to be sufficiently entrenched in their positions.

There is about a weeks’ worth of time before the US Treasury runs out of room to borrow money (via extraordinary measures), and then another couple weeks before they run out of cash entirely. This undoubtedly would create a market crash if this occurred and would result in a very large buying opportunity.

In other words, now is a good time to pick candidates for purchase in the event they are wholesale-dumped into the marketplace when other institutions realize that their T-Bills aren’t going to actually mature at par value.

It will likely not happen, but one can always hope – it is only at times when institutions and funds are forced to liquidate holdings that you can make the greatest gains from the market.