Interactive Brokers (Nasdaq: IBKR) is the best brokerage out there that is available to the retail level. They give me a degree of comfort that simply doesn’t exist in any other brokerage firm that I have dealt with. One of the reasons for their superiority is their founder, Thomas Peterffy, continues to push the innovation curve in such a manner that makes the firm cutting-edge.

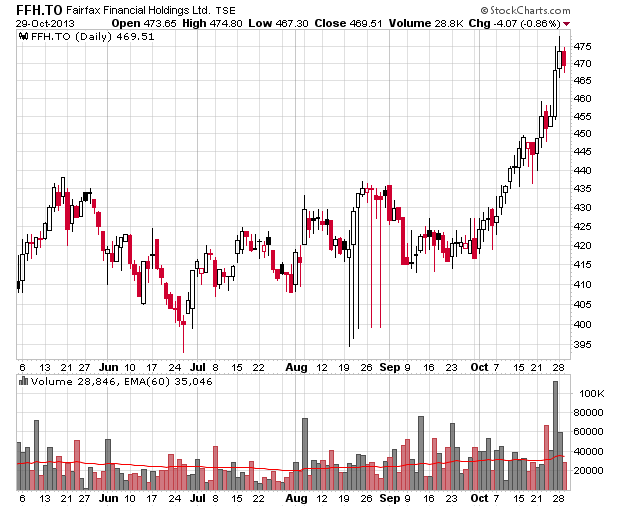

The company is publicly traded and has been on an unsual uptrend over the past few months:

The only reason why I have never put money in them is because the publicly traded entity is essentially a minority slice (12.4%) of the “true” asset and this creates all sorts of perversions of incentives that are not necessarily in shareholders’ best interests. It is a classic case of the underlying business being fantastic but the stock not necessarily being a good investment.

Anyhow, they have a tool that is relatively easy to utilize that highlights potential option strategies given the differences between the market’s implicit probability distribution and your own personal expectation of outcomes. Although I do not trade options very often (indeed, it is very rare that I do so simply because trading options is quite costly in terms of spread), this tool and this explanation is quite intuitive. If you do not understand how options are priced, this is a pretty good tutorial that avoids math.

Clearly understanding the math helps and I would highly recommend people learn some option pricing theory before considering trading them. Putting it mildly, options are a fantastic way of losing money if you don’t know exactly what you are doing. Options also appeal to gambler-types that love seeing huge rewards in total disproportion to the amount risked.