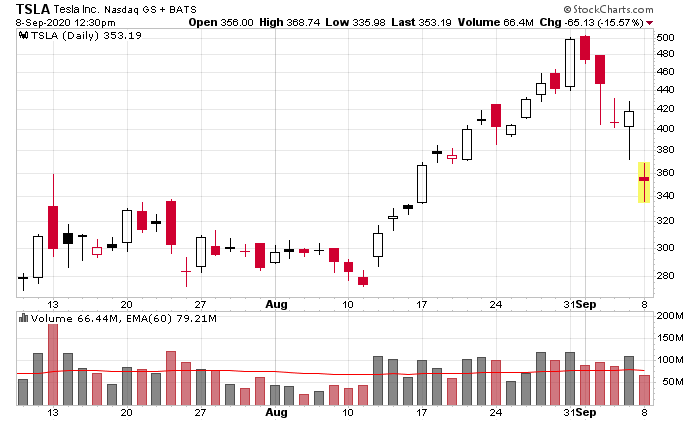

I’m going to use Tesla as the standard, but you can pretty much use whatever high-flying technology sector stock as a substitute (e.g. Zoom):

Some basic math – from August 11 to August 31, Telsa went from $280/share to $500/share.

It is really a shame that Robinhood removed their customer stock holding information since it is very illustrative what the retail momentum crowd is chasing. Just imagine seeing this chart, and on August 26th or 27th you finally capitulate and say I’m going in. You buy shares at $420 level (remember that number? Pre-split!), and on August 28 and after the weekend you are looking like a genius, up about 20% on your investment in a week. Now this is how you become a millionaire!

Fast forward a week in the markets, and suddenly your $420/share purchase is now sitting at a 15% loss from the cost. How much further down does this go before you capitulate, dump your shares, and then swear off gambling on these popular technology stocks?

This sort of thing happened in 1999-2000 all the time.

One of the few differences is that treating the stock market as a casino is even easier than ever. The emotions associated with gains and losses are all the same.

Another difference is that after the Y2K scare passed without any consequences, Alan Greenspan applied the monetary brake pedals (do you remember the days when interest rates were above zero?) and it was one of the contributors to the crash in March of 2000. This crash was preceded by an incredible amount of volatility in February 2000. Right now, gasoline is still being poured onto the fire in the form of fiscal stimulus and interest rate curve control.

I’d be curious what the average retail holding period of Tesla stock was in the past month. I’d guess a week or two at most.

Since there was likely much more broad participation in this upswing since June (the realization that markets are effectively decoupled from the economy), in order to make a check on the upward momentum requires a much more violent downswing. As the chart of Tesla above can attest to, this was a pretty violent downturn, and will shake out people that think the stock market was a one-way street to riches.

In the short term, if a trade feels comfortable to make, it probably is a losing one.