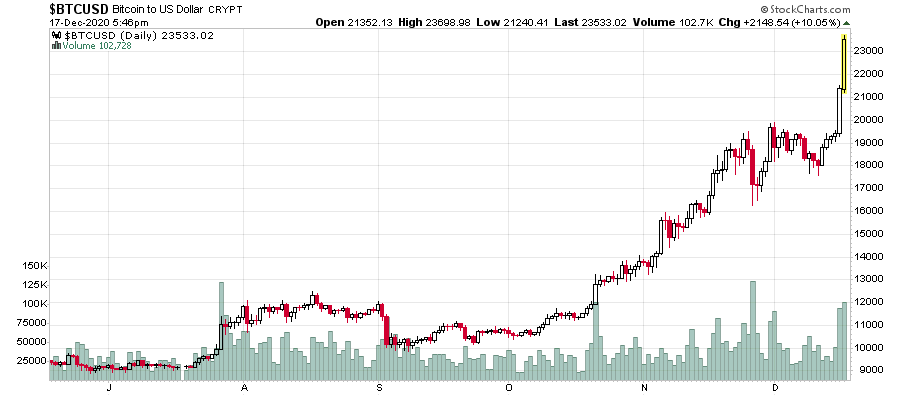

It is amazing how markets cycle from panic to mania so quickly. It is a lot quicker now than it was a decade ago – one theory is that this acceleration of sentiment is fueled by social media.

I’ve been reading a bit more about perception and reality (e.g. ages ago, I linked to a TED talk that discusses the non-correlation being able to see reality and survival) and this is quite apt to describe what is going on in the financial marketplace.

Many participants in the market depend on “sources” such as BNN, CNBC, Jim Cramer, Reddit, Discus forums, Youtube, and for a very rare few, yours truly to come to their investment conclusions.

They are all trying to figure out how to put cash to use, because cash in a 10-year treasury bond yields 80 basis points at present. A million dollars gives you $8,000/year in (pre-tax) cash, which is a pittance compared to alternatives. Going one step up, you can find a 5-year GIC at 175 basis points, but again, it isn’t going to get you very far.

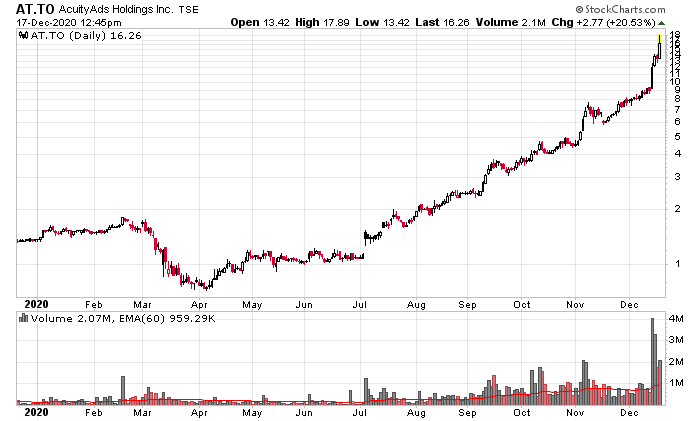

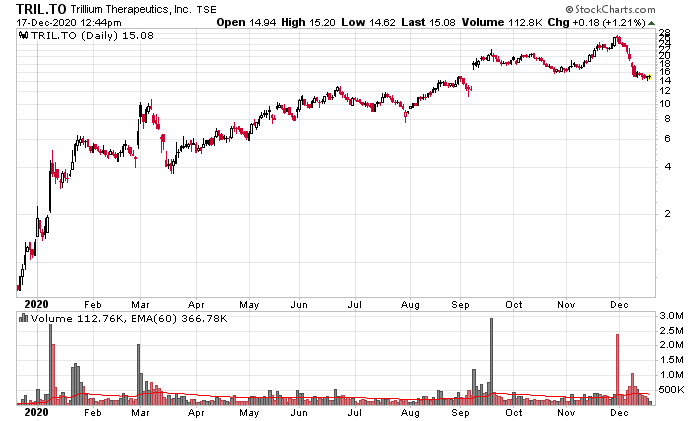

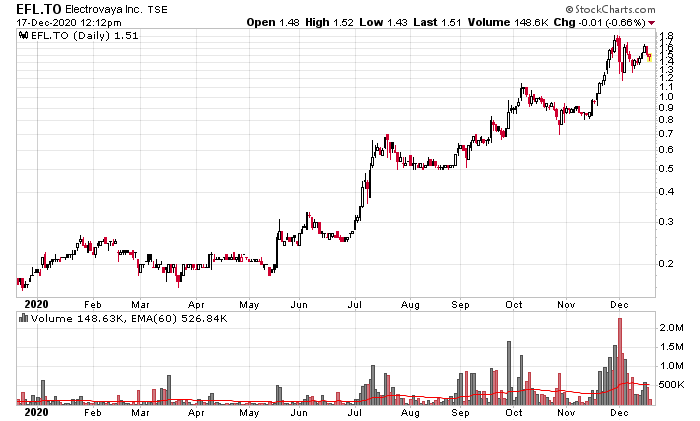

When markets appear to be stable, people reach for yield. A “reach for yield” market is exhibited when you see garbage rise, and a lot of sectors start incurring speculative fervor. We’re clearly in one of those market environments at present, a short temporal distance away from the March 23rd CoronaCrisis crash which lead everybody to the exits (yours truly was madly investigating opportunities) where quality was being thrown out the window. How times have changed – on very quick notice.

Institutions are in the same boat. They have to make their mandated returns otherwise pensioners don’t get paid and underperformance will cause capital to shift to those that bought and held Tesla at the beginning of the year.

I look at this Globe and Mail article about institutional managers buying Canadian apartments:

While many property deals are private transactions, Mr. Kenney cited some recent sales in mid-town Toronto that were completed at capitalization rates around 2 per cent, an astonishingly low level.

I ask myself what can justify 2%. For instance, CapReit (TSX: CAR.UN) in their last quarterly report stated their mortgage portfolio is an average of 1.93% at a term of 9.3 years.

While it isn’t clear whether the definition of cap rate in this instance included mortgage interest expenses (“cap rate” is not a standardized accounting term – you can make this number go up or down depending on how much leverage you employ), 2% is indeed a very low rate of return. Indeed, for it to make financial sense, you have to anticipate some degree of capital appreciation in the underlying property for the investment to make sense.

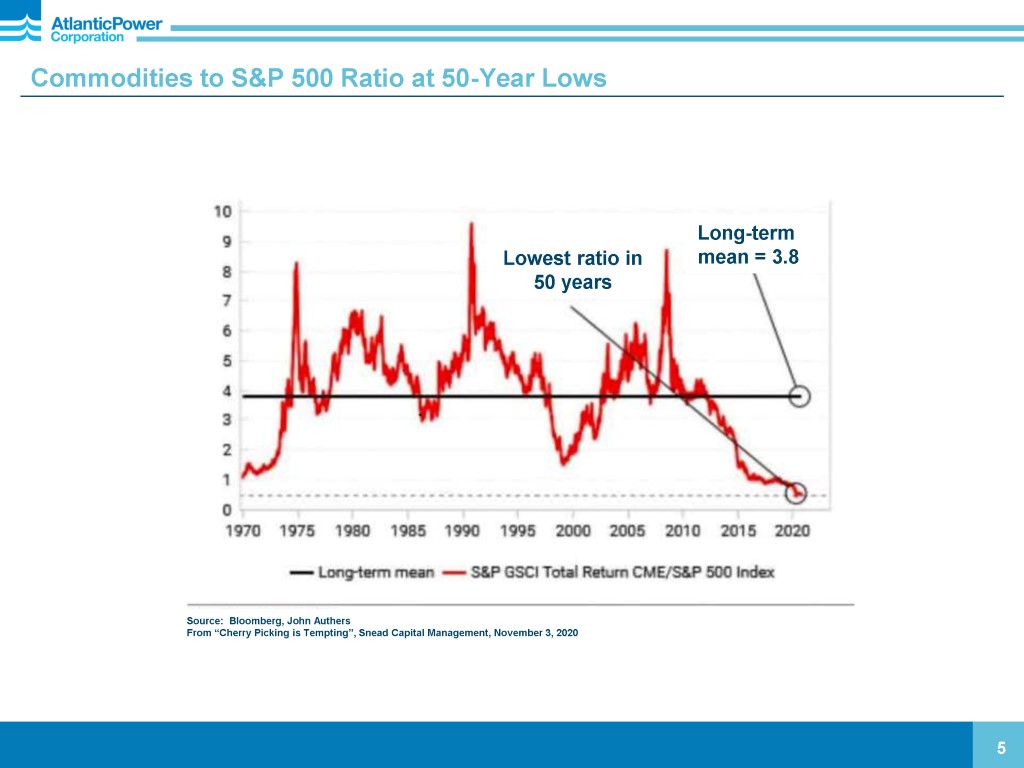

This low spread is not limited to real estate, it also includes the stock market.

(For the comparison above with CapREIT, I’ll tip the hat to Tyler (his Twitter) who has been discussing this concurrently and independently of the writing of this post, great minds think alike I guess!).

Let’s look at the S&P 500 top components. Apple, for instance, stock price $124, and the past year of 10-K earnings show $3.30/share, and relatively stable. So a bond-like earnings yield 2.7% for Apple stock. MSFT is $6 EPS and $214/share or about 2.8%. Facebook is about 2.5%, and so on. Of course in these cases you can make an argument that earning yields will grow over time and there is some franchise value. But it is shockingly close to these Toronto-area apartments that are selling for a current 2% (although given the choice of an investment in Apple or a Toronto apartment, I’d take Apple any day of the week).

Yields are very tiny now, and investors are going to chase them. High quality, such as Apple, will be rightfully expensive. But this yield chasing will make its way down the quality chain and companies that have no right to be chased down to 4% earnings yields will be done so because there is a huge liquidity avalanche out there that is looking for a home.

Realize when stocks trade, there is no cash or stock created or destroyed in the process; it is merely a transfer between buyer and seller. The amount of cash is the same, and this cash will circulate, being handed from account to account, while in the meantime the counter-transaction to that is the transfer of assets at higher and higher prices, until such a point that the amount of baked speculation on future yields will go to a low point.

If you believe those Toronto apartments will rise in price 10% a year for many years ahead, it would be completely rational to buy them even at single-digit negative cap rates, especially if you anticipate being ample future liquidity in case if you change your mind.

Likewise, for Apple, you could bake in a whole set of variables to justify purchasing it at a 200bps earnings yield, or 150bps, etc., citing a never-ending stream of inflation-shielded future cash flows. Indeed, that $124 stock price at 200bps would warrant an Apple stock price of $165, or a 33% gain from the current price!

I have no idea when this speculation house of cards will end, and can only conceive of a few scenarios of how it ends (one obvious “how it ends” would be the onset of inflation beyond that of asset prices – you’d see a 30-40% stock market crash). It is a very dangerous game of participants bidding asset prices higher and higher in the search for yield and appreciation. Apple today at 270bps sold to the next guy at 265bps, then to 260bps, etc., until the demand for that cash gets directed to some other supply that is not Apple equity.

Back in the dawn of the COVID-19 crisis when everybody thought we were going to die (April 5, 2020), I openly speculated the following:

This might sound a little crazy, but I can see the S&P 500 heading to 4000 before the end of the year.

Recall at this time when I wrote it, the S&P 500 was trading at around 2,500. Predicting a 4,000 index (a 60% rise) is crazy. I don’t think anybody on this planet did that except myself. We are living in a crazy world, where many are indeed going insane with COVID lockdowns and massive disruptions of a “normal life” that people are realizing is not coming back. And while the S&P 500 index will probably fall a hundred points short of 4000 before the new year, realize that going forward this is what it takes to be successful – not seeing reality as it is, but rather being able to adapt to what are inherently crazy circumstances in the minds of market participants.

Even if you see reality for what it is in the markets, it is not sufficient for your survival – you must understand the perceptions that surround the other participants.