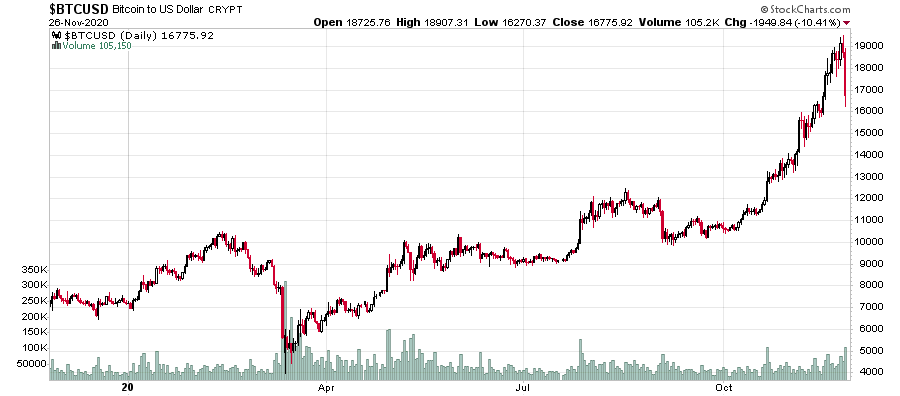

Today was the first day since the Coronacrisis where Bitcoin took a huge dive:

Speculating on reasons, I’ll offer three potential factors (it is likely a blend of these and other hidden factors):

1. US Thanksgiving resulted in all the automatic buying (ETFs and the like) taking a vacation, resulting in a demand drop and thus price correction.

2. A typical market reaction that occurs when things rocket up continuously for about two months – you get plenty of long players (FOMO!) and a lot of them decide at once to suddenly cash in their chips. Subsequently you get supply dumps of everybody’s trailing stops getting hit which causes a mini-cascade as we have seen. Happens with momentum stocks as well.

3. Speculation that the US Treasury Secretary will make privately held bitcoin wallets illegal. Most people own bitcoins through intermediaries (mainly crypto exchanges), but remember that the whole origin of bitcoin was to decentralize monetary policy. It is a myth that Bitcoin is anonymous – rather it is completely the opposite, with all transactions completely transparent for all to see. The blockchain database is just over 300 gigabytes at present and is available for anybody to download. The bitcoin wallet addresses don’t have peoples’ names on them, but presumably there will eventually be an association made unless if the transactions are done very carefully (i.e. with two parties that aren’t caught up in the usual electronic monitoring sweeps of large value transactions).

Transactions in bitcoins are also internalized off the blockchain and batched until some point where it is economical to post them on the chain itself. This is what practically happens as transactions cost about US$5 to post. This will get more and more expensive over time.

There are a couple analogies I can think of to the speculation of outlawing Bitcoin private wallets: Forbidding people to own (paper) cash without it being deposited into a bank, or forbidding people to own gold. These two were functionally the same thing since when (large scale) gold ownership was forbidden in 1933, US dollars were directly interconvertible into gold at US$20.67/troy ounce.

Another analogy is the pervasive usage of free web-based email providers and communication privacy. Even if you use an external email service, if you communicate with any individuals on a standard (obviously subject to government monitoring) web-based email services, your communication is going to be compromised by virtue of one side of the communication chain being monitored. Essentially the US Treasury is trying to forbid email communications between any individuals that do not use one of the sanctioned services.

============

Finally, it is well known that Microstrategy (Nasdaq: MSTR) adopted a treasury policy of holding bitcoins and their CEO gave an interview on CNBC today. The narrative is fairly well known, but at around 1:30 in the interview, the following words were said:

“What they don’t understand is bitcoin is a monetary network. And as a monetary network it is capable of storing and channeling energy over time without power loss.”

The words “storing and channeling energy over time without power loss” triggered my physics background on perpetual motion machines.

Indeed, crypto currency networks are huge consumers of energy. The amount of power being dumped into semiconductors keeping the bitcoin transaction network alive is very high. I’m not saying this is a good or bad thing (there are many other uses of electric power which are wasteful), but Bitcoin is structurally designed to incentivize more and more consumption (the larger the share you have of the network, the higher the chance you have of mining a block of bitcoin, or confirming a transaction for a fee) and hence one of the fundamental limitations of bitcoin will be how much silicon and electricity can be thrown into what (I claim) is the monetary equivalent of stacking one pile of rocks into a corner and then moving them to the other side of the room, repeated many times over.

Since cooling costs are one of the major costs of running a data centre, will it be a structural competitive advantage if you operate your data centre in a country that has very low average temperatures (can use outdoor air ventilation for cooling), coupled with being next to your own privately held nuclear reactor? Siberia anybody?