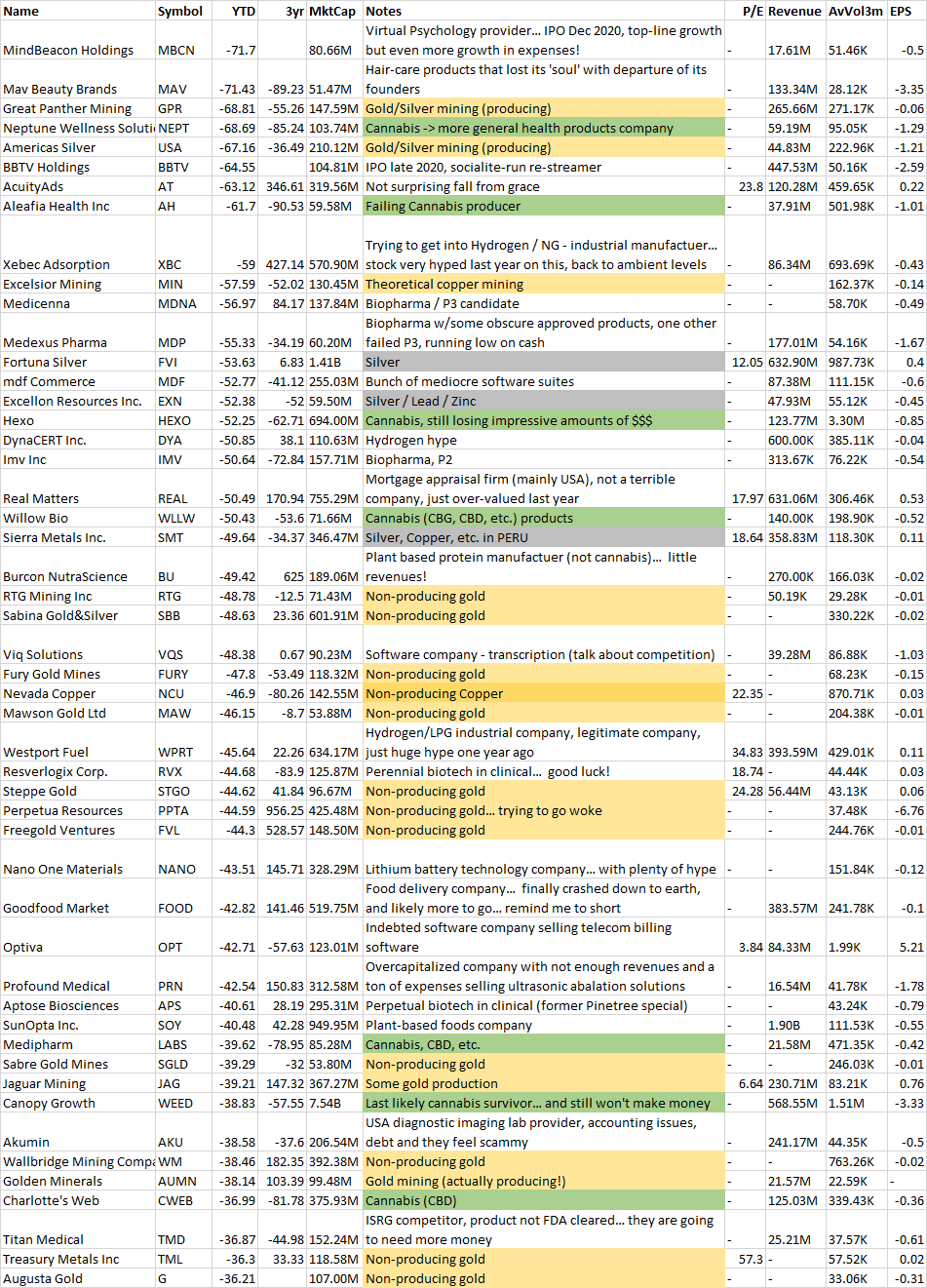

Just doing some general review and scribbling down some thoughts.

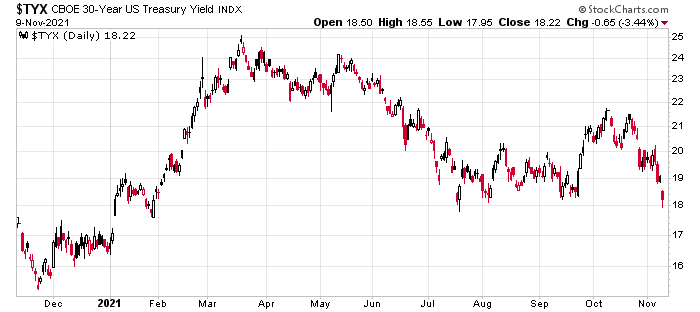

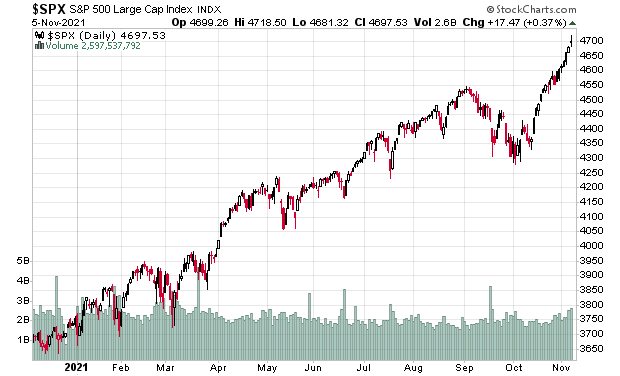

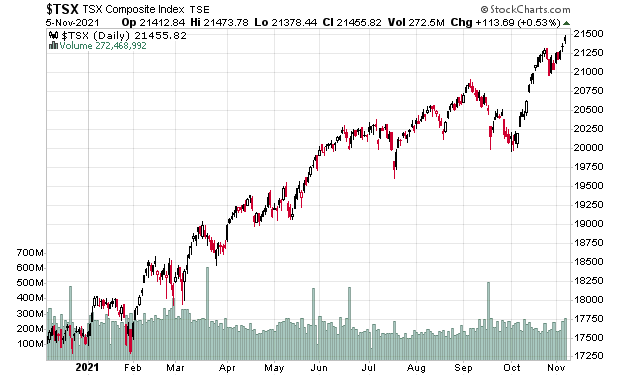

One is that the S&P 500 and TSX are up 25% and 23% year to date:

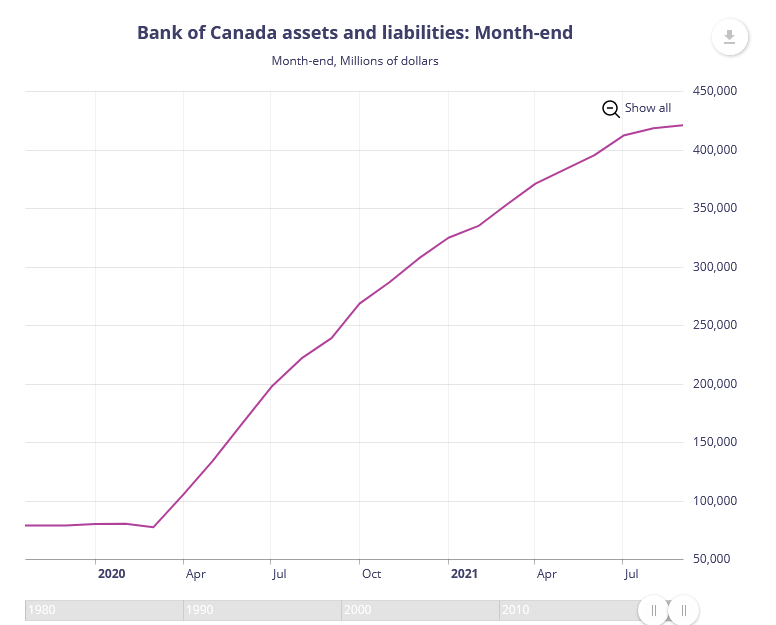

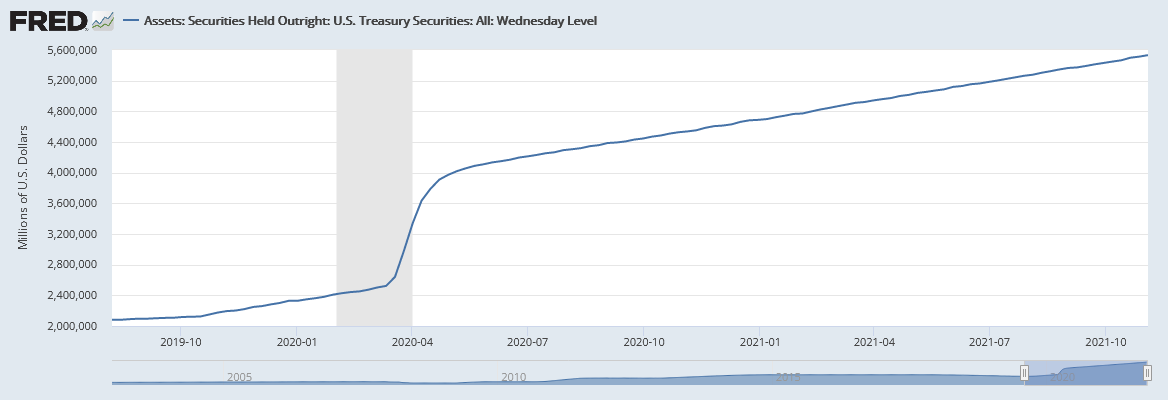

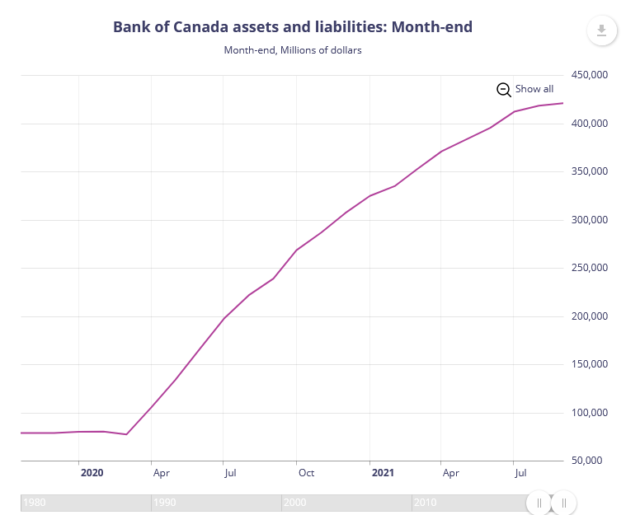

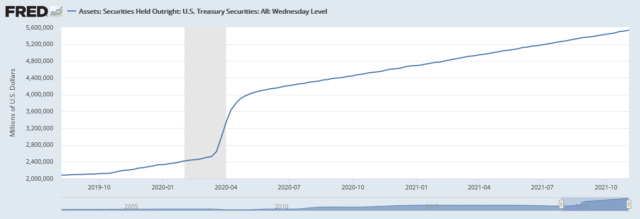

This is likely induced by monetary policy, with the US and Bank of Canada historically demonstrating a huge amount of QE:

The central banks have signaled that this party is slowing down.

Picture the flow of a notional dollar of capital from monetary policy.

Monetary policy has the Bank of Canada purchase a bond from a primary dealer (one of the big banks). The result is a BoC asset (government debt), and liability (reserves due to the bank). The big bank receives reserves as a credit at the Bank of Canada, which they can use to make loans. Customer X goes to the big bank and sees something that warrants taking out a loan. Big bank lends a couple dollars to Customer X (loan is the bank’s asset, Customer X has cash, at the cost of a yearly cash flow from customer (debit interest expense, credit cash) and to the bank (debit cash, credit interest revenue). QE makes it “possible” for the big bank to execute on this loan as they can do so more cheaply than if QE wasn’t in place, effectively making credit ‘cheaper’ and thus lowering the rate of interest.

In this scenario, the bank is the one suffering the default risk, and this dollar given to Customer X is not given to him by the central bank, so it is not money printing. The loan must be paid back, with interest.

Customer X takes the loan, and invests it in some widget machine with Company Y. Company Y takes the money to pay labour and materials needed to make the widget machine. The labour tends to spend it on various necessities (food, housing, consumer goods, etc), while the materials provider has to spend it on their payroll (labour) and capital equipment from Company Z, A, B, etc.

All of this is illustrating the flow of where the notional dollar of capital is generated and circulated – originating from a financial institution (the point of money creation) and circulating in the economy. Eventually profits from companies Z, A, B, etc., circulate into shareholder hands, and for the very rich that have nothing else better to do with capital (there is only so much food and drink and housing one can buy), gets slammed back into the equity market.

Clearly there is a point where you can just bypass all of this widget creation and just invest loaned capital into the equity markets directly, which seems to be the result of what has happened. The notional dollar does not get created or destroyed, but the path of where it flows is quite relevant. Depending on the speed it flows (monetary velocity) and where it flows, the economic outcomes wildly vary.

For instance, imagine a world where 99.9% of the cash is held in the hands of day-traders only, circulating amongst them within the Nasdaq and NYSE, and these participants have no interest at all in building widget machines. We seem to be increasingly in an environment where a lot of this capital is held in the financial and not real world.

When money bubbles out of the financial world into the real world, this is when we start seeing a chase up the prices for real assets. For instance, going back to our fictional world where day traders own 99.9% of the financial capital, they might discover that they need to eat food. But since the food markets have been so malnourished, all the day traders can do is just keep bidding up the few morsels of food remaining, until prices reach some absurd high – a typical hyper-inflationary scenario. Indeed, if the day-traders have to eat 100 units of food, and only 70 units of food are available, there is no amount of financial capital available that can satisfy the demand.

One can imagine that the high amount of financial capital available would dramatically increase the volatility for real goods and services when the carriers of financial capital recognize an imminent need.