Vector Acquisition Corporation (VACQ) is a SPAC that has an agreement to merge with Rocket Lab.

Rocket Lab is SpaceX’s number one private competitor, but it has several competitive disadvantages. One is that Rocket Lab’s product offerings do not include heavy launches. The other is that their rockets do not land by themselves (although they are reusable to a certain extent).

As such they are receiving a valuation of much less than SpaceX’s private placement valuation (SpaceX was estimated to be around $70 billion). Rocket Lab’s enterprise value was estimated to be around $4 billion.

The revenues scale accordingly – Rocket Lab estimates around $70 million in 2021, while SpaceX is reported to be around $2 billion in 2019.

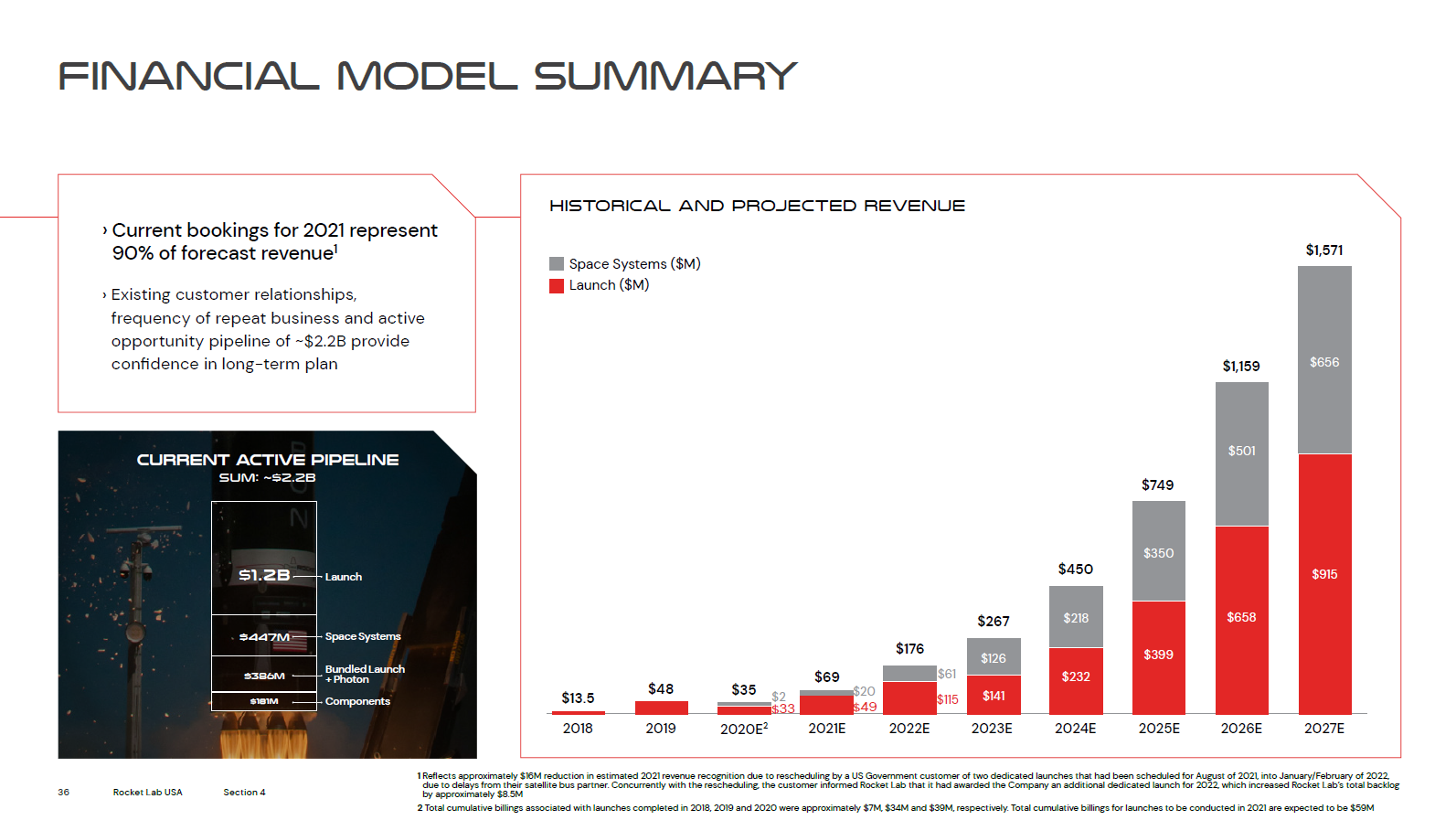

Just like most SPACs, they promise a quadratic increase in revenues:

If I had a nickel for every SPAC that promised such a revenue trajectory… I’d be richer than had I invested in these SPACs!

Space launch systems are very capital intensive and there is a certain economy of scale that is required to do this successfully. Blue Origin (Jeff Bezos’ firm) is another competitive in this domain (and of note, they have seemingly failed to get that point of scale). It could entirely be the case that the launch for small satellites (especially constellations of micro-satellites) is a competitive space where no firm will receive outsized profits – instead, the profitability will be through differentiation and also cost controls (SpaceX’s landable rockets would likely give them a cost edge over competitors at present). The differentiation will most certainly be with maximum launch capacity – there is only so much you can do with weight limitations on satellites.

The other component of competitive advantage in space is government relations. They are a significant source of revenue, especially in the military domain. Nobody is better in GR than Elon Musk.

I’ll be watching this one, but at the offering price I’m not interested. SpaceX receives a premium valuation for very good reasons.

Sacha,

Got in at issue price for MDA and got rid of it at around 17-ish.for a quick buck – this space is just too competitive.

Do you still hold Yellow in the same high regards? Any concern with the decline in digital revenue?

Thanks.

MDA and Rocket Lab are in two different domains, albeit both deal with space systems.

Yellow is performing to my expectations, although they were a lot more attractive at $7-8 pre-Covid compared to what they are right now. The shocking thing is that Covid seemed to have little effect on the business. That surprised me as well as the rest of the investment world.