Gas prices are the most visible price displayed on the entire planet. It is the most transparent price in the world – you go near a gas station, prices are posted and visible a hundred meters out.

With visibility comes politics. Especially in Canada, it is a perennial occasion to read of news articles claiming price collusion, and politicians claim to act in the public interest against price gouging, etc.

Cue in the headline that the US administration is deciding to release 1 million barrels a day out of the US Strategic Petroleum Reserve for the next 6 months.

If fully executed, this will drain about a third of the reserve.

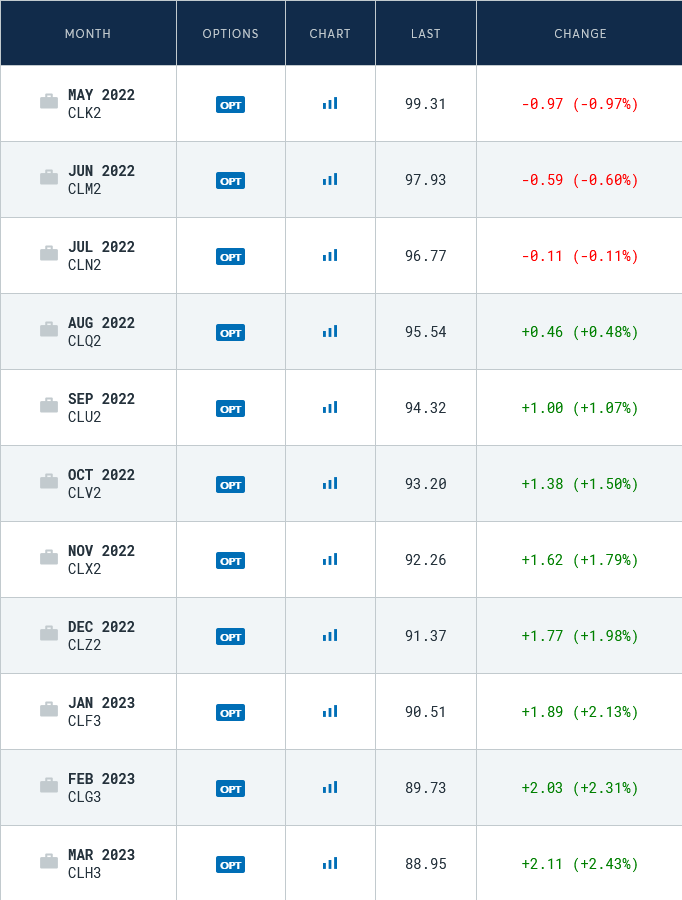

However, telegraphing this move allows traders to take advantage of the situation. You see this with a re-shaping of the oil futures curve (it was more dramatic when the preliminary news came out a couple days ago):

Back in 2020 during the middle of the Covid crisis, this curve was in the inverse direction – short term oil was priced much cheaper than longer-term oil. The reaction by the market was to store oil on tankers (bidding up tanker companies in the process) and arbitraging the time.

This is an inverse of that situation – sell spot oil (which is about $15 over 1-year out pricing), and long future-dated oil, and perform an arbitrage on the price difference. This is assuming that the inventory will actually be refilled in the future. This is a big assumption.

I do not think it will be that easy. Energy is highly in demand, and supplies will be more and more difficult to procure, especially within North America, where we have mal-invested in our energy production for quite some time.

If anything, this decision is a sign that my bullishness on fossil fuels was too low an estimate.

Having a strategic reserve reduces price volatility as if things really hit the fan (e.g. if the Saudis for whatever reason couldn’t export anymore) you had some time to work with. Every million barrels that gets pulled out of the reserves reflects an increase in future volatility since the price curve for fossil fuels is highly inelastic.

This is not to say that the upside will not continue – we could see a quenching of demand in our rising interest rate environment, or if we get into a recession. High energy prices also have a way of reducing energy usage.

But recall that world oil consumption only dropped from 100 million barrels a day to 91 million barrels in 2020 (the Covid year), when everything was virtually shut down in most places for at least 3 months. A recession will not drop total consumption by 9 million barrels a day – it will be far less than that.

It doesn’t take much of a supply imbalance to change prices – the fossil fuel market is inelastic. But right now, the price pressure is most certainly on the upside, and the SPR release is something to cause one to be more bullish of, especially since it is easy to see the political motivations behind this decision – the Democrats in congress right now are looking like they will be smoked in the upcoming November mid-term elections and high fuel prices, being as visible as they are, is one reason why.