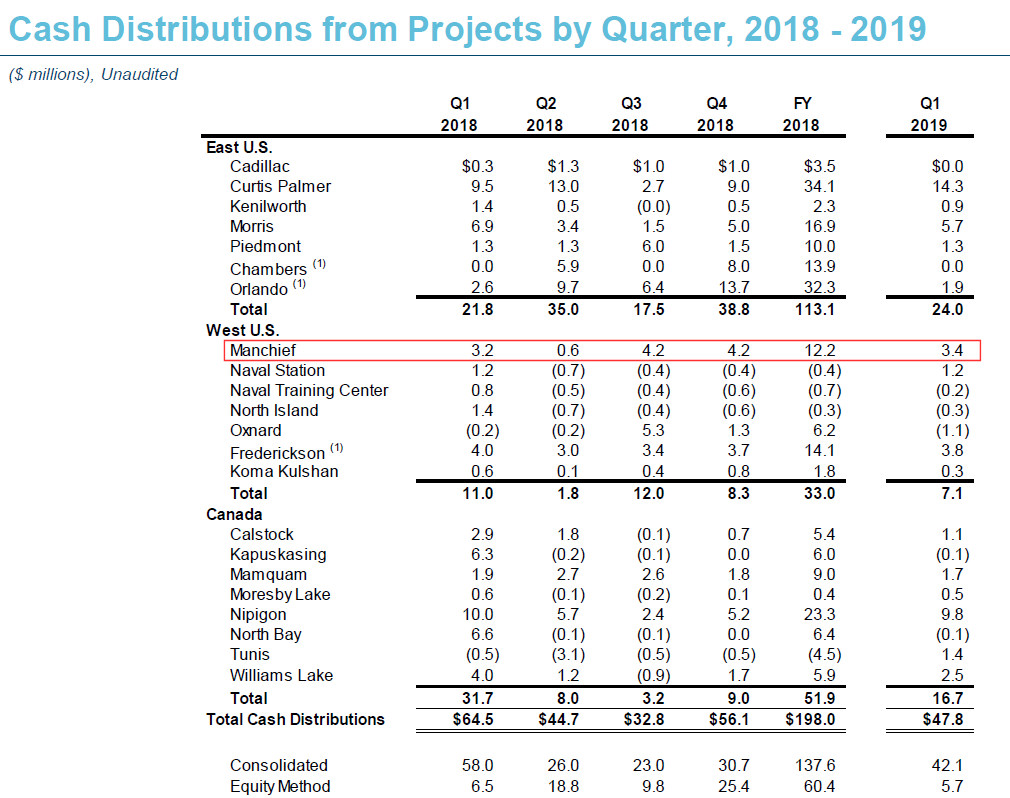

Atlantic Power (TSX: ATP) today announced they are selling their largest power producing plant (Manchief) on May 2022 for $45.2 million. In the meantime, Manchief will continue operating and contributing cash – in 2018, the cash generated from Manchief was 12.2 million (and indeed this number was somewhat lower than it could be given there was a turbine installation performed in 2018).

Manchief’s power purchase agreement expired on May 2022 and the primary customer of the electricity had an option to purchase which was exercisable on May 2020 or May 2021.

I’m guessing instead of stranding the asset (such as what happened in their San Diego operation, which was located on US Navy leased land which they could not further extend the agreement on), they decided to take the money and run. Clearly getting rid of an asset generating $12 million a year in cash for $45 million is not the best economics, but this is a part of dealing with a legacy business with power purchase agreements that were signed at much more favourable terms than what is available today.

Mansfield produced 300 MW of power, which makes it nearly a quarter of ATP’s net generating power (1,259 MW, not including the biomass plants that it will be acquiring).

In the meantime, the company continues to chip away at its debt and is on a relatively comfortable trajectory to doing this even as their legacy PPAs expire. In 2020 the next PPAs due to expire had a FY2018 EBITDA of 9.6 million (out of a total of 185.1 million for all projects) and distributed cash of 13.9 million (198.0 million). There are no PPA expirations in 2021.