Chris posted a comment with the following question:

Do you have any thoughts on Canadian Pref shares? I’m watching a few for potential multi-year hold.

I asked for his thoughts first, and he replied:

I’m seeing a few yielding around 7% (taxed as dividend), with resets 3 to 4 years out. I can’t predict where they 5 year bond will be at that time, nor can I pick the bottom on these moves, but 7% for a few years followed by a reset at 5 year bond + 2.9% (based on $25, as you know) seems like a decent place to put some longer term money to work. BAM.PF.A is an example. Prefs are a bit outside my wheelhouse, but it seems that they present an opportunity every now and then. Thanks for any insight.

…

I forgot to mention that Brookfield has been buying back some of their prefs in the open market recently.

Chris – One thought is fairly obvious and you touched upon – those 5 year rate resets are awfully sensitive to the bond yield!

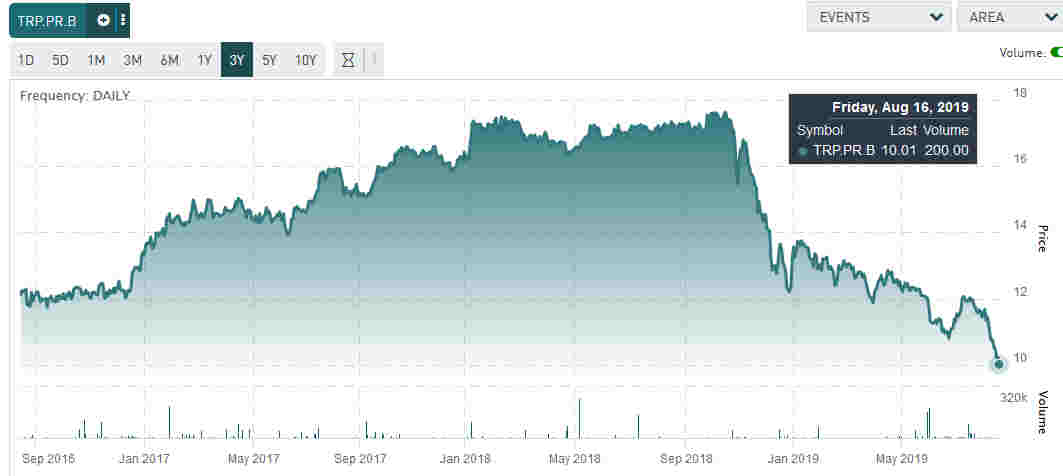

Example (above): TRP.PR.B (current coupon 2.152%, resets at 1.28% above 5yr, the reset is June 2020) – an investor since October 2018 will have lost 45% of their capital to date (when the 5yr yield was roughly 240bps)! That’s very heavy, and a double-whammy because the equity from October 2018 to present has gone up! Normally you’d expect capital gains/losses for preferred shares to be muted to the equity. The company itself hasn’t materially changed in credit profile.

Currently the 5yr government yield is 121bps – at present rates you’ll get a reset at 6.2%, but you can be sure if 5yr yields go down to 60bps (which is conceivable and mirrors the lows a few years back) TRP.PR.B will be trading at around $7.60-ish, all things being equal, or almost another 25% of capital loss!

There also appears to be a law of dividing by small numbers effect going on. Let me illustrate with an example – pretend something yields 3% at present. Going from 3.0% to 2.5% is a 17% difference. Going from 2.5% to 2.0% is an 20% difference. Going from 2.0% to 1.5% is a 25% difference – low-rate reset preferred shares such as TRP.PR.B are getting absolutely killed because of the small denominator.

So if you want to take your 6-7% coupons and run with them, you need to take into consideration that there’s a good chance that you won’t be able to unlock the capital without taking losses, and ultimately you want to eventually see a day where interest rates are higher than when you initially purchased the preferred securities – who knows if/when this will be?

Hence, those 5 year rate resets are much more risky than people probably thought – they have been wildly volatile in the past five years.

You can dampen the risk by buying rate resets that are further out in time (e.g. resetting 3, 4 years from now) but they still trade quite sensitively to the overall 5yr government bond rate. Fixed rate (straight) preferreds are another option (albeit with different rate sensitivity). Most minimum-rate guaranteed preferreds trade very expensive (e.g. PPL.PR.K).

Of course if you anticipate 5yr government rates will increase, the inverse of the above scenario applies (i.e. potential for significant capital gains).

With the US Fed anticipated to drop short term rates, there’s a good chance Canada will be following to some extent and this will continue to depress the entire yield curve. I’m not offering an opinion on future rates, but the trend clearly has been negative (i.e. bias towards lowering rates) since the beginning of the year.

Another comment I will make is that I’ve generally noticed equity presents a much more attractive risk/reward than the preferred shares in a lot of issuers. If you’re just buying for income, why not just buy equities that give out nearly the same yield with a lot more potential for upside (including dividend increases)?

Also, I have not seen another asset class that is so ripe for tax-loss selling. If you were sitting on a 45% loss on TRP.PR.B but really wanted the exposure, I’d sell it and buy something very related instead (e.g. TRP.PR.C) and this avoids the 30-day wash sale rule.

So to conclude, there appears to be quite an element of risk unless if you’re planning on holding these securities strictly for income for a considerable period of time.