Few appreciate liquidity until you don’t have it, and then everybody wants to rush out the exits – this is when you get price crashes.

With major US regional banks trading down significantly (examples: FRC, WAL, ZION, PACW) and with SI, SIVB and SBNY going into FDIC receivership, there will be some other consequences. I’ll write a few of them here:

1. The Fed is offering a “treasuries for par for one year” program. So if you were stupid enough to buy long duration last year, you’ve got a one year term grace period to figure things out – although inevitably your shareholders will have to choke on the loss (unless if the Fed really bails out everybody by dropping interest rates!). This can only be described as a time-limited QE action! However…

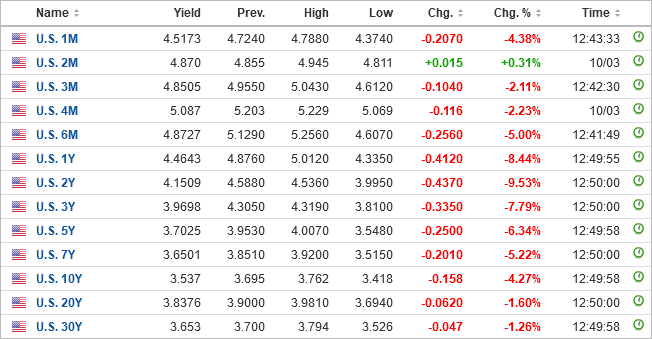

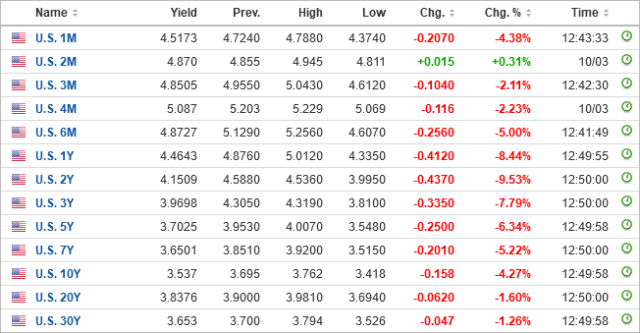

2. The yield curve has gone bonkers, with longer-term yields trading significantly down and the Fed Funds rates basically indicating one more quarter-point rate hike and that’s it:

3. Bitcoin and Gold have simultaneously received a huge bid, with BTC up +$4,000 to US$24,000 and an ounce of gold up $50 to $1915. There is obviously a huge pressure in the market for safety at the moment.

What is the big picture here?

1. A bank’s traditional model of riding the yield curve does not work very well in an inverted yield curve environment. The yield curve has been inverted for many months, and customers with zero-interest deposits are not going to be a stable source of capital if you’re running a bank;

2. The question of inflation – the central banks have a mandate to stamp inflation. This is also a function of what the BoC referred to as entrenched expectations of inflation. Ultimately the labour input function of inflation will get stamped down if we start seeing mass unemployment claims come to the fore. I’m suspecting that my prognostications of this happening in January-February 2023 (which I made later in 2022) are simply delayed – I’m going to guess we will see more of it coming, especially in the second half of the year;

3. “This can’t happen in Canada!” – the Bank of Canada in 2008 took considerable measures to backstop the major Canadian schedule 1 banks. The USA has JP Morgan, Bank of America and Citigroup, while Canada has Royal Bank and Toronto-Dominion as key global banks. While the stability of the banking system will be defended at all costs by central banks, whether equity/debt holders or not will take a bath is another question.

Let’s review the business model of a bank. Inherently it is a very simple business. You take deposits from customers and (usually) pay them for the right to hold their money for a time. Say your rate of pay is 2%. Parallel to this, you also lend money out to credit-worthy customers at a higher rate of interest. Say that you lend money out at 5%. In this example, for every dollar your are able to recycle, you get a 3% interest spread. Then you have to subtract all sorts of expenses relating to hiring staff, maintaining IT infrastructure, leasing branches across the country, etc., and after paying taxes on the residual, your shareholders make a profit.

Making a 3% interest spread is not efficient. To increase this amount, you do the procedure twice over – take in one dollar of customer deposits at 2%, and loan out two dollars to customers at 5%. You can do this because you have a deal with the central bank that if you keep a certain amount on deposit, you have a license to create money and leverage it off your net equity figure. If you can pull the 1:2 deal as described on this paragraph, then your effective margin is 6% on a dollar of deposits due to the power of financial leverage.

The magnitude of money you can earn is even greater if you raise a hundred million dollars in equity financing and use that to lend a billion to customers, which is typical for most banks.

Where does this blow up?

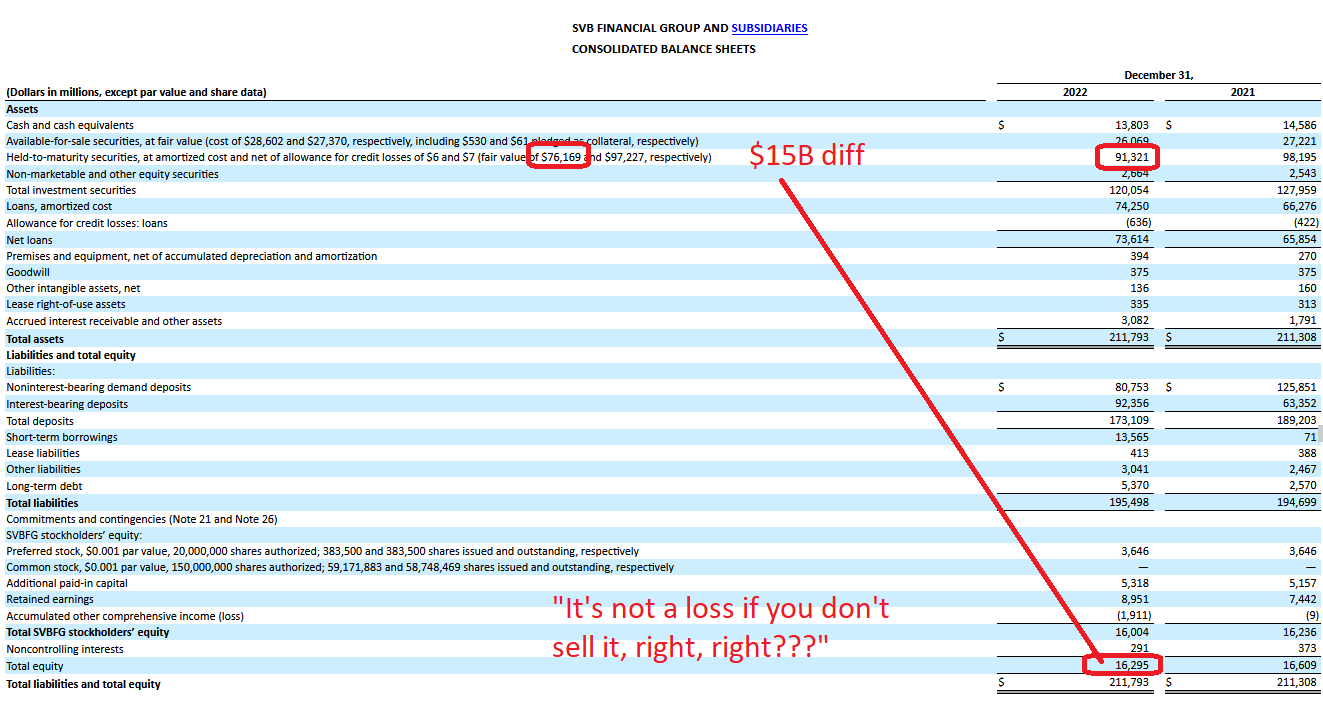

One is what happened to SI/SIVB/SBNY – the bank took their liquid customer deposits and dumped them into long-dated government securities which could only be sold for less than what they paid for it, coupled with the depositors wanting their money back, now.

The second mode of failure is if the customers you’ve loaned money to don’t pay back their loans. We haven’t seen this to any material degree (yet). However, if we start seeing defaults on construction loans in Canada, this might become material.

The third mode of failure is more subtle – for a prolonged period of time, you can’t obtain deposits from customers at a cheaper rate of interest than you can loan the money out for. This could happen if would-be depositors start to demand higher rates of interest, coupled with your customer screening division not being able to find credit-worthy customers to lend money to.

4. Financial companies in themselves do not generate wealth in an economy (i.e. manufacturing, farming, natural resource extraction, Netflix, etc.) but they facilitate it. Inevitably if the business that financial companies are financing are unprofitable, financing companies cannot be profitable by definition (businesses won’t be able to pay back loans). Companies that produce economic value, as measured by profitability, will survive this mess, while those participants that are forced to rely on low-cost capital will wither.

5. Hold onto your wallets, this will get pretty wild. I was originally thinking “sell in May and go away”, but perhaps I was a couple months too late with this prognostication.

More later.