It’s always good to review some companies that have crossed your radar in the past – the library of knowledge that gets built up becomes an investing competitive advantage when the market decides to vomit.

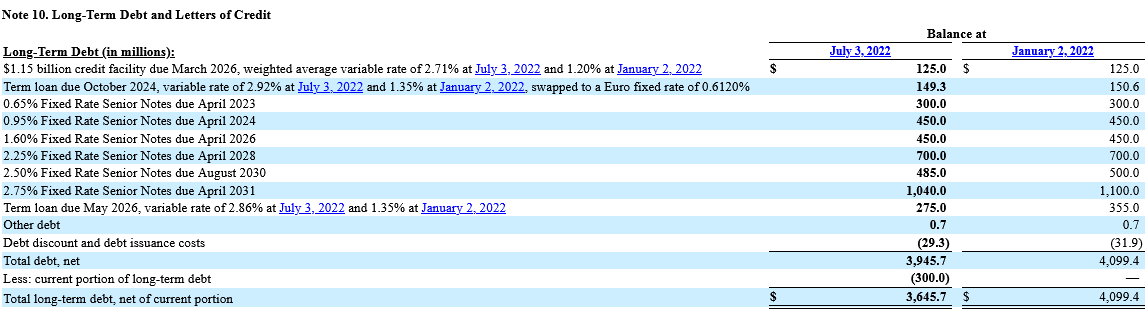

Teledyne (NYSE: TDY) got on my radar when they acquired FLIR Systems (I was a shareholder of FLIR at the time). They are competently managed, in a market space that is relatively insulated (they have a lock on certain technologies and are strategically well positioned). However, they took on a ton of debt when they took over FLIR and here is the salient table:

We see a structure that is $550 million variable, and $3.4 billion fixed rate. Clearly the highlight debt offering was the $1.1 billion of 2.75% notes due April 2031!

TDY currently makes an annualized operating income of $900 million. Current annualized interest charges are approximately $100 million. The residual after income taxes will be poured into debt repayment over the next few years. However, the problem from an investor perspective is that this capital has an effective return limitation – for instance, the 0.65% notes due on April 2023 (half a year from now) will effectively be re-financed at higher rates via the credit facility. Ironically, the Federal Reserve increasing interest rates improves the return on capital of TDY’s debt repayment and because most of it is fixed for the next 9 years, an increasing interest rate structure should not harm the company too much.

However, the debt burden poses significant limitations on shareholder returns (traditionally this has been in the form of share buybacks), in addition to making the valuation from an EV/FCF perspective even more expensive. The share buyback history of TDY in itself is a fascinating story – the last time they did so was in 2015.

Despite the business being great, it suffers from the same problem I identified when the FLIR takeover was happening – it is just too expensive. They did crash down to $200 during Covid, where they may be worth considering. Unfortunately if it got to this point, there’s likely to be a lot of other stuff on sale at the same time. But I continue keeping it on the radar.