A few things caught my attention today, and it is likely that means that the next few days (i.e. the short term) there is going to be some turbulence in the stock markets. If you have some leftover cash, after this storm purges some weaker holdings out of their positions, it’ll be a better time than not to load up.

First, the commodity that seemingly everybody in retail has talked about ad nauseum as the salvation to currency depreciation (gold) has cratered today:

This ~US$100 drop in gold is significant. The last time it got dumped badly was during the Covid-19 crisis where people were seeking liquidity in the form of cash at any price possible. Beyond that you have to go back to late 2016, and I think this was due to threats of interest rate normalization (does that feel like a long time ago!).

The psychology of the situation is telling. Gold was the crowded trade where everybody piled in because they were comfortable in ordering the shiny yellow metal. It was the hedge against the collapse of the currency and economy due to COVID-19. After it eclipsed $2,000/Oz, that was a catalyst for people to assume it was all systems go, and people were pronouncing price targets of $2,500, $3,000, etc., per ounce. Instead, the bottom is falling out, and the question is how low this price will have to go for the people that got in at $2,000+ to bail out.

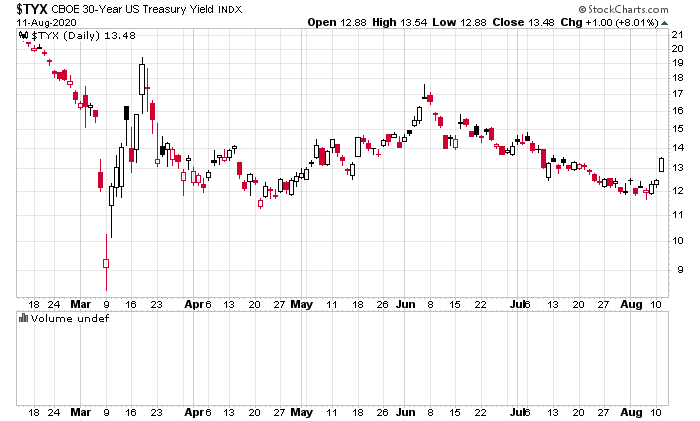

What’s even more interesting is the rise up (some 10bps or so) of the 30-year US treasury bond:

This is not a huge rise, but it is sharp. Rising long-term interest rates have many spin-off consequences. Since the Federal Reserve effectively controls the yield curve at present, they may be pushing for larger spreads. Tough to tell at present. The assets of the Federal Reserve continue to be flat in the month of July.

I’m going to guess there will be a spike of equity volatility in the next few days that will follow this minor tremor. It will be enough to get weak hands out of the market and confuse people about future market direction – negative headlines and worries will once again permeate. A great time to deploy more incremental cash, similar to when the markets vomited in the second week of June.