The S&P 500 is up another 100 points today, purportedly on a jobs report that the US hired people in the month of May (everybody was expecting layoffs). For example, the unemployment rate expected was 19.8%, while the actual rate was 13.3%. Suffice to say this was a shock.

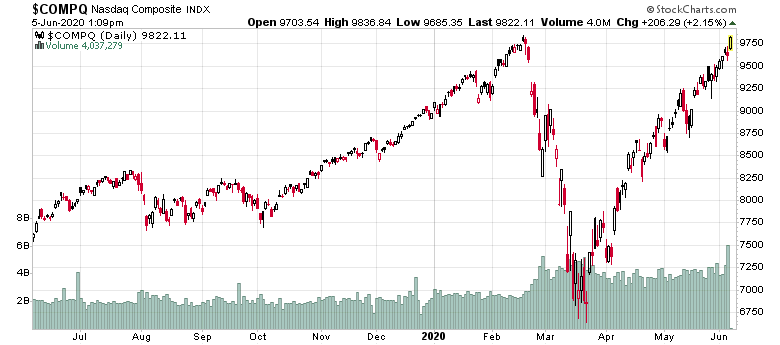

So everything’s going crazy. Cruise liners are up about 20% (they’ll be able to raise another round of financing and sail through it). Energy stocks are going through the roof. There are all sorts of indications of a market recovery, and indeed, the “V” scenario happened:

Recall my daily rule of “only sell in up markets, buy in down markets”. There will be days things will go down, that’s the time to buy. On a day like today, the only real option is to lighten up and raise some cash. You’re too late if you do the opposite. Today, and especially for those in the past month, those that have cash on the sidelines are hurting. The only worse feeling in the stock market than losing money is to watch everybody else make money while you’ve got a pile of zero-yielding cash. The news headlines are going to gravitate away from Covid-19, protests and now gravitate towards recovery and give people a feeling of comfort. Again, this will be false, since it will be built up on a pile of debt taller than Olympus Mons, but this is a medium term consideration and not short-term, which will be euphoria.

You are also seeing the start of the capitulation of the gold market, which is down about $40 per ounce. Although the downside here is not going to be extreme (10-20% from the US$1,780 peak?), holders in gold will be wondering alongside those holding cash whether they should dip back into the markets at ever increasing prices. There will be a significant contingent of people holding on to hedge themselves against the excesses of monetary policy, but there are also a lot of “loose” holders that have held paper gold which will want to catch the equity train. In fact, for those contemplating dipping back into gold, consider that the Canadian dollar is likely to rise in the future due to the resurgence in commodities, so valued in Canadian dollars you will probably be able to pick up gold for relatively less.

In these sharp rallies, there are going to be two-three day periods where you will see volatility spikes and the main indexes will dip down, usually caused by some transient headline. These are really the only opportunities to deploy cash. The only factor is when they will happen – it is difficult to predict these sentiment spikes. These spikes down are designed to wash out very short-term holders (this tend to be retail investors very new to investing that are skittish to volatility and because they tend to act in swarms, it amplifies price changes), but the overall trend is going to continue to be up as long as Central Bank rocket fuel propels the market.

Speaking of which, by the end of this year, the Federal Reserve is going to step off throwing gasoline onto the fire, and depending on how ridiculous things get, may even signal an increase in interest rates next year (the buzz-word will be “re-normalization”, very ironic since nothing is normal now). Any rate increase will be nothing extreme – just a quarter point – but even they will start to recognize when the S&P 500 hits 3500 that they should be applying some brakes otherwise they are getting ready to engineer the market crash of the 21st century that will make the 2008-2009 economic crisis look like a correction. Central Bank interest rates cannot rise too much because there is just too much debt.

My last note is a very easy prediction. Zoom stock (Nasdaq: ZM) in three years will be lower than US$208/share. The borrow is extremely cheap right now, but once the Federal Reserve rocket ship stops, this is probably the easiest short candidate I have seen in ages. I wouldn’t short it now because all of the index-based buying can make it even more ridiculously expensive. But I did note that Zoom sent me a spam to my inbox offering me 30% off a yearly subscription (I was month-to-month) and this is more than their usual “buy 12 months for the price of 10” offer, which means that their management is smart enough to know their gravy train is ending, and ending soon (get the years’ worth of deferred revenues while you can!). Microsoft, Google, and even open source options are all competing for this market and Zoom has little in the way of competitive advantage other than incumbency protection.

Have a good weekend everybody.