There are a couple hot assets that are down in the upper-teens percentages today. One is Bitcoin, but I’ll let other financial scholars write about it.

The other is equity in Turquoise Hill (TSX: TRQ), which is an entity that is 50.8% majority owned by Rio Tinto. The TRQ entity owns 65.9% of Oyu Tolgoi LLC, a Mongolian corporation that operates the Oyu Tolgoi mine, which currently is mining gold and copper. Copper represents the vast majority of revenues (roughly 75% in the 9 months ended 2020). While nominally Canadian, the primary operating entity is Mongolian and their operations are consolidated into TRQ’s financials. They report in US currency.

The company is facing significant issues concerning an ongoing dispute with the Mongolian Tax Authority, and also operational concerns regarding the expansion of their copper mine. While the GAAP financials are showing profitability, one quick look at the cash flow statement shows that the entity is (not using formal finance terms here) bleeding cash like crazy.

The first nine months of 2020, they spent $817 million on property, plant and equipment, and their net operating cash flow was negative $29 million.

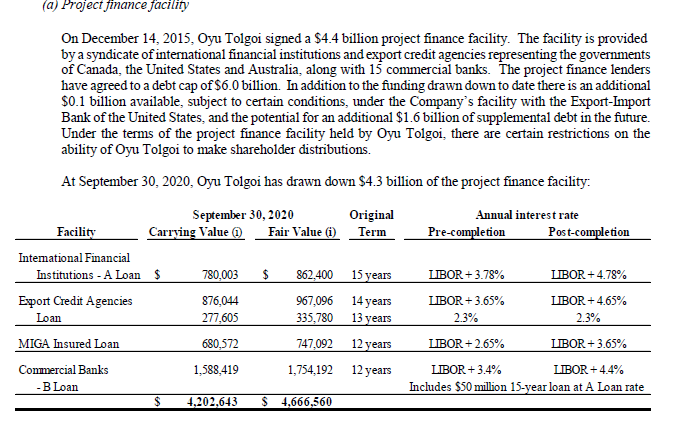

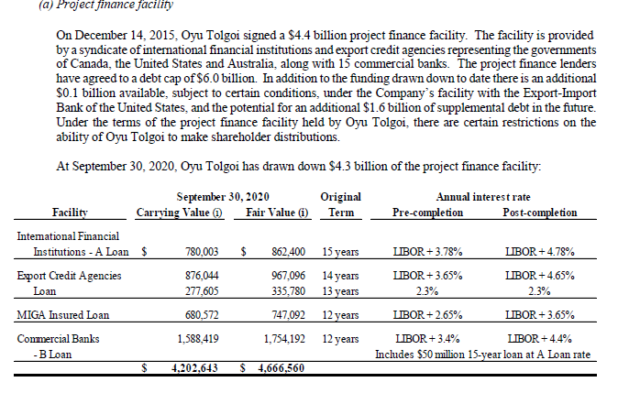

At the end of September 2020, they reported $1.4 billion cash on the balance sheet, but this is offset with $4.2 billion in long-term debt, primarily consisting of a project finance facility:

They have another US$1.6 billion to draw out, but there are conditions regarding this which I won’t bother posting about here.

Last month there were news pieces about a tax dispute brewing, and today TRQ announced they are taking it to an international tax tribunal. It looks incredibly messy.

This post is not about a rigorous financial analysis about the viability of the copper mine expansion, but rather about the risk of investing in foreign jurisdictions – I know very little about Mongolia and it is very difficult to sort out how much of this is political, or false positive promises, or whatever. All I know is that an investment on the simple narrative of “Copper and Gold will go up, therefore I should invest in this” has been shown to have embedded risk that is very difficult to quantify, and quite likely the stock price was not pricing in correctly.

Also, in such majority-controlled situations, it is unlikely that the parent (Rio Tinto) will take actions that will give minority shareholders a fair shake. If there is a bailout in the works from the parent, it will be very extractive to the minority.

In my books, this is easily a stock that goes into the “too difficult” pile. But fascinating to study nonetheless.