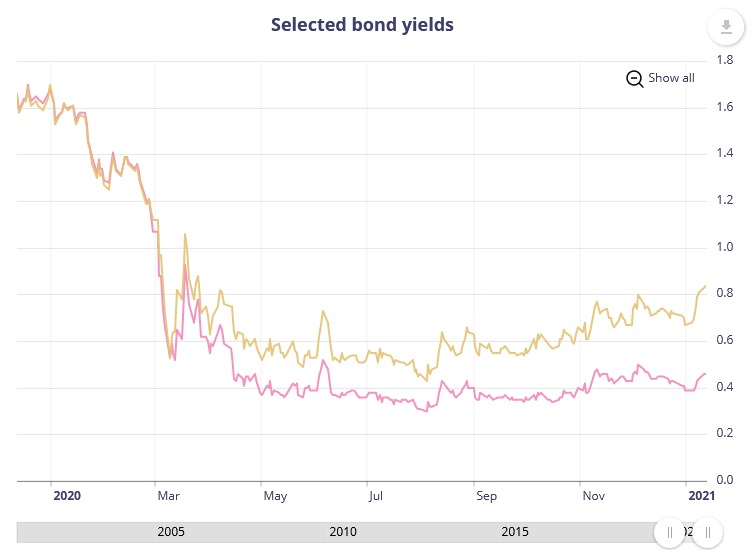

From the Bank of Canada (the 10-year and 5-year government bond yield):

From the end of 2020 (0.67%) to yesterday (0.84%) the 10-year bond yield has risen.

This could just be from the “white noise” of trading. A fixed equity/debt split would surely have resulted in equity selling and fixed income purchasing which to date has not occurred, prices would appear to have done the opposite. US 10-year treasuries are also up about 15bps or so from the beginning of the year.

The impact of rising long-term interest rates have a ripple effect through the market. If the trend continues, you’ll see a dampening effect across the investment spectrum. Right now it is not a lot, but if yields continue to rise another 20bps or so (totally arbitrary guess), more people will start noticing and you’ll start to see momentum effects occur, which would likely be concentrated with price contractions of yield-based instruments (which would have the immediate impact of increasing their yields, but interest rate increases would result in the expense of their ability to borrow money at low rates). Soros’ theory on reflectivity reflexivity really applies here!

Theory of “Reflexivity” 🙂

I remember misspelling this word when initially typing it in and picked the first thing on the spell check without reading it carefully and hitting the publish button. Reflectivity sounds pretty good as well!