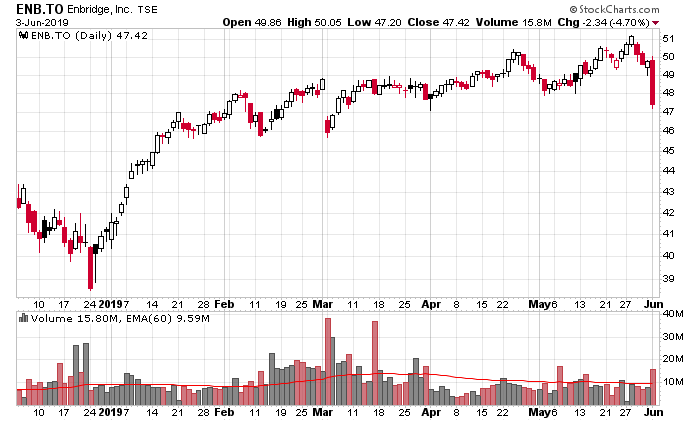

I do not have shares in Enbridge, but investors today (and probably tomorrow as the news came out mid-day and institutions will look at it overnight to digest the impact on valuation) will be feeling slightly less rich after today’s news that the Minnesota court of appeals deemed the environmental assessment concerning Line 3 to be inadequate.

The net result is that Line 3 will have their construction halted until Enbridge can file an appeal or an amended environmental assessment. This will also result in another round of legal battles with the 3Cs of regulation – committees, commissions and courts and my initial estimate would be at least half a year of delays. I could be wrong.

The reason for the delay is not terribly relevant from a financial standpoint, but the impact of it will be for both Enbridge (who will not be realizing increased cashflows from the increased volume that would be flowing through the pipes the second they are activated – not to mention the capital that has already been sunk into the project), but more importantly, land-locked Albertan/Saskatchewan oil producers that were seeing a light ahead of the tunnel after the presumptive second half of 2020 activation of Line 3.

At CAD$50/share, Enbridge was priced for perfection. Although Enbridge is mostly a cash flow story, an investor is paying a lot in advance in order to realize those cash flows – in addition to the requisite risks to pay back the debt, interest and preferred share dividends. Just wait until Line 3 or Line 5 experiences a spill, or some other adverse event which is currently not baked into the stock (or perhaps another adverse legal ruling that will stall it another couple years). Although the company in 2019 is expected to generate around $4.50/share in cash ($8.9 billion), the inherent growth that is available to Enbridge is a limiting factor – and as such, the accounting income P/E in the 20s (which takes into account depreciation) is unjustified. Coupled with large future capital expenditures, if there is any sort of credit situation that may occur in the future, equity owners will be taking a lot more price risk than the current potential for reward – which wasn’t going to be a stock price that much higher than CAD$50/share.

I would especially take issue with the common share dividend, which is currently $6 billion a year – while they can certainly afford to pay this at present (and management continues to escalate the dividend each year), it is not a financial perpetual motion machine – given the capital expenditure profile, this is currently being partially financed with debt.

There aren’t many free lunches in the stock market, including the pipelines. Companies like Inter Pipeline (TSX: IPL), which has less legal risk than Enbridge, are still at valuations that aren’t incorporating much risk to their future expected cashflows (albeit, in IPL’s case, it is a lot better today than it was a couple years ago where it was trading about 30% higher). It wouldn’t surprise me to see Enbridge follow a similar trajectory, but still maintain its equity dividend.

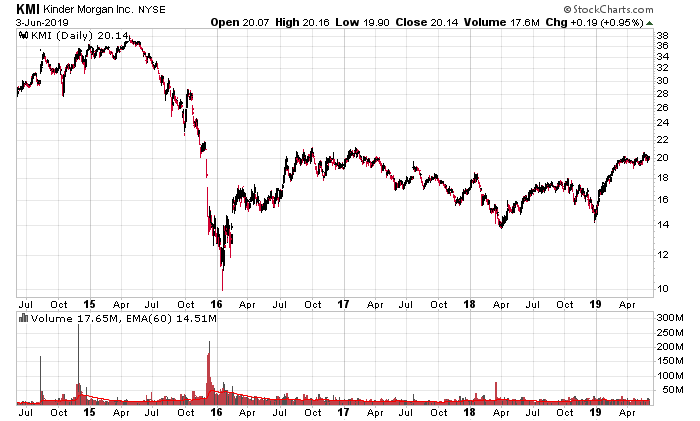

Students of history will want to pay attention to Kinder Morgan (NYSE: KMI), a supposedly safe and stable pipeline company in 2015:

I’ll leave it at that – pipeline companies are supposed to be stable for their cash generation capabilities, but financially it can be a completely different story.