Genworth MI Canada (TSX: MIC) reported their 4th quarter and annual results today. Because they never bothered to post the full financials on their investors website, sadly I had to dredge it out of the parent company SEC filing.

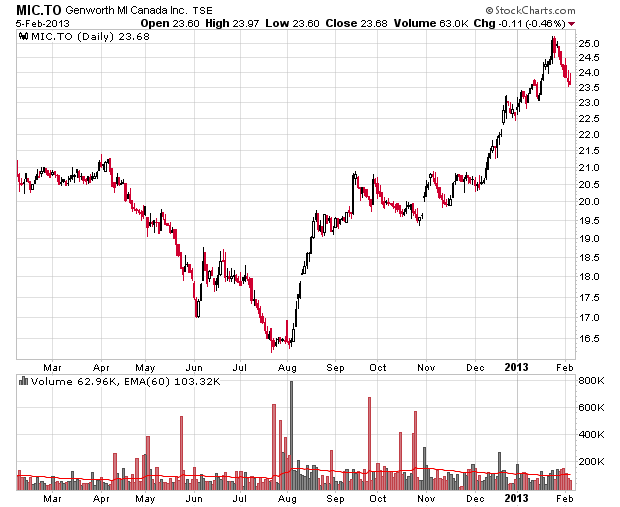

The chart has suggested there is an improvement of sentiment and there was also a scurry of investors in the past few days lightening up their risk in the company in the leadup to the quarterly announcement:

The results have to be translated to exclude the positive impact of the December 20th announcement concerning how they were accounting for the government guarantee fund (which caused a non-trivial reversal in expenses). After doing all the adjustments, the magic number is 90 cents per share earned in the quarter.

The CMHC hitting its insured portfolio ceiling is also visibly helping the business on the private side, despite changes to amortization and down payment rules.

Delinquency rates continue to remain exceptionally low at 0.14% for the quarter (0.2% in the previous year’s quarter).

I haven’t been able to see the consolidated balance sheet as of yet, but book value is $30.62/share, while intangibles and goodwill is approximately 20 cents a share.

With a market value of $23.68/share, they are still deeply betting that the Canadian housing market is going into the gutter. While this might be true price-wise, what is important is the ability for people to pay off their mortgages, and this means employment. Nothing has changed in Canada at present with respect to this and although I believe housing prices will exhibit long-term depreciation (especially when interest rates decide to rise again), this will not adversely affect the mortgage insurance business unless if such price drops are precipitous.

The effective loan-to-value of the insurance portfolio is a good metric of how buffered the company is in the event of a mortgage default. Most of the embedded risk are on new purchases and as payments continue amortization of mortgages continue to result in risk reduction for the company. At the end of the year, the loan-to-value (essentially an inverse measurement of equity) on such insurance is as follows:

2006 and prior – 40%

2007 – 68%

2008 – 73%

2009 – 75%

2010 – 82%

2011 – 88%

2012 – 92%

It should be pointed out that on a typical 5-year fixed rate mortgage at current rates, if there was a 5/10% downpayment made, that the homeowner at the end of the 5-year period will have 18.7/23.0% equity in the property. This is the buffer room that insurance companies have with respect to price deprecation and also are compensated with the 2.75% premium paid on such mortgages.

Needless to say my original thesis is still in effect – Genworth MI is an inexpensive cash machine, even at current prices. Not as good as when it was in the teens when I bought my shares, but still is a very good value. All things being equal, at existing market values, investors should be realizing about a 14% annual return and this does not include any accretion that comes out of a realization of the negative differential between book value and market value. Compared to putting money in bonds, this is a pretty good return given the risk taken (which is low, but certainly not zero – this is what you are being compensated 11% over bonds with!).

The company also gives out a 32 cent/quarter dividend, but this is utterly irrelevant to the investment thesis, which is that there is incredibly deep value in the company. I am quite frankly surprised that the company already hasn’t been hived off to Sunlife (TSX: SLF) or Manulife (TSX: MFC), both of which desperately need diversification from the tragic errors they made with variable life annuities a few years back.

There’s excellent potential for this company to get back to book value and it is just a matter of being patient and not watching the Canadian real estate market implode. As long as that market does not implode, the shareholders should profit immensely.