I hate to sound like a broken record, but I’ve still been doing nothing other than research but nothing worth investing in at the moment except for one illiquid play mentioned in an earlier post.

Here is a series of miscellaneous observations:

* I note that Apple (AAPL) continues its slide down to the point where I am wondering if they are pricing that the company is not going to be able to keep its premium pricing strategy. On paper, they are still massively profitable, but if competition continues to chip away at their product line (mainly through Samsung on the phone front and a variety of other realistic competitors on the tablet front), they might run into revenue growth problems. The company in their last fiscal year (ended September 2012) made $156.5 billion in revenues and this year the analysts are projecting an average of $182.8, which is a $26.3 billion increase year-to-year. This is a huge amount of growth and the law of large numbers will likely be catching up to Apple in short order.

* CP Rail (CP.TO) is trading at absurdly high valuations at present. They performed a change in management and the market is giving the new CEO a lot of credit, but the railroad business is very mature and I don’t have a clue why they are giving the equity such a huge premium at the moment. I’d be a seller at this price range (the C$130 mark).

* Anybody remember the big scare about rare earths a couple years ago when China started restricting the supply and most of those stocks went crazy? The big play here, Molycorp (MCP) has continued to slide into the gutter now that the market reality of the perceived shortage has completely gone away. The substitution effect is very powerful and MCP shareholders are holding the bag.

* Likewise, most other fossil fuel commodity companies, including my favourite company that has been so overrated by many, Petrobakken (PBN), are continuing to suffer. It is similar to how most gold mining companies are not faring nearly as well as the underlying commodity – it costs an increasing amount of money to extract the resource, so even if the commodity price is increasing, if your costs are increasing, you are not going to make much money. Even Crescent Point Energy (CPG.TO) is starting to lose its lustre.

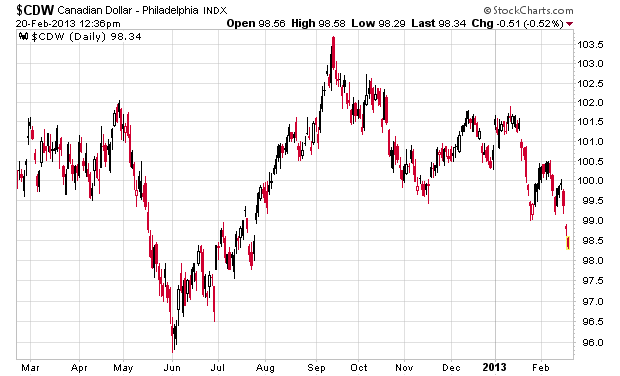

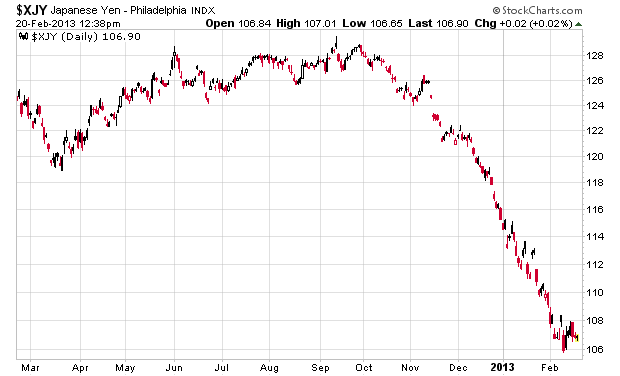

* The other commodity market that is continuing to get my curiousity up is currency trading – the US dollar has continued to outperform most of the other global currencies. The only way that I play this is that I try to hedge my portfolio by having some US-denominated securities rather than using leveraged speculation.

* The two Canadian Real Estate financing proxies, Home Capital (HCG.TO) and Equitable Group (ETC.TO) warrant a further look. HCG has faded somewhat off of its 52-week high, but Equitable is still there. If people are still hyper-bearish on the Canadian real estate market, these two companies should be the first on anybody’s short selling list. Non-performing loans are still around the 0.3% level and currently still do not show any real signs of distress in the market. I am still riding the wave on Genworth MI (MIC.TO) and believe there is still a reasonable percentage gain to be realized from current price levels. The loan companies, however, are hugely leveraged and I’m finding it difficult to see value there when book values are so significantly below market prices.

* Long term interest rates have also taken a nose dive – the Canadian 10-year bond was skirting at the 2% yield a month ago, but now they are back down to 1.8%. The world is awash with capital and there are few places to deploy it where you’ll generate yield at an acceptable risk level. Eventually the leverage party will end and the fallout is going to be very brutal. Whether this happens in 2013, 2014 or later, nobody knows. But there will be fallout, and figuring out how to brace yourself for the fallout will be a big financial challenge over the next decade.