CMHC has announced today a new fee schedule, to be effective May 1, 2014:

| Loan-to-Value Ratio | Standard Premium (Current) | Standard Premium (Effective May 1st, 2014) |

|---|---|---|

| Up to and including 65% | 0.50% | 0.60% |

| Up to and including 75% | 0.65% | 0.75% |

| Up to and including 80% | 1.00% | 1.25% |

| Up to and including 85% | 1.75% | 1.80% |

| Up to and including 90% | 2.00% | 2.40% |

| Up to and including 95% | 2.75% | 3.15% |

| 90.01% to 95% – Non-Traditional Down Payment | 2.90% | 3.35% |

Assuming Genworth MI increases its fee schedule to compensate for this (which is likely), this will have the effect of increasing the company’s premiums written, which in turn will have a proportionate impact on the premium recognition as it is recognized over time. The effect on 2014 earnings will be minimal, but it will start to kick in 2015 and beyond.

At December 31, 2013, 73% of Genworth MI’s loan portfolio had a loan-to-value level of 80% or higher, so it stands to reason that they will be making a not trivial increase in this. However, one would observe that the 15% downpayment rate only will be experiencing a very minor increase in premium (1.75% to 1.80%) and chances are this “sweet spot” will lead to gains less than expected.

For the calendar year 2013, Genworth MI’s loss ratio was 25% and expense ratio was 20%. Mortgage delinquencies are quite low at present.

To those prospective homebuyers out there that want to avoid this mess: Just pay 20% down. If you have any decent credit profile, lenders will not require mortgage insurance.

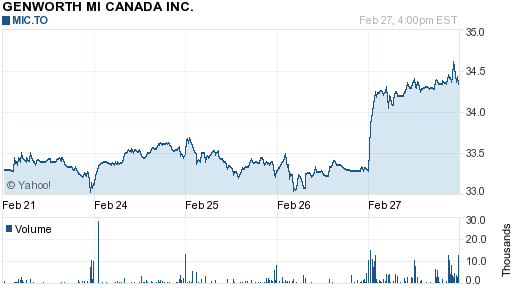

Genworth MI is up about 5% as of the time of this writing.